rewrite this content and keep HTML tags As of early March, a majority of the public (59%) is worried about affording prescription drugs for themselves and their families, the largest share since KFF first polled this question in 2018.

Source link

As TrumpRx Expands to Include Generic Drugs, KFF Polling Shows Nearly 6 in 10 Adults Are Worried About Prescription Drug Costs

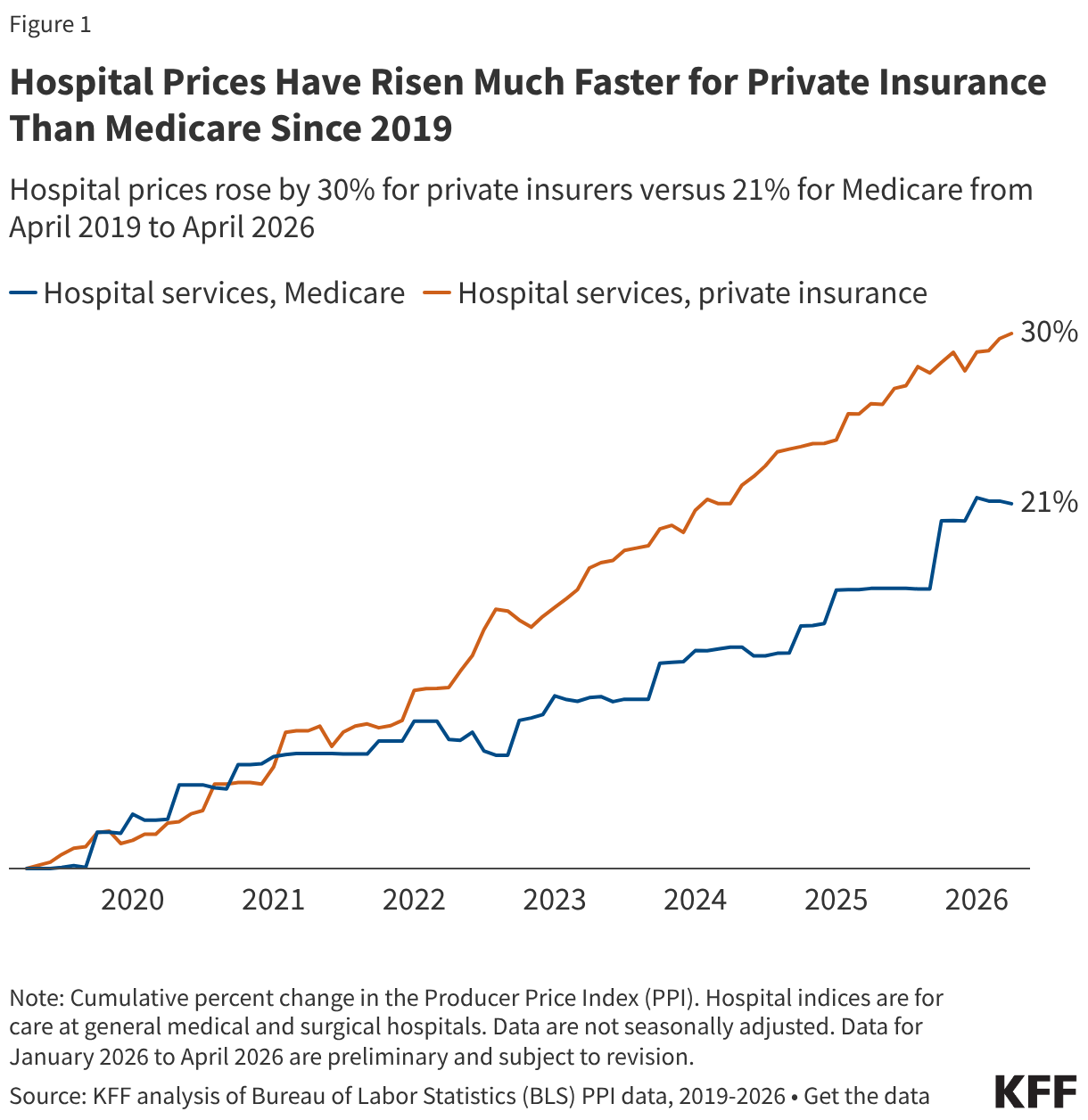

Hospital Prices Have Risen Much Faster for Private Insurance Than Medicare Since 2019

rewrite this content and keep HTML tags

Health care costs are a top concern for the public, and there is widespread interest among lawmakers in making health care more affordable. Attention has increasingly focused on hospitals, which represent nearly one third of total health care spending and accounted for 40% of spending growth from 2022 to 2024. Hospital spending reflects both the prices paid for services and the volume and intensity of care delivered, and trends in both factors have implications for affordability and spending growth. The prices paid by private insurers are higher than Medicare rates on average—e.g., nearly double traditional Medicare rates for hospital services when averaging across studies, according to a prior KFF review—and vary across regions and across hospitals and payers within regions. These high prices affect households through higher premiums and cost sharing obligations and reduced wages for those with employer-sponsored health coverage.

There has been some discussion at both the national and state level about policies that could rein in hospital prices. One set of policies aims to do so by promoting competition and reducing consolidation in provider markets. A substantial body of evidence shows that hospital market consolidation has contributed to higher prices, with unclear effects on the quality of services provided. Another set of policies would rein in prices more directly, such as by capping the prices that providers can charge. For example, Indiana recently enacted a law that will eventually cap private insurance prices for the state’s nonprofit hospitals, and Oregon has capped hospital prices at 200 percent of traditional Medicare rates for its state employee plan since 2019.

To inform policy discussions related to hospital prices and price regulation, this brief describes the growth of prices paid by private insurers for hospital care relative to increases in Medicare payment rates from April 2019 through April 2026, using data from the Bureau of Labor Statistics (BLS) Producer Price Index (PPI). The analysis begins in 2019 to fully capture changes in prices during the pandemic. See Methods for more detail.

Hospital Prices Have Risen Much Faster for Private Insurance Than Medicare Since 2019

Private insurance prices for hospital care rose 30% from April 2019 to April 2026 compared to a 21% increase in Medicare rates (Figure 1). Put differently, private insurance prices grew 47% more quickly than Medicare rates over this 7-year period. Private insurance prices grew at a similar pace as Medicare rates from April 2019 to April 2020, but grew more quickly than Medicare rates each year from April 2020 to April 2025, before increasing less quickly than Medicare rates from April 2025 to April 2026. These patterns are broadly consistent with prior research that finds faster price growth for private insurance than Medicare over time, with some variation across time periods. Private plans pay much higher rates than Medicare for hospital services according to prior research, and this analysis suggests that the gap has increased over time.

Private insurance prices for hospital care are the result of negotiations between hospitals and insurers. Increases in private prices over time can reflect changes in the cost of providing care and in the bargaining power of hospitals relative to insurers, among other factors. Hospital markets have become increasingly consolidated, with one or two health systems controlling at least 75% of the market for inpatient hospital care in the large majority of metropolitan areas (83%) in 2024, according to KFF analysis, contributing to higher prices. Large increases in labor and supply expenses during the pandemic have likely pushed providers to negotiate for higher prices (economy-wide inflation jumped in March and April 2021 before reaching a peak in June 2022). However, contracts between hospitals and insurers are only periodically renegotiated, and often last for multiple years, meaning there may be a lag before any effects of higher input costs are fully reflected in higher prices.

In contrast, traditional Medicare hospital prices are updated annually by the Centers for Medicare and Medicaid Services (CMS), primarily through the Inpatient and Outpatient Prospective Payment Systems (IPPS and OPPS). These changes are based on factors and methods described in law and regulation. Medicare IPPS and OPPS updates are based partially on estimates of increases in hospital services input costs, which are affected by overall inflation. There is some evidence that rates paid by Medicare Advantage plans for hospital services (incorporated with other private Medicare plans in the Medicare but not private insurance PPI) are generally close to rates paid by traditional Medicare. Increases in prices paid by Medicare Advantage insurers have likely been aligned with changes in traditional Medicare rates over time.

One factor that slowed Medicare growth is that the program underestimated inflation in recent periods when prospectively setting rates (e.g., inflation in 2022 was much higher than expected when hospital rates were set for that year), according to the hospital industry and others. Nonetheless, CMS has noted that its forecasts have tended to be close to actual inflation on average when looking over longer periods for the IPPS hospital market basket (see Methods for more detail).

Various other factors may have restrained Medicare price growth during the study period, such as the productivity adjustments enacted under the Affordable Care Act, which reduce the growth in traditional Medicare rates over time under the assumption that hospitals are becoming more efficient at delivering care. As another example, sequestration, which is an automatic reduction in Medicare payments required under budget rules, was temporarily suspended during the pandemic beginning in May 2020 but gradually reintroduced in April and July 2022, likely contributing to the increase and decrease in the Medicare PPI during those periods.

Methods

This brief used the Producer Price Index (PPI) to evaluate hospital prices and overall inflation over the seven year period from April 2019 to April 2026 (the most recent month available). The PPI measures prices from the perspective of producers of a good or service, such as hospitals. The PPI was used over other comparable measures like the Consumer Price Index (CPI) because it breaks out hospital price growth by payers, such as Medicare and private insurance. The PPI for private insurance excludes private Medicaid and Medicare plans. The PPI for Medicare includes both traditional Medicare and private Medicare plans, including Medicare Advantage, which accounted for 54% of the eligible Medicare population in 2025.

Hospital price growth overall (i.e., across all payers) as measured by the PPI grew much less quickly than hospital price growth as measured by the CPI during this period. Differences between the PPI and CPI reflect both conceptual and methodological differences. For example, the CPI—which measures prices from the perspective of consumers—excludes Medicare Part A, Medicaid, and certain other payers from its price measurements.

This analysis examines hospital PPI data classified by industry, in this case, the hospital industry. The PPI also produces series classified by a specific commodity, such as a product or service. This brief uses industry classifications because they provide an overall measure of hospital prices by payer, while the commodity classifications are separated into inpatient and outpatient price measures and only distinguish private insurers from other non-Medicare, non-Medicaid payers for the former.

Most of the increases in the Medicare hospital PPI occur in October and January over time. That likely reflects, at least in large part, the timing of when traditional Medicare updates inpatient and outpatient reimbursement for hospitals, respectively.

CMS noted in its FY2026 IPPS rule that its forecasts for the IPPS hospital market basket have tended to be close to actual inflation on average when looking over longer periods. This basket is used for both IPPS operating and OPPS payment updates (though it is unclear if CMS’s comment above was also including OPPS payments, which are updated on a different schedule). During the 2026 rulemaking process, CMS received comments, including from the hospital industry, recommending an increase in IPPS operating and OPPS payment rates to account for prior errors in forecasting, though CMS did not do so, citing various reasons. CMS does make certain adjustments for forecasting errors for IPPS capital payments (as it has proposed to do in FY2027), which account for a relatively small share of hospital payments.

A Look at the GENEROUS Model and Factors That Could Impact Medicaid Drug Costs

rewrite this content and keep HTML tags

While spending on prescription drugs accounts for a relatively small share of overall Medicaid spending, Medicaid drug spending has grown in recent years. As a result, both states and the federal government continue to prioritize the management of rising prescription drug costs. There have been several recent Trump administration prescription drug initiatives, including negotiating “most-favored-nation” (MFN) drug pricing deals. These MFN agreements are based on the premise that the U.S. shouldn’t pay higher prices for prescription drugs than other comparable nations. The deals include agreements by drug manufacturers to provide MFN pricing in Medicaid and other commitments in return for a 3-year reprieve from tariffs, though the specific details of these agreements remain confidential. Though prices vary across countries, studies have shown that drug prices in the U.S. are about three times higher than in other countries.

To make MFN drug prices available to state Medicaid programs, the Centers for Medicare & Medicaid Services (CMS) developed the GENEROUS (GENErating cost Reductions fOr U.S. Medicaid) Model, a drug payment model through which CMS will negotiate supplemental drug rebates based on prices paid in other countries. Given significantly lower drug prices internationally, this approach could result in substantial Medicaid savings, with a recently released White House report estimating that a voluntary MFN framework in Medicaid would save $64.3 billion over a 10-year period. While initial savings would be large and diminish over time – in part due to the fact that prices in other countries might increase as a result – savings would average $6.43 billion a year, or approximately 14% of annual Medicaid prescription drug spending.

However, it is unclear what assumptions were made to develop the administration’s estimates, and there remain several uncertain factors that make it difficult to assess the overall impact the new model will have on Medicaid drug costs. This issue brief provides background on the GENEROUS model, examines the factors that will contribute to the model’s overall impact on Medicaid drug costs, and illustrates how savings will depend on model details that are confidential or uncertain at this time. Key takeaways include:

- The impact of the GENEROUS model on Medicaid prescription drug spending remains unclear due to several uncertain factors related to drug pricing and model participation.

- Existing Medicaid rebates already reduce overall Medicaid prescription drug spending substantially, likely limiting the impact of the GENEROUS model’s MFN supplemental rebate approach.

- GENEROUS model savings will depend on which manufacturers and states participate as well as what drugs are included in the model due to variation in drug rebates (and net prices) as well as spending and utilization trends.

What Is the GENEROUS Model?

The CMS Innovation Center launched the GENEROUS model in January 2026 with the goal of lowering Medicaid drug spending by offering prices based on what other countries pay. The model is voluntary for manufacturers, though it is expected that the seventeen pharmaceutical companies (e.g. Pfizer, AstraZeneca, etc.) that have signed MFN agreements will participate. Manufacturers now have until June 11, 2026 to apply to participate in the GENEROUS model (the deadline has been extended twice from March 31, 2026 to April 30, 2026 and again to June 11, 2026). The model is also voluntary for states, with states having until July 31, 2026 to submit their application and until August 31, 2026 to execute a state participation agreement with CMS. States may be able to join the model after August 31, 2026 at CMS discretion. The model will run for five years through 2030, though manufacturers and states may voluntarily terminate their participation and key terms between CMS and manufacturers may be renegotiated.

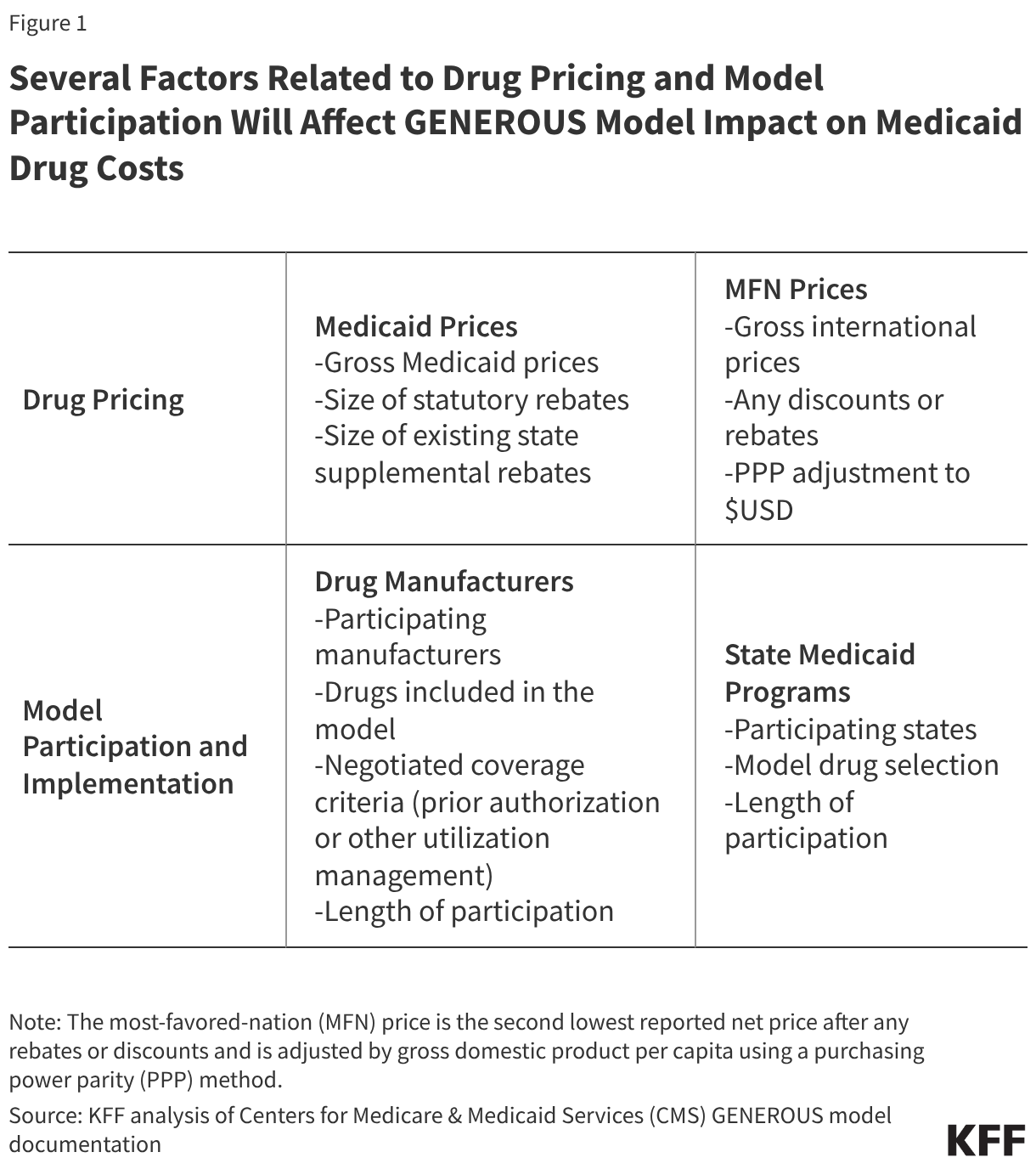

Through the GENEROUS model, CMS will negotiate supplemental drug rebates based on prices paid in other countries (or the “MFN price”). For model drugs (single source or innovator multiple source drugs, also known as brand drugs), CMS will calculate the MFN price based on international pricing data provided by manufacturers across eight other countries (the United Kingdom, France, Germany, Italy, Canada, Japan, Denmark, and Switzerland). The MFN price is the second lowest reported net price after any rebates or discounts and is adjusted by gross domestic product per capita using a purchasing power parity method. CMS will then calculate the supplemental rebate for each model drug that results in a Medicaid net price equivalent to the MFN price (more specifics on the MFN price and Medicaid guaranteed net unit price calculations are available in both the state request for applications (RFA) and the manufacturer RFA). States can select which model drugs they’d like to receive MFN pricing for and must enter into new supplemental rebate agreements (SRAs) that reflect the model’s key terms (states cannot receive additional supplemental rebates outside of the model for drugs they have opted into).

CMS and participating manufacturers will also negotiate uniform coverage criteria, which includes utilization controls such as prior authorization or step therapy. These terms will be based on existing criteria states have negotiated, and states will have to adopt the uniform criteria to access the supplemental rebate for a given drug. States currently negotiate their own SRAs with manufacturers and use an array of payment strategies and utilization controls to manage prescription drug expenditures. States often use placement on a preferred drug list (PDL) and prior authorization as leverage to negotiate supplemental rebates with manufacturers, though the specific strategies vary by state. The negotiation of standardized coverage criteria could help reduce the administrative burden for states and manufacturers of negotiating individual SRAs tied to specific clinical criteria. However, the negotiated criteria may be more broad or more restrictive than the criteria states have already developed, which could have implications for state participation and model savings.

CMS will also conduct GENEROUS model monitoring and evaluation. The law requires Innovation Center models to either maintain or reduce program expenditures, and the model will test whether the MFN supplemental rebate approach can reduce Medicaid drug costs. To the extent negotiated clinical criteria broadens, the model may also increase enrollee access. Throughout the model, CMS will track data and assess the impact of the model on health care spending and access to care as well as audit the manufacturer reported international drug pricing data. GENEROUS works within the existing Medicaid Drug Rebate Program (MDRP) framework and builds on other CMS supplemental rebate models including the Cell and Gene Therapy Access Model and the BALANCE model. Notably, while these models aim to address high drug costs for the Medicaid program, they do not affect out-of-pocket costs for Medicaid enrollees, which are limited to nominal amounts under federal law.

What Are the Potential Impacts on Medicaid Prescription Drug Spending?

The impact of the GENEROUS model on Medicaid prescription drug spending remains unclear due to several uncertain factors related to drug pricing and model participation. Several factors will affect model cost savings (Figure 1), many of which are confidential or not yet available, including:

- While data on gross drug prices is available, data on the size of rebates for specific drugs is proprietary in both Medicaid and internationally, making it difficult to compare net Medicaid prices to net international prices.

- At this time, it also remains uncertain which manufacturers and states will participate in the model and how long participation will last.

- Further, while model documentation makes it clear that states may select model drugs, it remains uncertain whether all drugs in a participating manufacturer’s portfolio will be subject to the model. The RFAs note that “model drugs are limited to all the single source drugs or innovator multiple source drugs of a participating manufacturer”, indicating manufacturers must include all of their covered outpatient drugs. However, the RFAs also report that the listed terms may differ from the final terms, and a CMS presentation to states noted “manufacturers will opt into the model for certain branded Medicaid covered outpatient drugs”, leaving it uncertain whether all of a manufacturer’s drugs will be subject to MFN pricing or if exemptions will be available. Recent letters from the Senate Finance Committee sent to drug manufacturers push for more model details, including which drugs will be included in the model.

- Lastly, details on the uniform coverage criteria for model drugs have not been released, making it difficult to assess the impact the terms may have on drug spending or access.

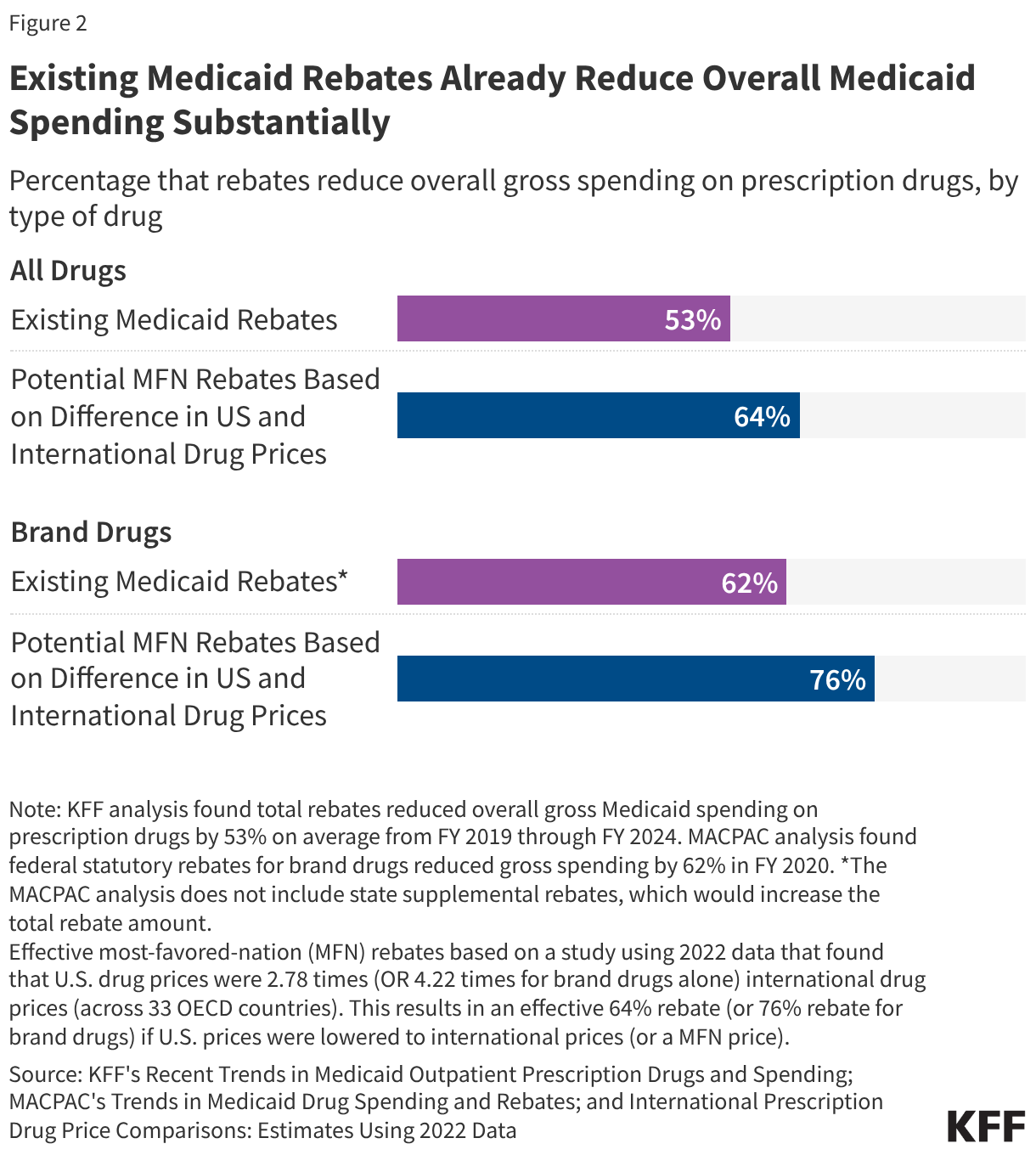

Existing Medicaid rebates already reduce overall Medicaid drug spending substantially, likely limiting the impact of the GENEROUS model’s MFN supplemental rebate approach. Medicaid programs already pay lower prices, net of rebates, than other payers due to the MDRP, which requires manufacturers to rebate a portion of drug payments to states. Medicaid rebates overall reduced gross Medicaid spending on prescription drugs by 53% on average from FY 2019 to FY 2024 (Figure 2). Rebates for brand drugs are typically even higher, with a Medicaid and CHIP Payment and Access Commission (MACPAC) analysis of FY 2020 data finding a 62% rebate overall for brand drugs.

At the same time, a recent study showed that U.S. drug prices overall were 2.78 times international drug prices (across 33 OECD countries); this differential is similar to those found in other research. Assuming U.S. drug prices are 2.78 times more than international prices, this would mean international prices are about one-third (36%) of U.S. drug prices. Based on this calculation, an MFN approach that reduced prices to international levels would provide a 64% rebate off existing U.S drug prices (Figure 2). The same study found U.S. brand drug prices were 4.22 times international drug prices, which is effectively a 76% rebate. While this is an illustrative example based on non-Medicaid specific drug prices in aggregate, it indicates that an MFN approach could provide substantial discounts given the large difference between drug prices in the U.S. and abroad. However, Medicaid already receives sizeable rebates, signaling there may be limits to this approach when applied to the Medicaid program.

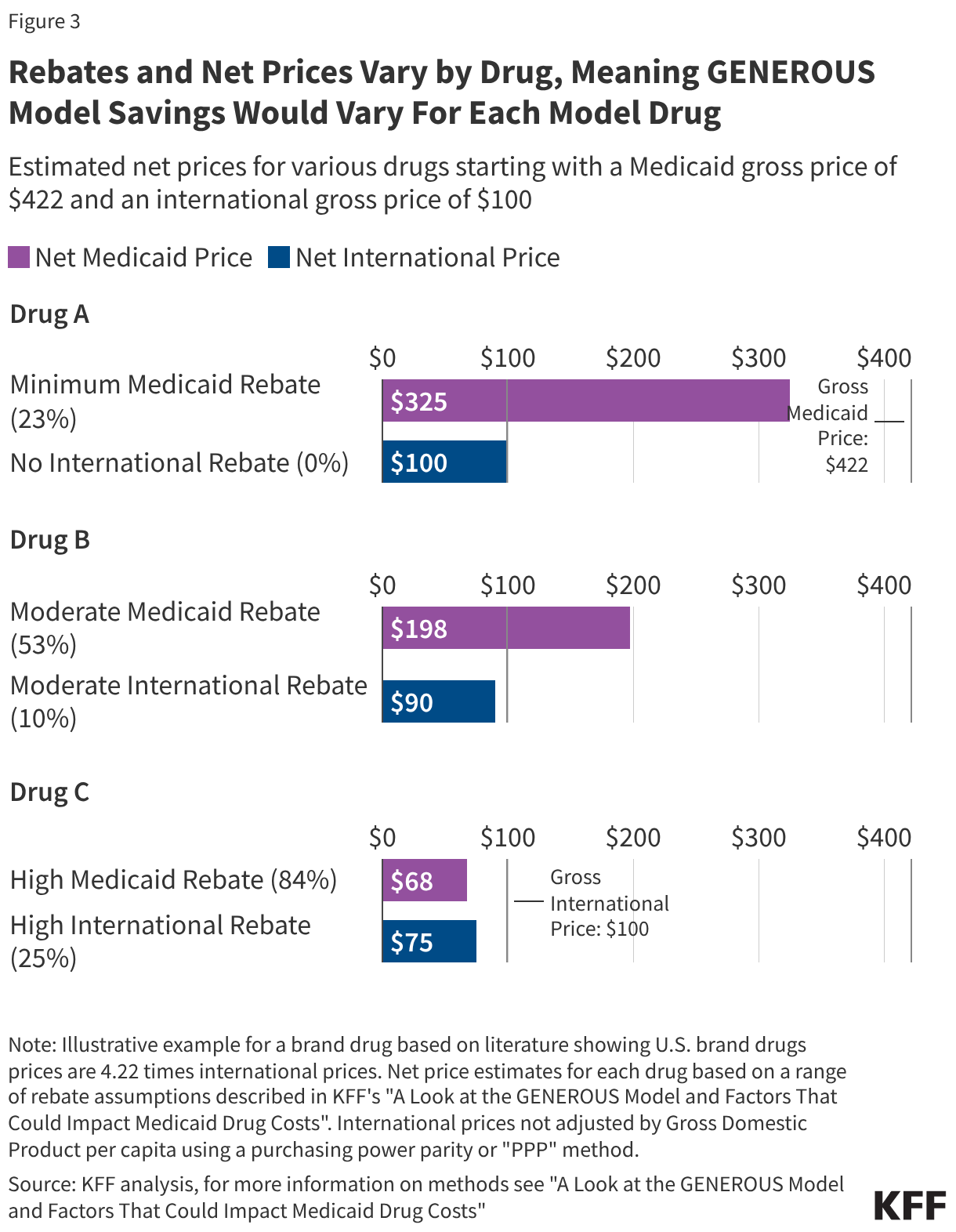

However, rebates and net prices vary substantially by drug, meaning GENEROUS model savings will vary for each model drug (Figure 3). While data on the total rebate for a specific drug is confidential, rebates vary substantially by drug. The minimum federal statutory rebate for a brand drug is 23.1%, but FY 2020 data shows statutory rebates for brand drugs subject to Medicaid’s best price provision and inflationary rebate component are generally much higher, reaching 77% overall. Further, as of January 1, 2024, there is no longer a cap on the total rebate amount if a drug’s price increases quickly over time, meaning overall rebates may now be even higher. In addition to these federal statutory rebates, states have been increasingly negotiating supplemental rebates with manufacturers, with supplemental rebates across states reducing gross Medicaid spending by 7% in FY 2024 (resulting in a higher total rebate estimate of 84% if added to the 77% in statutory rebates for some brand drugs). International countries in the model may also negotiate rebates or discounts. Available studies indicate rebates vary by type of drug and country, ranging anywhere from 0% of gross spending in Japan to about 25% or more in several model countries including Canada, Germany, France, Switzerland.

To illustrate, this analysis examines three example drugs (Drugs A-C), all with a gross Medicaid price of $422 compared with $100 internationally (based on the above study) but with different sized rebates (Figure 3). Some drugs, typically newer drugs with few (or no) competitors in their therapeutic class, may have smaller rebates and large gaps between the net Medicaid and net international price (like Drug A). For example, Biktarvy, the first single tablet combination HIV treatment with the ingredient bictegravir, was FDA approved in 2018 and had an estimated Medicaid rebate of 24% in 2019. It can be difficult for states to secure supplemental rebate agreements for these types of drugs, meaning their inclusion in the model would likely result in savings for states but at a cost to manufacturers.

However, there are also drugs, typically those with more competitors or that have been on the market longer, for which states are already receiving sizeable Medicaid rebates (like Drug B or C). For example, Eliquis, an anticoagulant (or blood thinner), was FDA approved in 2012 and had an estimated Medicaid rebate of 100% in 2019, meaning Medicaid programs are likely paying little to nothing for the drug. In cases where Medicaid rebates are already high, there may not be substantial savings for states through the GENEROUS model, but the impact of the model on manufacturer profits would be mitigated.

Medicaid drug rebates also vary by state, resulting in differing model impacts across states. While federal statutory rebates are required by law and calculated by CMS, the number and magnitude of SRAs vary across states. Medicaid rebates reduced gross Medicaid spending on prescription drugs by 53% on average nationally from FY 2019 to FY 2024, though the percentage varies across states. MACPAC data from FY 2024 shows that drug rebates (including both statutory and state supplemental rebates) reduced gross Medicaid spending on drugs by less than 40% in four states (Kentucky, Oregon, South Dakota, and Virginia) to over 90% in another four states (Delaware, Mississippi, Nevada, and Wyoming). This variation likely reflects differences in the amount and types of drugs paid for as well as differences in SRAs across states. States will likely complete their own internal analyses to assess model impact, including comparing their existing supplemental rebate agreements to what is available under the model and analyzing the impacts of standardized criteria before entering into new model SRAs.

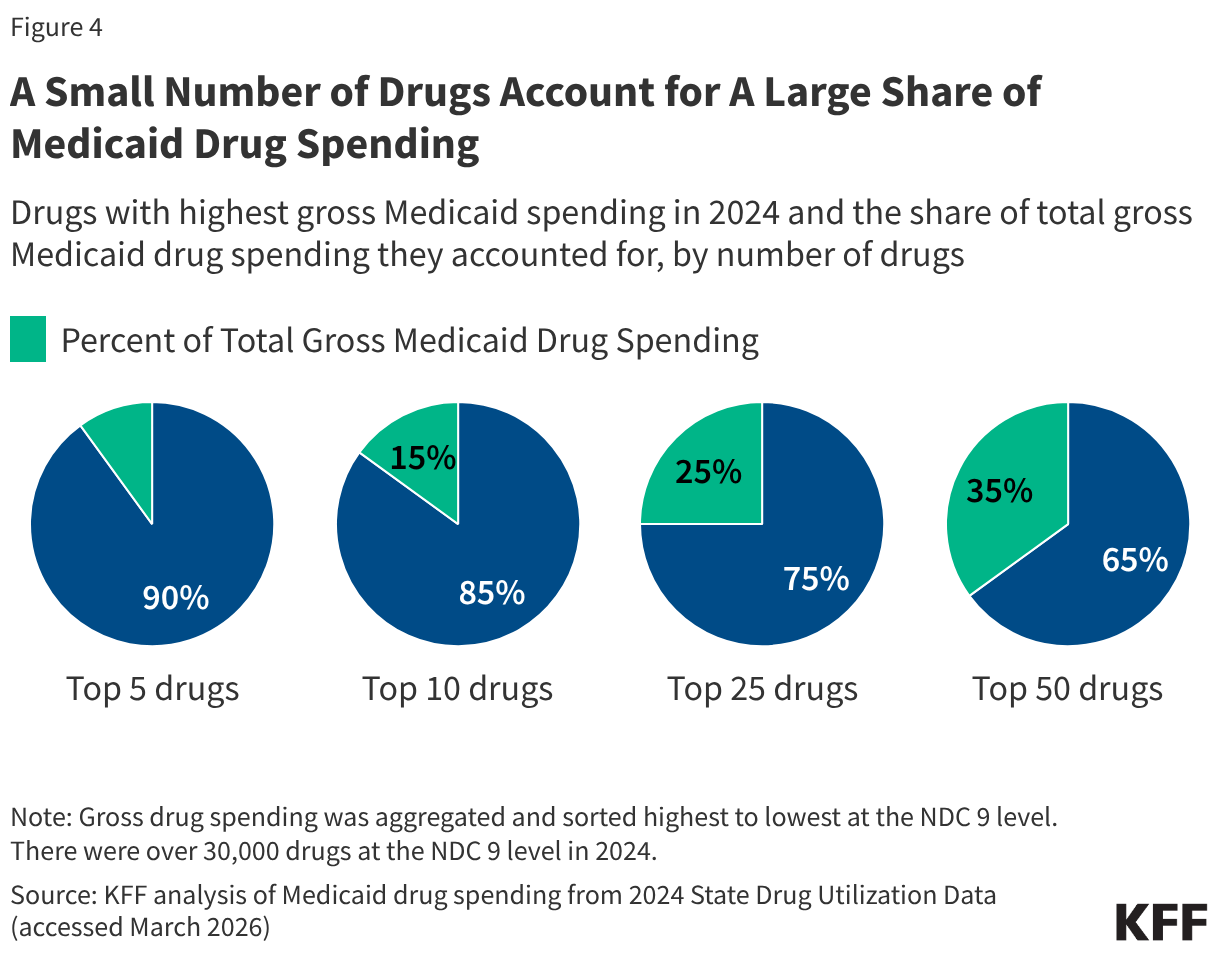

Medicaid drug utilization and spending patterns will also have implications for the Medicaid savings possible under the model. KFF analysis of Medicaid State Drug Utilization Data shows that a relatively small number of drugs account for a large share of Medicaid drug spending (Figure 4). The top five drugs (Biktarvy, Humira, Stelara, Dupixent, and Ozempic) account for 10% of all Medicaid drug spending, and the top 50 drugs account for over one-third of all Medicaid drug spending. Substantial MFN supplemental rebates on the costliest and most utilized drugs for Medicaid programs could result in significant savings (if the drugs are not already subject to sizeable Medicaid rebates), whereas substantial rebates on drugs that are not frequently utilized or only account for a small share of spending would have less of an impact. In addition, the overall number of participating manufacturers and model drugs as well as the number of participating states will affect the magnitude of savings.

Overall, GENEROUS model savings will depend on who participates, both manufacturers and states, and what drugs are included. While these factors remain uncertain at this time, the implications for Medicaid drug costs may become clearer as additional model details become available or if manufacturers respond to recent Senate letters requesting details of the Trump administration’s deals. Looking ahead, substantial state participation will likely indicate the potential for considerable model savings as states may only opt in if they expect the model supplemental rebates to be larger than their current supplemental rebates. States are also currently facing broader state budget pressures and federal Medicaid cuts, which may make some states eager to adopt pharmacy cost containment strategies. Further, manufacturer model participation may increase following the recent announcement of new pharmaceutical tariffs for companies who have not yet entered into MFN deals, though it is not clear what will happen to manufacturer participation when the tariff reprieves end. Once implemented, the GENEROUS model could also have implications for Medicaid prices on drugs from non-participating manufacturers or for the broader drug market, including changes in international prices or manufacturer participation in international markets.

There Are Many MAHAs | KFF

rewrite this content and keep HTML tags

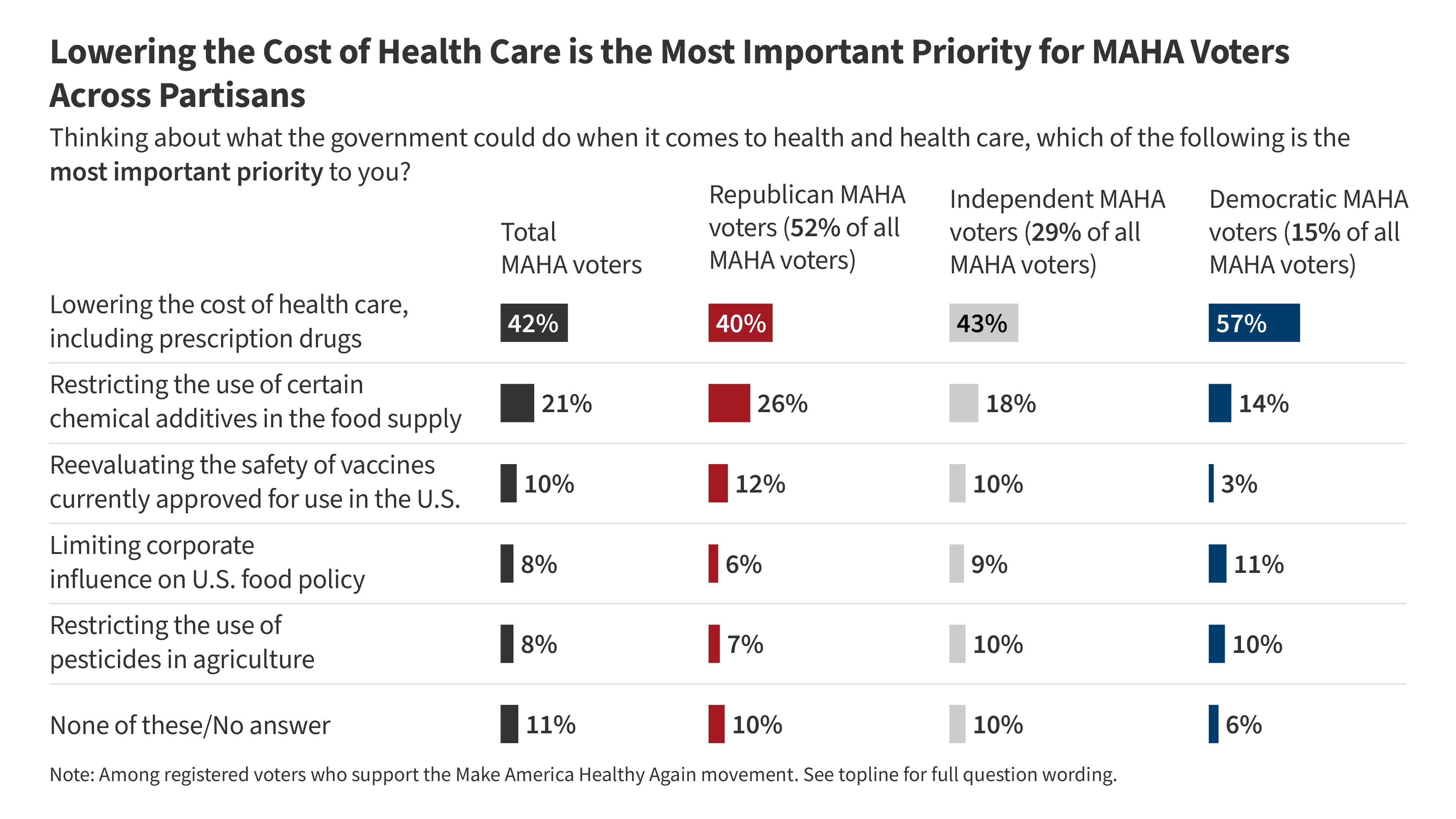

Make America Health Again (MAHA) is led by influencers and commentators and Secretary Kennedy and through that vanguard, it has influence, but the MAHA movement is not a monolith, and it may not be a movement. MAHA is a collection of Americans with interests in different health issues, felt with varying degrees of intensity, and like all Americans, they care much more about health care costs than the issues typically associated with them or with Secretary Kennedy.

This matters because with so many different issues in the MAHA stew, they are not likely to behave as a block on policy issues or in elections. Nor will Secretary Kennedy likely be able to control or deliver them as a group; just parts of MAHA who support him most strongly, which looks like about a third of MAHA supporters.

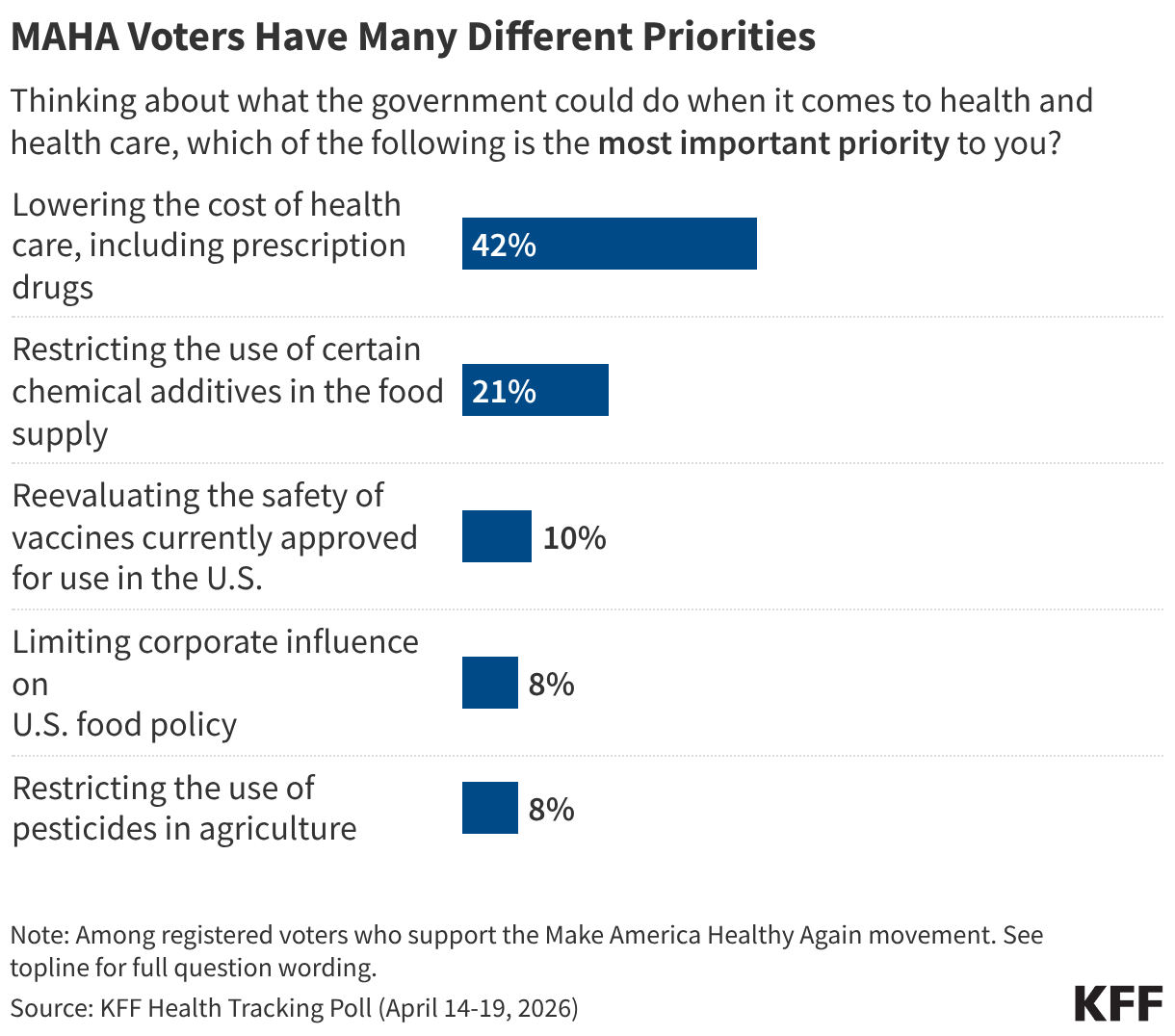

The chart tells the story. Twice as many MAHA voters (42%) say lowering health care costs is their top priority for government than say that about their next highest health priority, which is restricting food additives (21%). Vaccines are down the list, picked by just 10%. One issue, pesticides, was picked by 8% as the top priority. That’s an example of an issue that generates considerable intensity from an influential minority. Raw numbers don’t always equal influence.

One big take-home message: it’s not the case that MAHA and Republicans have unlocked a key to voters by focusing on “health” while Democrats focus on coverage and costs; MAHA voters are also focused on costs and affordability. MAHA influencers and leaders are not generally focused on costs and affordability, except occasionally to assert that a healthier population will bring costs down. How many will vote their party (most are Republicans), or the issue (health costs, on which Democrats have a significant advantage) remains to be seen. About one in five MAHA supporters are Democrats.

A second take-home message: there appear to be many MAHAs, not one. You can care about pesticides, or food additives, or vaccines, or child health, or corporate influence, or all of the above, to varying degrees. The reason so many Americans say they support MAHA when asked in polls is that, like a restaurant with a large menu, there is something in it for many Americans to select. But, the one thing they care about most—their health care costs—isn’t on the menu.

KFF Health Tracking Poll: MAHA and the Midterms

rewrite this content and keep HTML tags

Key Takeaways

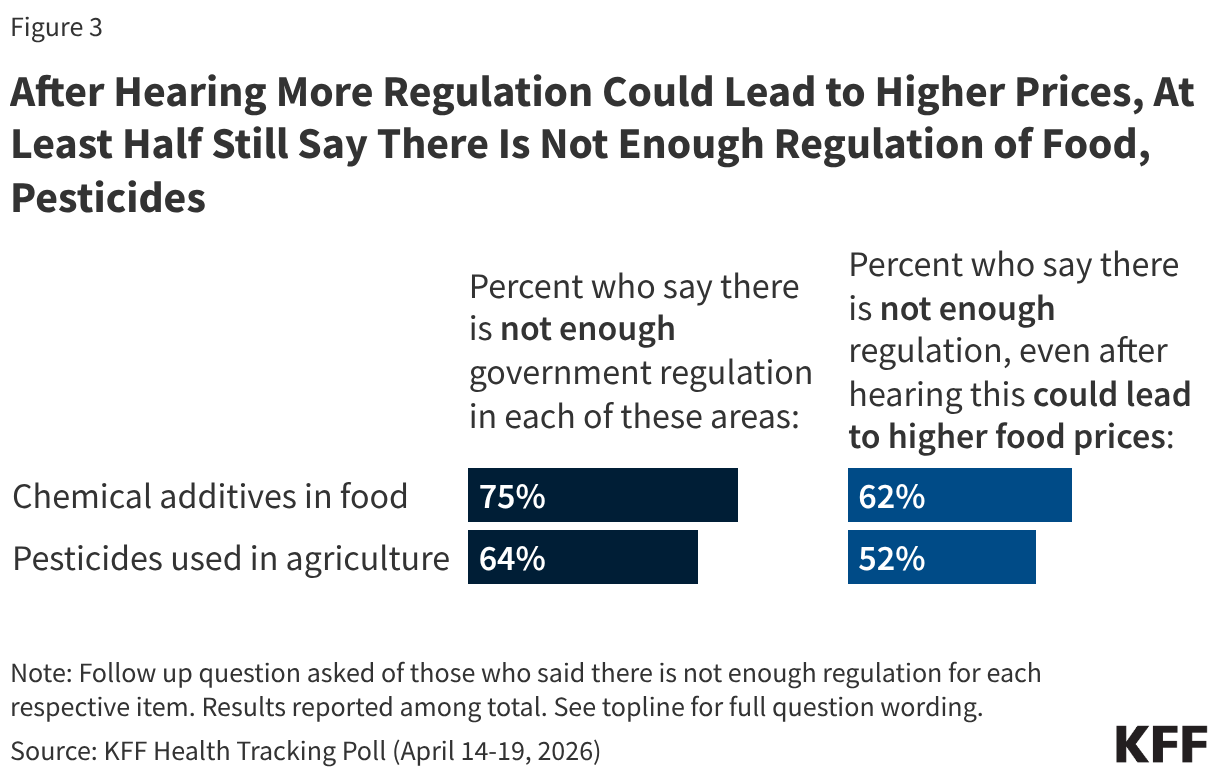

- About four in ten (41%) U.S. adults say they support the Make America Healthy Again (MAHA) movement – a group largely made up of Republicans and supporters of the Make America Great Again (MAGA) movement. Yet, many of the concerns elevated by the MAHA movement about food safety and corporate influence resonate with a larger share of the public beyond those who identify as supporters. Majorities of the public say there is not enough regulation of chemical additives in food (75%) or of pesticides used in agriculture (64%) in the U.S., and most adults express distrust in agricultural, food, and pharmaceutical companies to act in the public’s best interest. At the same time, confidence in the government agencies that are tasked with regulating these industries is low across partisans; about a third of the public express confidence in the FDA (36%) and the EPA (36%) to act independently without outside interference.

- Even as MAHA issues resonate, the cost of health care is a more prominent focus for voters than issues like food and vaccine policy. Most voters say health costs will have a “major impact” on their decision to vote (55%) and who they vote for (61%) in November, compared to about four in ten who say the same of vaccine or food policy. Even among voters who support the MAHA movement, health care costs are the dominant priority by a wide margin when compared with other areas of health. When asked to select the most important health priority for the federal government, four in ten MAHA voters (42%) choose lowering health costs, twice the share who choose restricting chemical additives in the food supply (21%) and far outranking other MAHA priorities like reevaluating vaccine safety (10%), limiting corporate influence in U.S. food policy (8%), or restricting pesticide use in agriculture (8%).

- Voters overall give the Trump administration low approval ratings on two key health areas elevated by the MAHA movement; about four in ten approve of the administration’s handling of vaccine policy (38%), and fewer than half approve of the administration’s handling of food policy (46%). The Democratic Party holds the advantage over the Republican Party in who voters trust to handle vaccine policy (41% vs. 25%) and to ensure federal health agencies act independently without corporate influence (33% vs. 24%). Voters are more evenly divided on whether they trust Democrats (31%) or Republicans (27%) to handle the safety of food additives and pesticides, or neither party (31%).

Who Are MAHA Supporters?

Make America Healthy Again (MAHA) is the political and public health movement promoted by the Trump administration and led by Health and Human Services (HHS) Secretary Robert F. Kennedy Jr. The movement has elevated issues such as vaccine safety, the role of corporate interests in federal health agencies, and the presence of chemical additives and pesticides in the food supply. KFF’s latest Health Tracking Poll shows about four in ten adults say they are supporters of the MAHA movement, but some of the concerns elevated by the MAHA movement resonate well beyond its core supporters.

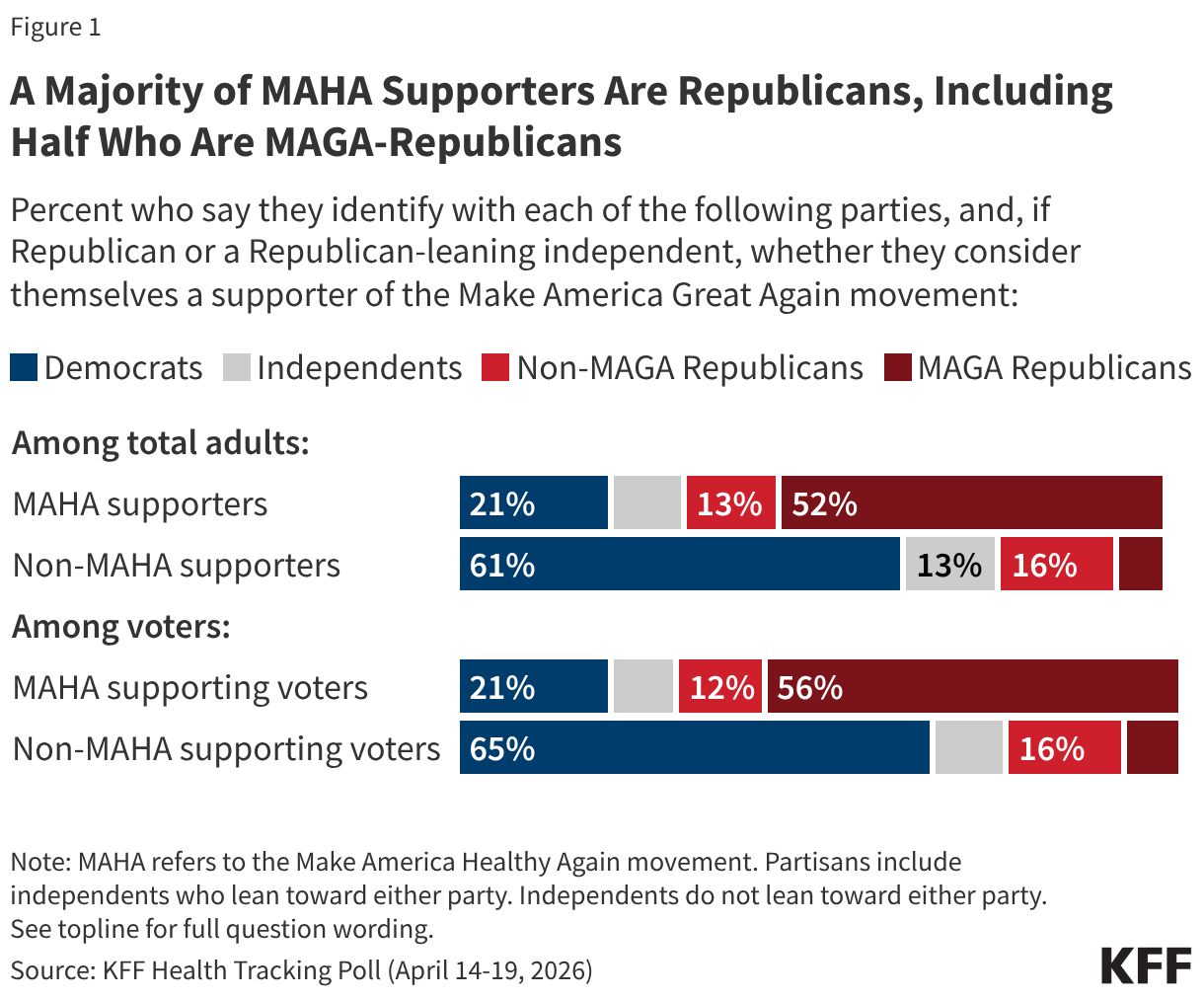

Overall, about four in ten (41%) adults – and a similar share of voters (43%) – say they are supporters of the MAHA movement, with support closely tied to partisanship and support of the Make America Great Again (MAGA) movement. Two-thirds of MAHA supporters identify as Republican or Republican-leaning independents, including about half (52%) who are supporters of the MAGA movement. Far fewer MAHA supporters are Democrats or Democratic-leaning independents (21%) or independents who do not lean toward either political party (10%). Among registered voters who support MAHA, the partisan composition is similar.

Among MAHA-supporting voters, just over half say they “strongly” support the movement (55%) and 45% say they “somewhat” support it, translating to about one in four voters overall as strong MAHA supporters (24%) and one in five who “somewhat” support it (19%).

When asked specifically why they support the MAHA movement, supporters give a range of answers, with the two most common relating to generally wanting people to be healthier (19%) and removing or regulating harmful substances in food (15%). Some MAHA supporters mention improving nutritional habits for Americans (7%) or lowering obesity rates (7%). Five percent of MAHA supporters cite health care access and affordability as their reasons for supporting the movement, despite the MAHA movement’s lack of focus on these issues. Just 4% of MAHA supporters cite vaccines and medical choice as their reason for supporting the movement. Few MAHA supporters specifically express support for President Trump or HHS Secretary Robert F. Kennedy Jr. (2%) as their reasoning for supporting the movement.

In Their Own Words: What is the Main Reason You Support the MAHA Movement?

“It is morally correct. We don’t want to poison our kids with vaccines they don’t need. We don’t want to eat food that leads to morbidity to make companies’ profit margins higher,” 43-year-old Republican man, Pennsylvania

“America uses far too much harmful ingredients that most other countries ban,” 28-year-old independent man, Indiana

“To get people healthier so taxpayers don’t have to pay for their health care,” 58-year-old Republican woman, Kentucky

“We should be promoting healthier lifestyles in the country,” 29-year-old Republican woman, Iowa

“The MAHA movement gives patients more freedom to choose the doctors they actually want to see…While I support it for now, I’ll be waiting to see how these policies are actually implemented,” 39-year-old independent man, Washington

“It’s about making the next generation healthy,” 27-year-old independent woman, Arizona

“I followed Kennedy before he was in office and I’m hoping that he will continue with what he stood for before,” 51-year-old independent woman, Tennessee

“Health care should be a right,” 65-year-old Democratic man, New York

Where MAHA Concerns Resonate With the Public: Food Safety, Pesticides, and Industry Influence

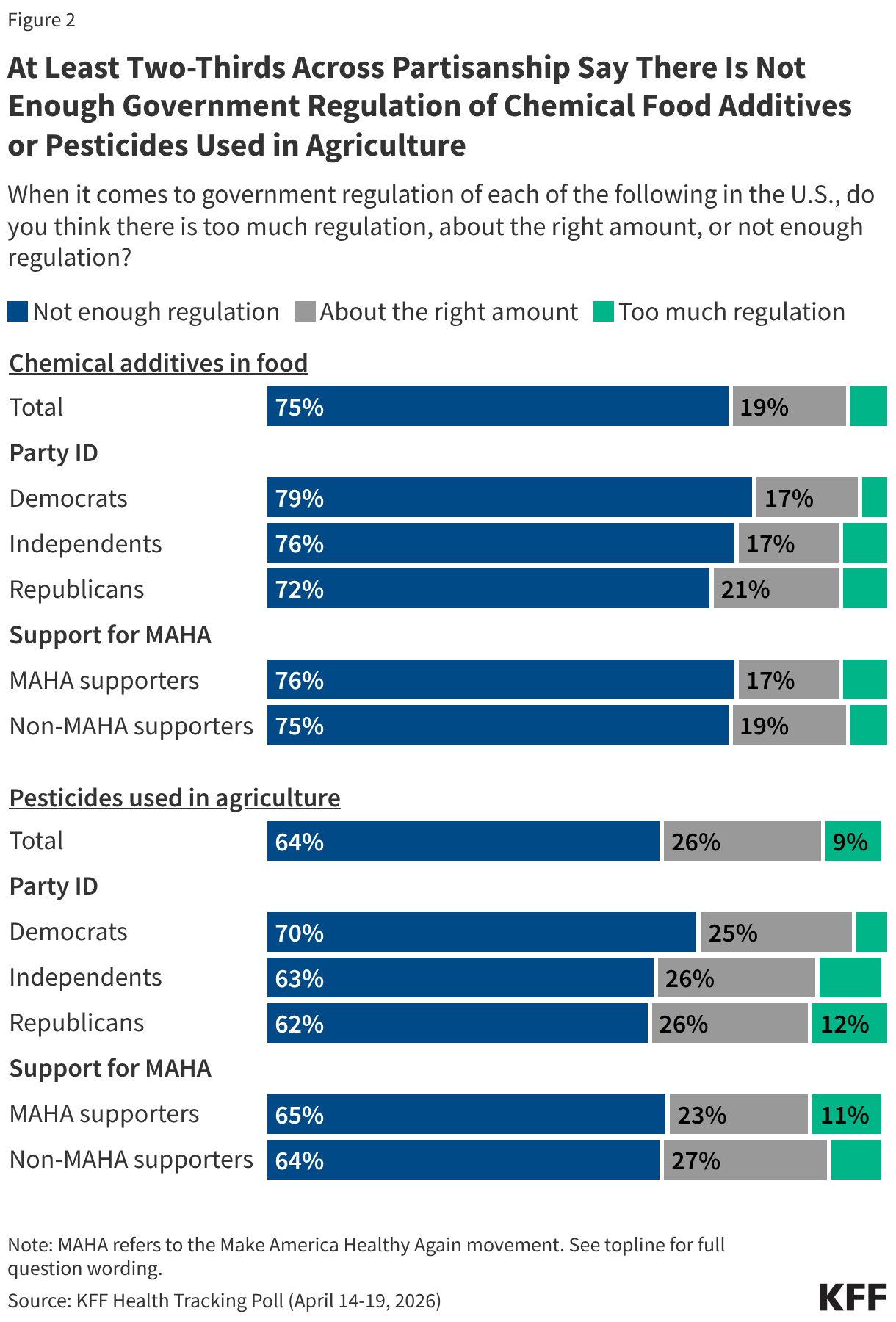

Among the public, there is broad, bipartisan agreement that there is not enough government regulation of chemical additives in food and pesticides in agriculture in the U.S. Three-quarters of adults say there is not enough government regulation of chemical food additives, and about two-thirds (64%) say the same about pesticides used in agriculture. Majorities across partisan lines and among both MAHA supporters and those who do not support the movement agree, suggesting this is an area where MAHA’s concerns align with broader public sentiment.

Some food industry groups and public health experts have argued that restrictions on approved food ingredients could limit access to affordable groceries for families in the U.S. When those who originally said there is “not enough regulation” of chemical additives in food or pesticides used in agriculture are presented with the caveat that increased regulation could lead to higher food prices for consumers, most still support increased regulation. But the possibility of increased costs does move some people. The share saying there is not enough regulation of food additives drops by 13 percentage points after hearing that increased regulation could increase costs (from 75% to 62%), with a similar drop in the share who maintain that there is not enough regulation of pesticides (from 64% to 52%).

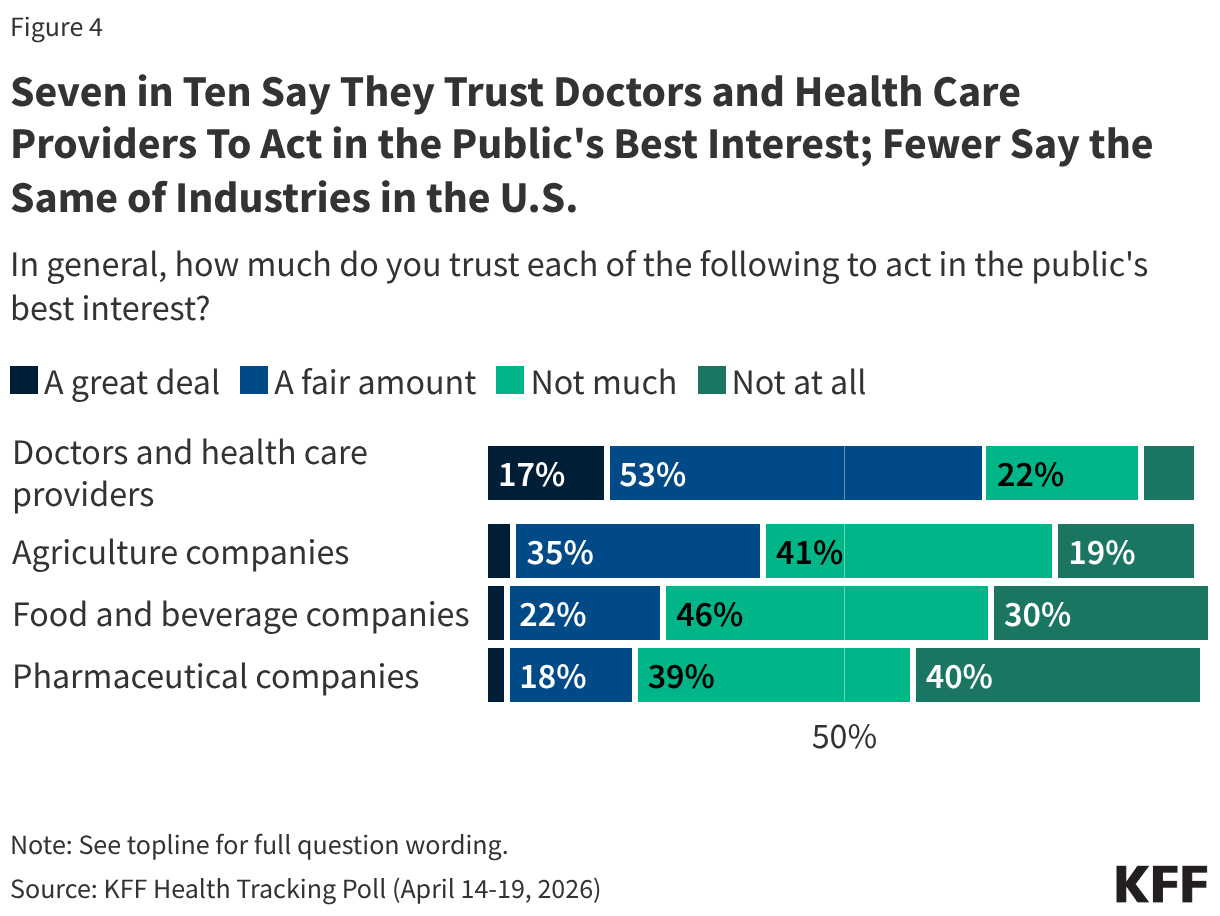

The public perception that there is not enough regulation may be rooted in broader skepticism toward the industries themselves. Most U.S. adults do not trust pharmaceutical companies, food and beverage companies, or agricultural companies to act in the public’s best interest. One in four or fewer adults say they trust food and beverage companies (25%) or pharmaceutical companies (21%) “a great deal” or “a fair amount” to act in the public’s best interest, while a somewhat larger share (40%) trust agricultural companies on this measure. Very small shares – fewer than 5% – trust each of these groups “a great deal” to act in the public’s best interest.

By contrast, seven in ten adults say they trust doctors and health care providers at least “a fair amount” to act in the public’s best interest.

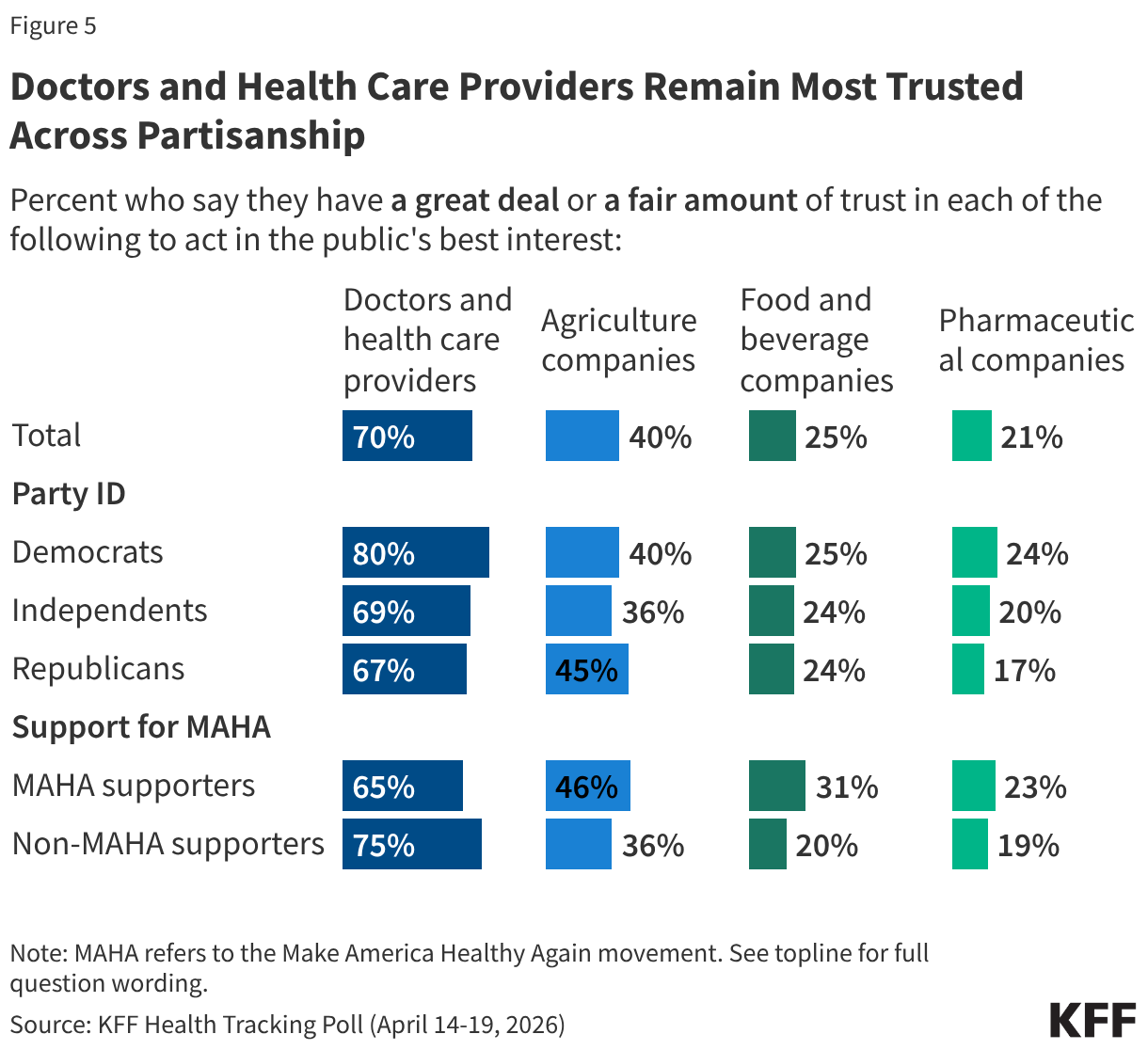

Across partisanship, and among those who do and do not support the MAHA movement, fewer than half trust agricultural companies, food and beverage companies, or pharmaceutical companies to act in the public’s best interest. However, most Democrats (80%), independents (69%), and Republicans (67%) have a great deal or a fair amount of trust in doctors and health care providers to act in the public’s best interest.

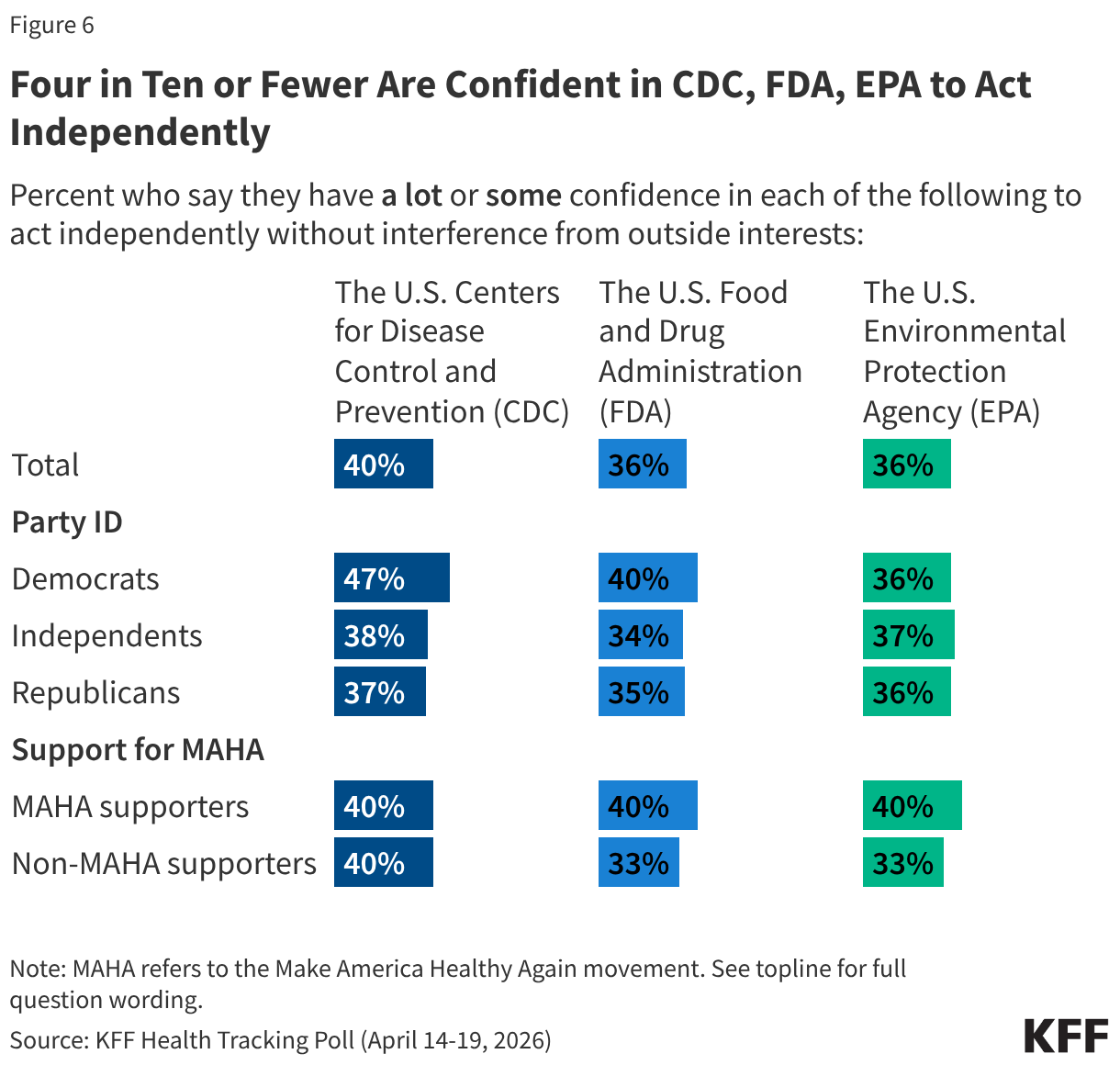

Confidence in the government agencies with major responsibilities for food safety and public health is low across partisans. Four in ten or fewer adults say they have “a lot” or “some” confidence in the U.S. Centers for Disease Control and Prevention (CDC) (40%), U.S. Food and Drug Administration (FDA) (36%), or the U.S. Environmental Protection Agency (EPA) (36%) to act independently without interference from outside interests. Democrats are slightly more likely than Republicans or independents to express confidence in the CDC (47% vs. 37% and 38%, respectively), but partisan differences largely disappear when it comes to confidence in the FDA and EPA.

U.S. adults who support the MAHA movement and those who do not are similarly skeptical. Four in ten MAHA supporters say they are confident in each of these agencies to act independently, leaving six in ten MAHA supporters who have “a little” or “no confidence at all.”

MAHA and Other Health Care Issues in the Election

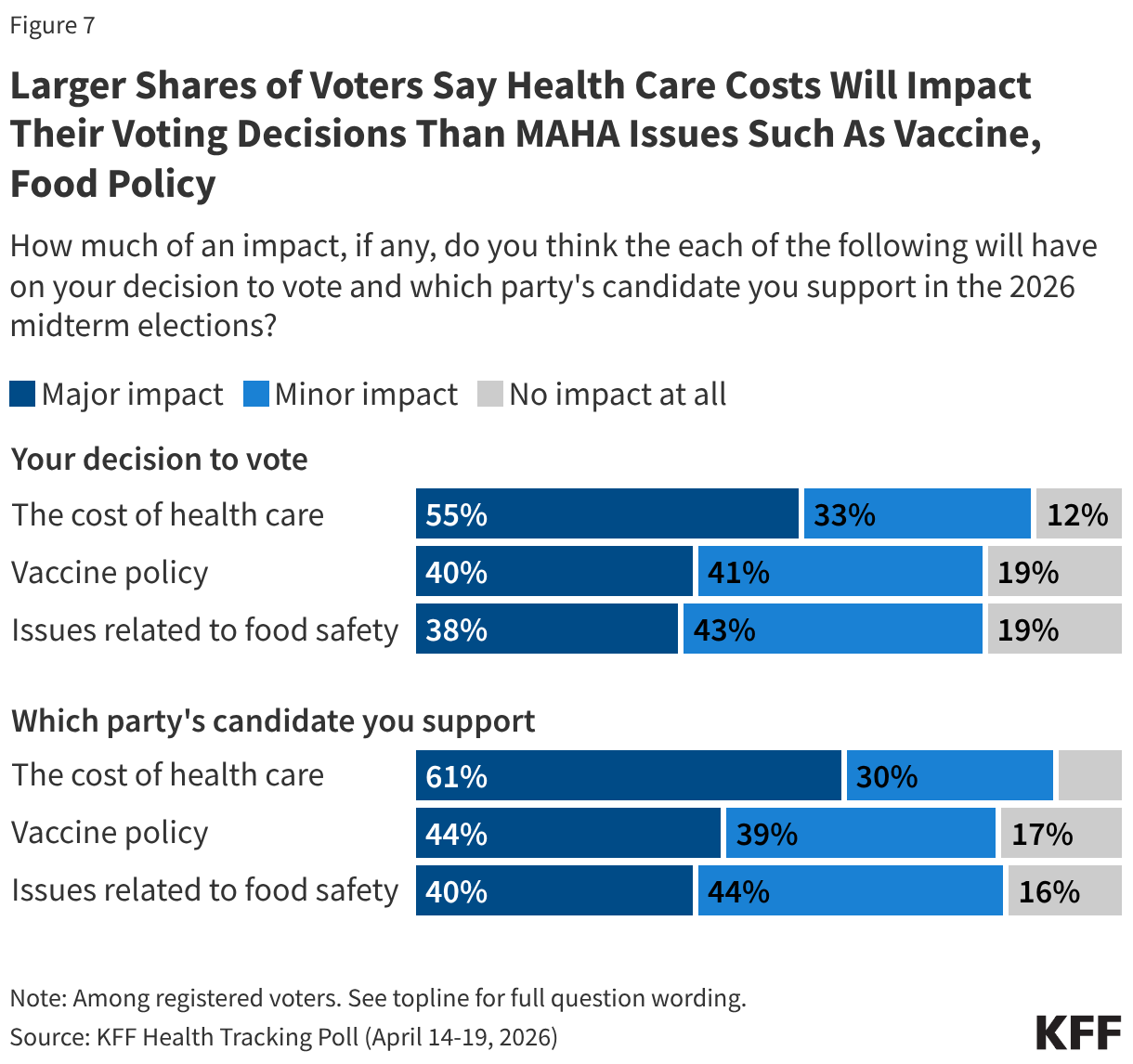

Despite the resonance of these issues elevated by the MAHA movement, health care costs overshadow these concerns for voters heading into the 2026 midterm elections. Previously released findings from the April 2026 KFF Health Tracking Poll show health care costs remain a primary economic concern for the public. Reflecting that, costs are voters’ top health concern heading into the 2026 midterm elections, outweighing policy areas elevated by the MAHA movement, such as vaccines or food safety.

More than half of voters say health care costs will have a “major impact” on their decision to vote (55%) or which party’s candidate they will support (61%). When it comes to vaccine policy and food policy, about four in ten voters say these issues will have a “major impact” on their decision to vote or which party’s candidate they will support, at least 15 percentage points lower than the share who say the same about health care costs.

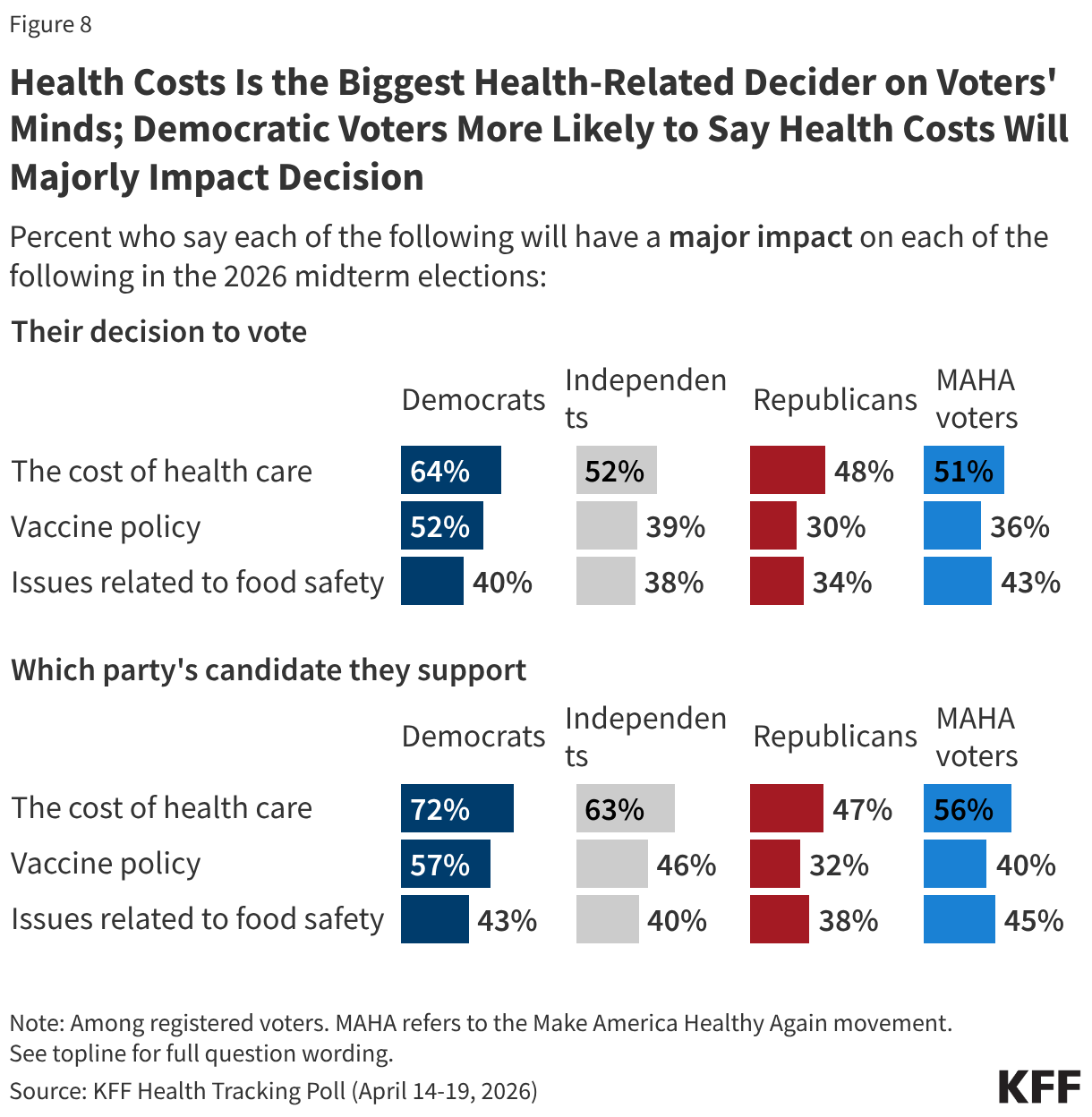

While the issue of health costs is more salient for Democratic voters than for Republicans, larger shares across partisans say health costs will have a major impact on their voting decisions than say the same about vaccine policy or food safety. For example, about half of independent voters (52%) say health care costs will have a major impact on their decision to turn out in November, compared to about four in ten who say the same about vaccine policy (39%) and food safety (38%). Patterns are similar for Republican voters (48%, 30%, and 34%, respectively) and Democratic voters (64%, 52%, and 40%, respectively).

Among voters who say they support the MAHA movement – a majority (56%) of whom identify as MAGA Republicans – at least half say the cost of health care will have a major impact on their decision to vote (51%) or which party’s candidate they support (56%). Despite the MAHA movement elevating issues such as vaccine and food safety, fewer MAHA voters – about four in ten – say vaccine policy or issues of food safety will majorly impact their voting decisions.

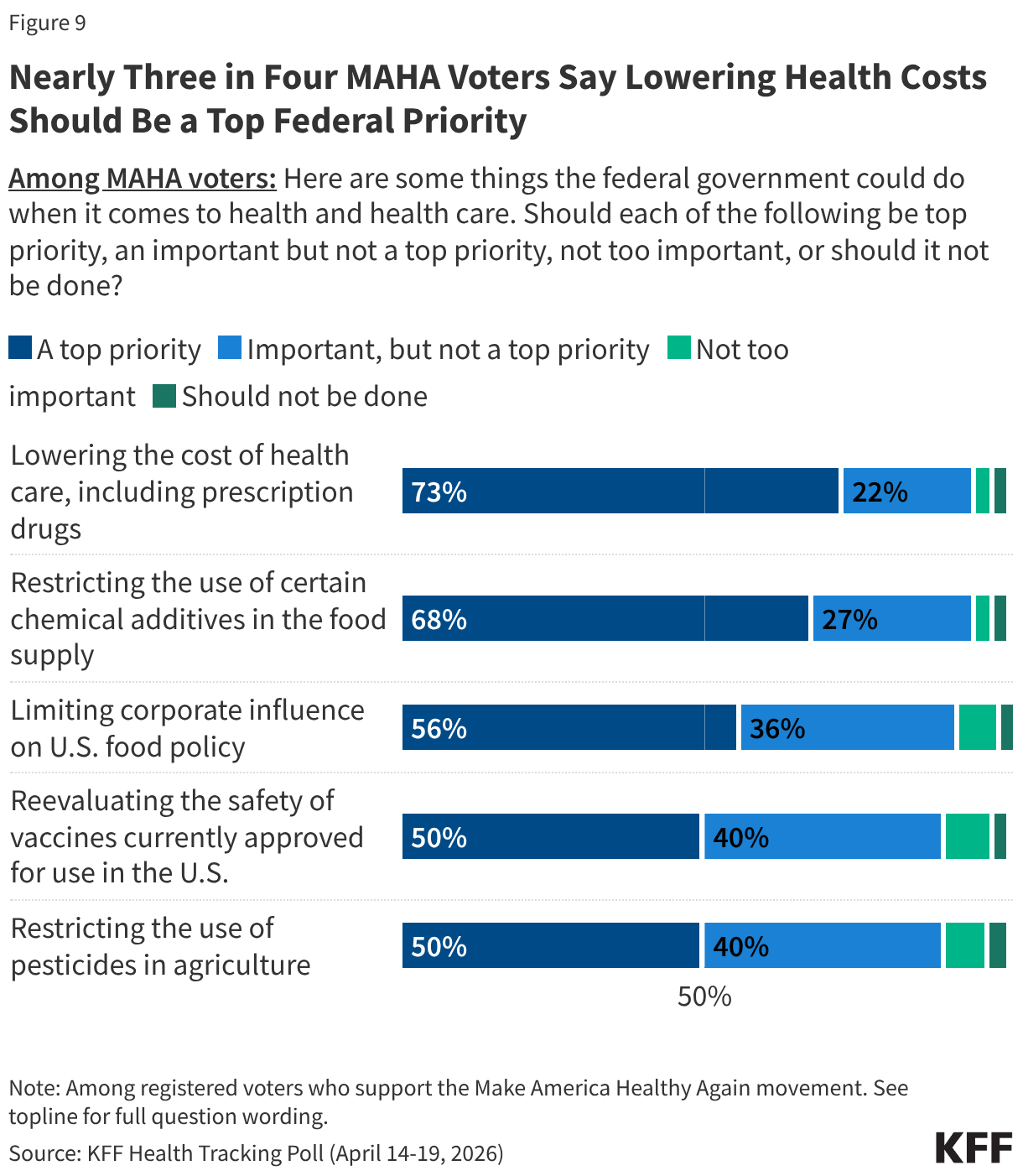

MAHA-supporting voters express broad enthusiasm for federal action across the movement’s core agenda, but once again, health care costs remain the dominant priority. Nearly three-quarters of MAHA voters (73%) say lowering the cost of health care, including prescription drugs, should be a top priority for the federal government. This is followed by restricting the use of certain chemical additives in the food supply (68%) and limiting corporate influence on U.S. food policy (56%). Half of MAHA voters say reevaluating the safety of vaccines currently approved for use or restricting the use of pesticides in agriculture should be top priorities. Across all five items, one in ten or fewer MAHA voters say any of these efforts are “not too important” or “should not be done.”

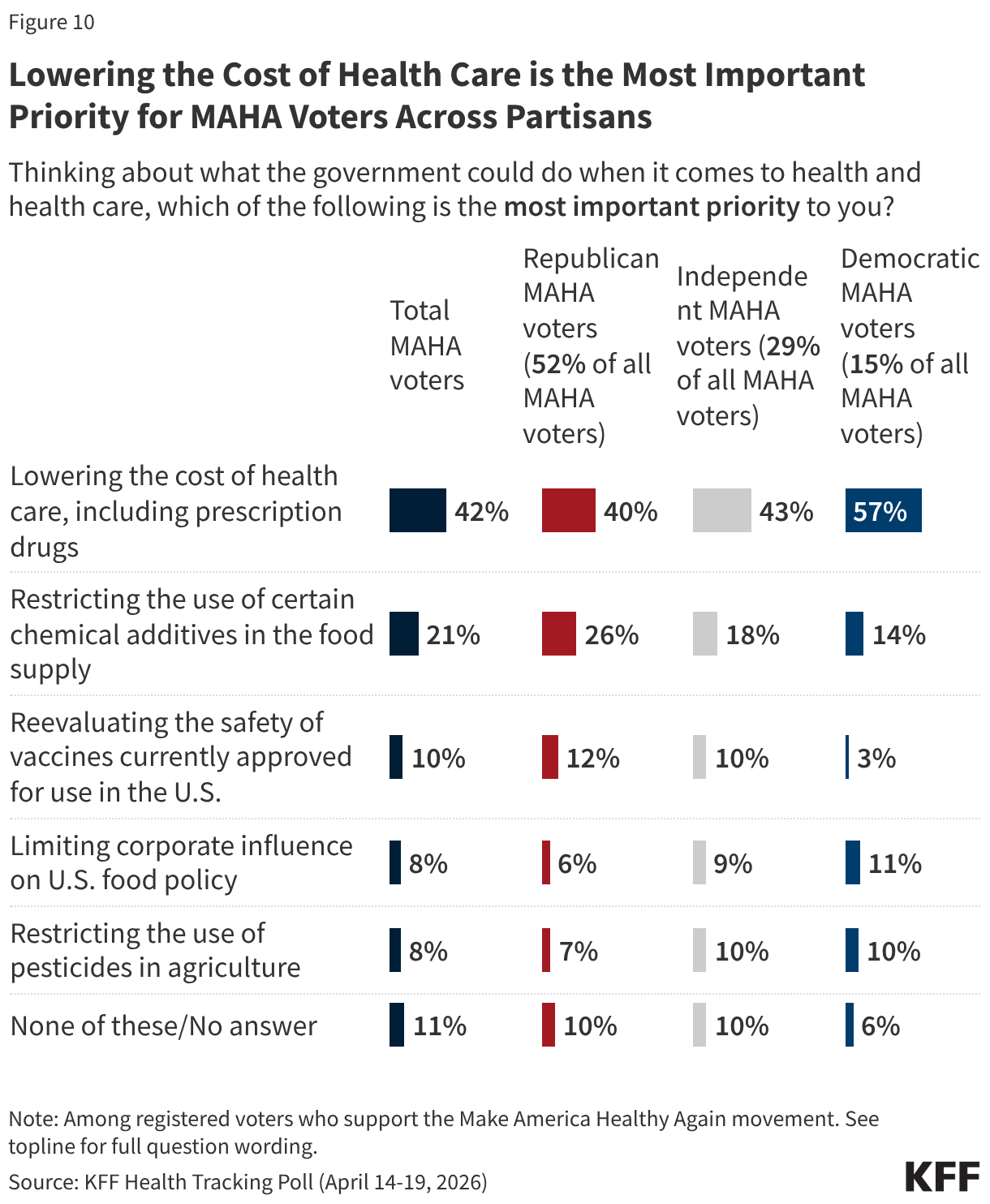

When asked to choose the single most important health priority to them, about four in ten MAHA-supporting voters (42%) choose lowering the cost of health care, including prescription drugs—twice the share who say the same of restricting chemical additives in the food supply (21%). Fewer cite reevaluating vaccine safety (10%), limiting corporate influence in U.S. food policy (8%), or restricting pesticide use in agriculture (8%) as their single top priority.

The cost of health care tops the list of health care priorities for MAHA voters regardless of partisanship. Among voters who support the MAHA movement, six in ten Democrats (57%) and four in ten independents (43%) and Republicans (40%) say lowering the cost of health care is the most important priority. For each of these groups, health care costs rank at least 14 percentage points ahead of restricting the use of chemical additives in food, and even further ahead of issues like reevaluating vaccine safety and restricting pesticide use.

Trump Administration Approval and Party Preference on MAHA Health Issues

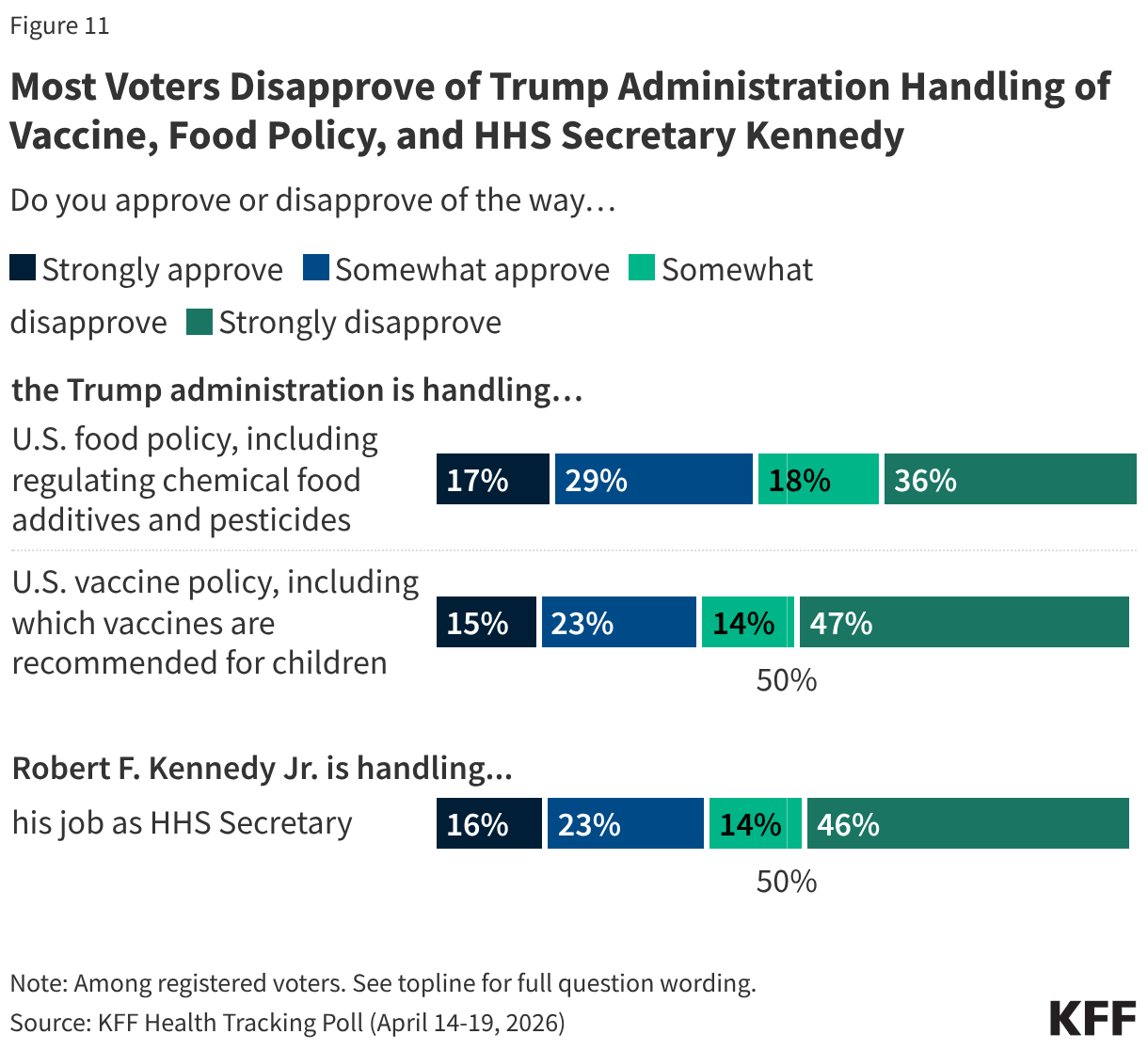

Voters give the Trump administration low approval ratings on two key policy areas elevated by the MAHA movement. Just under half (46%) of voters approve of the administration’s handling of food policy, and a larger share (54%) disapprove. Just a few months after the changes made to the childhood vaccine schedule by HHS, about four in ten voters approve of the administration’s handling of U.S. vaccine policy (38%) and six in ten (61%) disapprove, including about half (47%) who “strongly disapprove.”

As the head of the MAHA Commission and Secretary of Health and Human Services, Robert F. Kennedy Jr. is the spokesperson for many of the administration’s federal health policies. About four in ten voters say they approve of the way Secretary Kennedy is handling his job (39%) and six in ten disapprove, including nearly half (46%) who “strongly disapprove.”

Unsurprisingly, voters are split along partisan lines, with the Trump administration receiving high approval ratings from Republicans on food and vaccine policy as well as Secretary Kennedy’s handling of his job at HHS, and most Democrats disapproving.

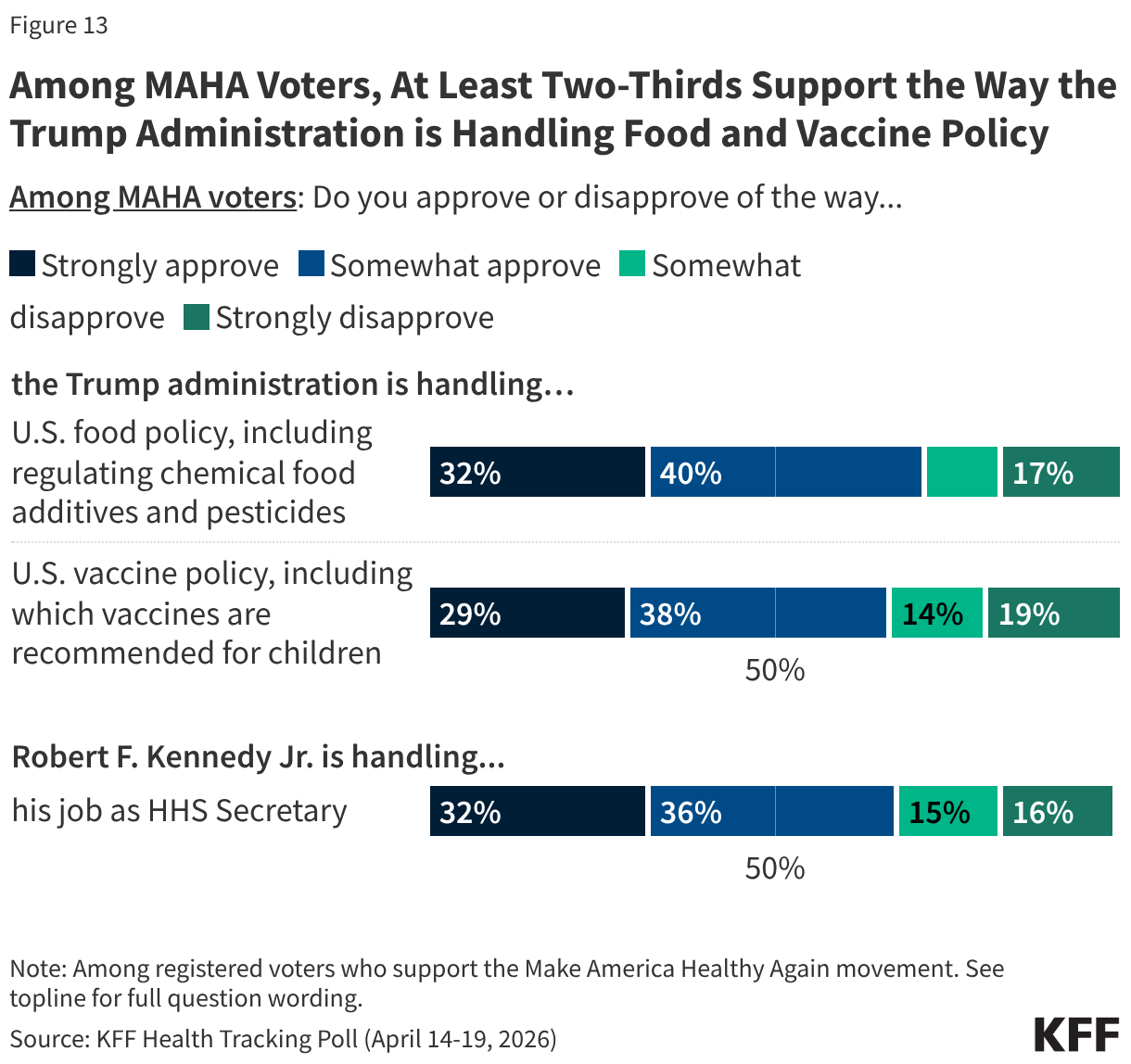

Despite Secretary Kennedy’s leadership at HHS and recent changes focused on MAHA priorities, approval of the administration’s handling of issues like vaccine policy is far from unanimous among the movement’s supporters. About seven in ten MAHA voters approve of the administration’s handling of food policy (72%) and vaccine policy (67%), and Secretary Kennedy’s handling of his job as Health Secretary (69%). On each of these areas, just a third “strongly” approve of the administration and a similar share disapprove: tepid ratings for a group that aligns with Kennedy’s signature movement.

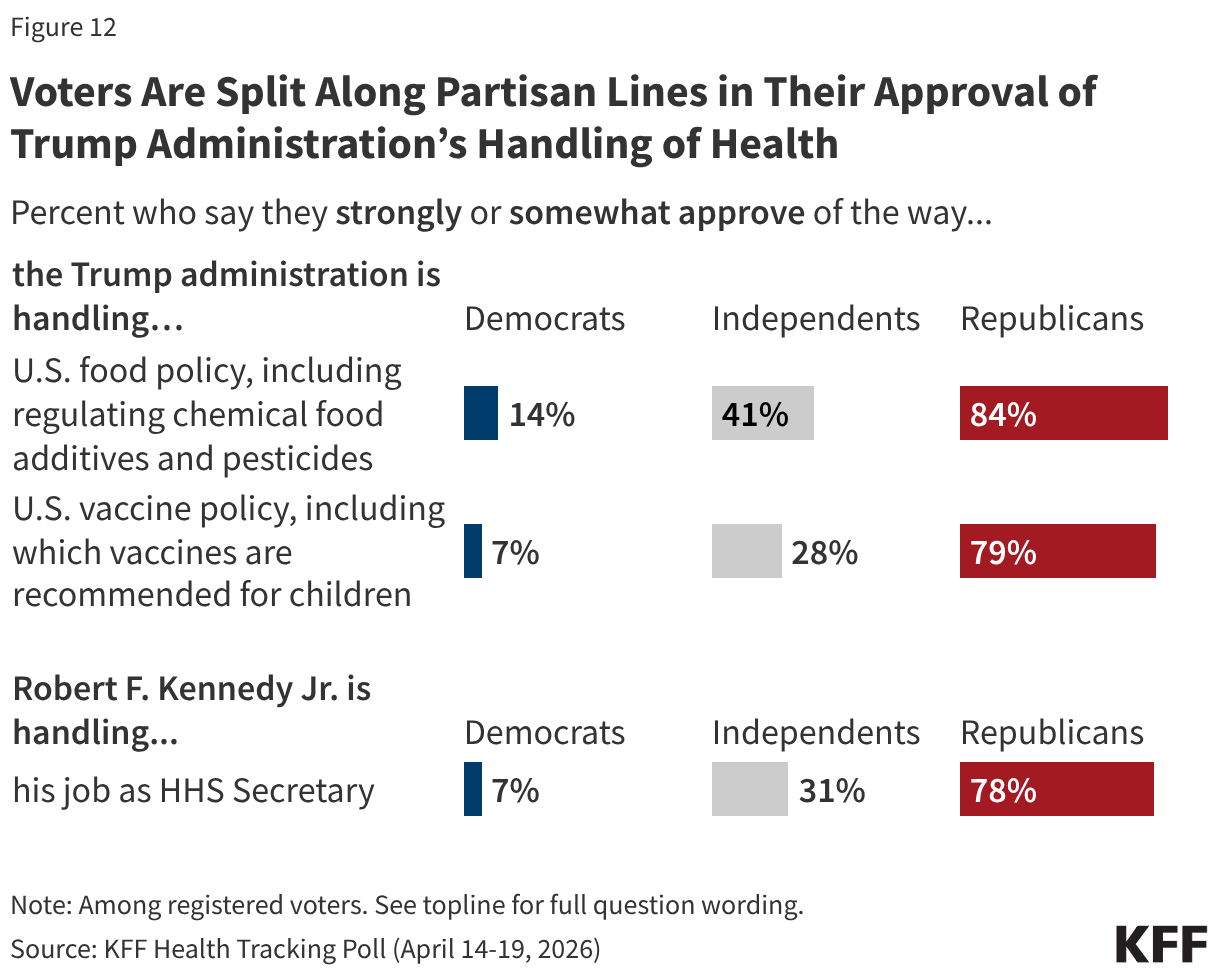

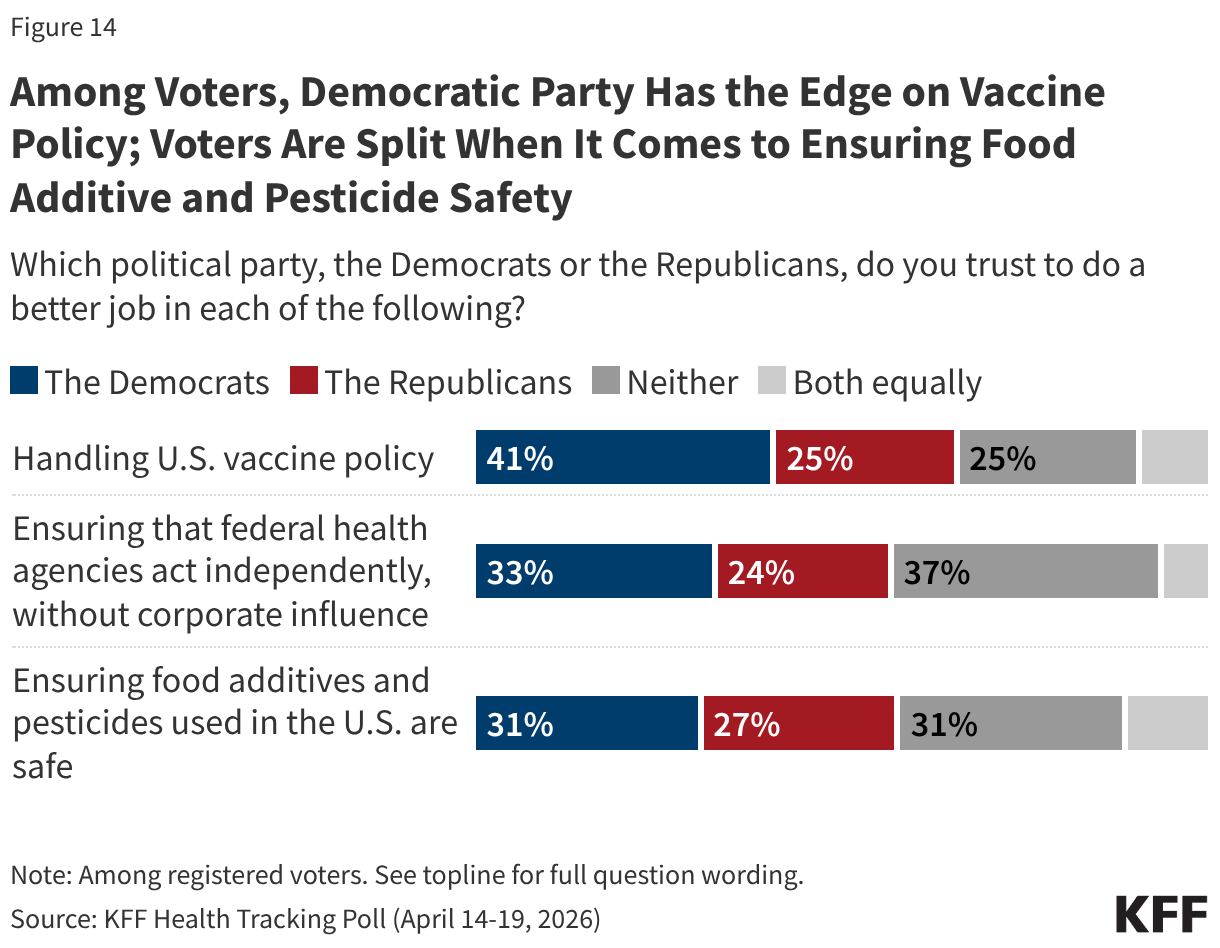

With about six months until the 2026 midterm elections, the Democratic Party has a strong edge over the Republican Party when it comes to who voters trust to address vaccine policy, and a narrower edge on ensuring federal agencies act independently. Voters are split over who they trust to do a better job ensuring food additives are safe. Democrats have a double-digit advantage over Republicans when it comes to who voters trust to handle vaccine policy (41% vs. 25%). While the Democratic Party has a smaller advantage among voters on which party they trust to ensure that federal health agencies act independently without corporate influence (33% vs. 24%), nearly four in ten (37%) say they trust “neither party.”

Similar shares of voters say they trust the Democratic Party (31%), the Republican Party (27%), or “neither party” (31%) more when it comes to doing a better job ensuring food additives and pesticides in the U.S. are safe.

MAHA Health Concerns Resonate Broadly but Lag Behind Health Care Costs Even for MAHA Voters

rewrite this content and keep HTML tags

Chemical food additive and pesticide concerns associated with the Make America Health Again (MAHA) movement are shared broadly across the public. But when it comes to voters, health care costs are a higher priority and bigger motivator, even among MAHA supporters, a new KFF Health Tracking Poll finds.

When asked to identify their most important health priority for government to address, far more MAHA-supporting voters identify lowering the cost of health care (42%) than other issues more closely associated with the movement, such as restricting the use of chemical additives in the food supply (21%), reevaluating the safety of vaccines (10%), limiting corporate influence on food policy (8%), or restricting the use of pesticides in agriculture (8%).

At least half of MAHA voters also say that the cost of health care will have a “major impact” on their decision to vote (51%) and which party’s candidate they will support (56%) in the upcoming midterms. That’s more than say the same about vaccine policy (36% say it will impact their decision to vote, 40% say it will impact which candidate they will support) or food safety (43% say it will impact their decision to vote, 45% say it will impact which candidate they will support), two issues closely aligned with MAHA, a movement promoted by the Trump administration and by Health and Human Services (HHS) Secretary Robert F. Kennedy Jr.

Overall, about four in ten (41%) adults—and a similar share of voters (43%)—say they are supporters of the MAHA movement, with support closely tied to partisanship and support of President Trump’s Make America Great Again (MAGA) movement.

Among voters who support MAHA, about half (52%) identify as Republicans, 29% identify as independents, and about one in seven (15%) identify as Democrats. A majority (56%) of MAHA voters identify as Republican or Republican-leaning and support the MAGA movement. The pattern of prioritizing health costs ahead of other MAHA issues is consistent across these partisan subgroups.

Other MAHA Health Concerns Are Shared by the Broader Public

Majorities of the public say there is not enough regulation of chemical additives in food (75%) or of pesticides used in agriculture (64%)—including majorities across partisans, among MAHA supporters, and those who do not support the movement.

Most of the public—across partisans and MAHA supporters—also share a distrust of federal health agencies and food and drug industries:

- Four in ten or fewer adults say they have at least some confidence in the U.S. Centers for Disease Control and Prevention (CDC: 40%), the U.S. Food and Drug Administration (FDA: 36%), or the U.S. Environmental Protection Agency (EPA: 36%) to act independently without interference from outside interests. Democrats are more likely than Republican or independent adults to trust the CDC, but partisan differences largely disappear for the FDA and EPA.

- Less than half of U.S. adults trust agricultural companies (40%), food and beverage companies (25%), or pharmaceutical companies (21%) to act in the public’s best interest. Low levels of trust in these industries are also present across partisans.

About 1 in 3 MAHA Voters Strongly Approve of HHS Secretary Kennedy’s Job Performance

MAHA voters approve more than other voters of how the Trump administration is handling food policy, including chemical additives and pesticides (72% vs. 27%), and vaccine policy (67% vs. 17%), as well as how HHS Secretary Robert F. Kennedy Jr. is handling his job (69% vs. 17%). However, less than one-third of MAHA voters “strongly approve” of the Trump administration on food policy (32%) and vaccine policy (29%) and of the HHS Secretary’s handling of his job (32%)—while similar shares of MAHA voters disapprove in all three areas. This is a fairly tepid rating for a group that aligns with Kennedy’s signature movement.

Overall, voters are evenly divided on whether they trust Democrats (31%) or Republicans (27%) to handle the safety of food additives and pesticides, and a similar share (31%) gives neither party the advantage on this issue. Meanwhile, the Democratic Party holds the advantage over the Republican Party in who voters trust to handle vaccine policy (41% vs. 25%) and ensure that federal health agencies act independently without corporate influence (33% vs. 24%).

Designed and analyzed by public opinion researchers at KFF, this survey was conducted April 14-19, 2026, online and by telephone among a nationally representative sample of 1,343 U.S. adults in English and in Spanish. The margin of sampling error is plus or minus three percentage points for the full sample. For results based on other subgroups, the margin of sampling error may be higher.

Reaching Voters on Health | KFF

rewrite this content and keep HTML tags

As we inch closer to the midterms, our latest tracking poll shows that health care costs have some staying power as a voting issue, hanging in as a top voter concern, tied with gas prices as the number one economic worry, even as gas prices have soared with the Iran war and are in the news every day. That says a lot about the salience of health care costs as an issue right now. I had expected gas prices to take the top spot decisively, at least temporarily.

But candidates have to capitalize on voters’ worries to make them matter in elections. Another question in our poll provides clues about how best to do that, and it’s not what I expected it to be (more on that below).

The first and most basic thing is simply for candidates to talk about health care costs a lot. In case you take this for granted, I recently watched a televised debate between California’s candidates for governor. It featured three advocates for single-payer health care—always a controversial debate topic—including a former Secretary of Health and Human Services. Surprisingly, health and health care costs, the voter’s top economic concern according to polls, weren’t mentioned once by the moderators or the candidates themselves.

But health care will get airtime in the midterm campaigns. This is another area where our survey findings weren’t what I expected: My assumption was that the single most important thing for candidates to do was to show voters that they care about, and can relate to, the struggles they have paying for health care. Candidates do this a lot, talking about their family experiences with illness and health care costs and telling stories about people they met on the campaign trail. No doubt that registers, but according to our poll, it may not be the most important thing to do.

Voters said what matters most to them is to see candidates show some “fight” by taking on the big health care interests they have come to see as villains. Thirty-six percent said “what matters most to them” about candidates is their willingness “to take on drug and insurance companies.” (The poll doesn’t tell us how much the voters value rhetoric versus substantive proposals that would have consequences.)

After that, voters also wanted to have some confidence that candidates would deliver something. Thirty-three percent want to know that they “have a plan to address health care costs.” That doesn’t tell us a lot about whether the plan has to be sweeping or small and tangible, or what voters mean by “having a plan.”

Then, coming in third, 21% said they want to see that candidates “care about the problems people are having with their health care costs.” Democrats are a little bit more into candidates showing empathy, at 25% v. 17% for Republicans.

And then 10% said none of these, presumably looking for something else.

I wouldn’t make too much of the distinctions between these perceived candidate virtues. After all, showing “fight” and taking on big interests are also forms of showing you care. And voters always say they want to see a “plan,” then most tune out the details, as if having a plan is more important than the plan itself. Poll respondents may also think that having a plan is something they should say to pollsters. The news media also pushes candidates for plans they then dissect, while candidates try to keep their intentions general. And stakeholder groups push for plans to advance their goals. However, as any political adviser knows, candidates are best off with general plans that signal direction and values and are plausible, but don’t have enough detail to attack. It’s not clear that voters crave detailed plans, but they do want a sense that candidates will “do something,” and maybe also that the “something” won’t hurt them or upset their own current health care arrangements (long a red line for health reform).

What jumped out from the poll is the value voters place on villainizing health care’s big interests now. It’s like serving up a big fat slow curveball for every candidate to hit. And the polling makes sense at this moment. Once the territory of the left, even President Trump has been taking on drug and insurance companies, ending this as a no-fly zone for Republicans. (Hospitals, where much of health spending is, so far have remained relatively safe).

Of course, candidates also know that health care’s big interests won’t just sit there and take it; they will respond with political contributions to their opponents if they believe a candidate, if elected, might do something that damages their interests, or that their rhetoric and agenda-setting power might add momentum to actions they want to block. The polling may foreshadow growing candidate courage to take on health care’s big interests that we’ll see unfold in this election cycle, but not necessarily a change in how the system works.

KFF Health Tracking Poll: Health Care Costs and the Midterms

rewrite this content and keep HTML tags

Key Takeaways

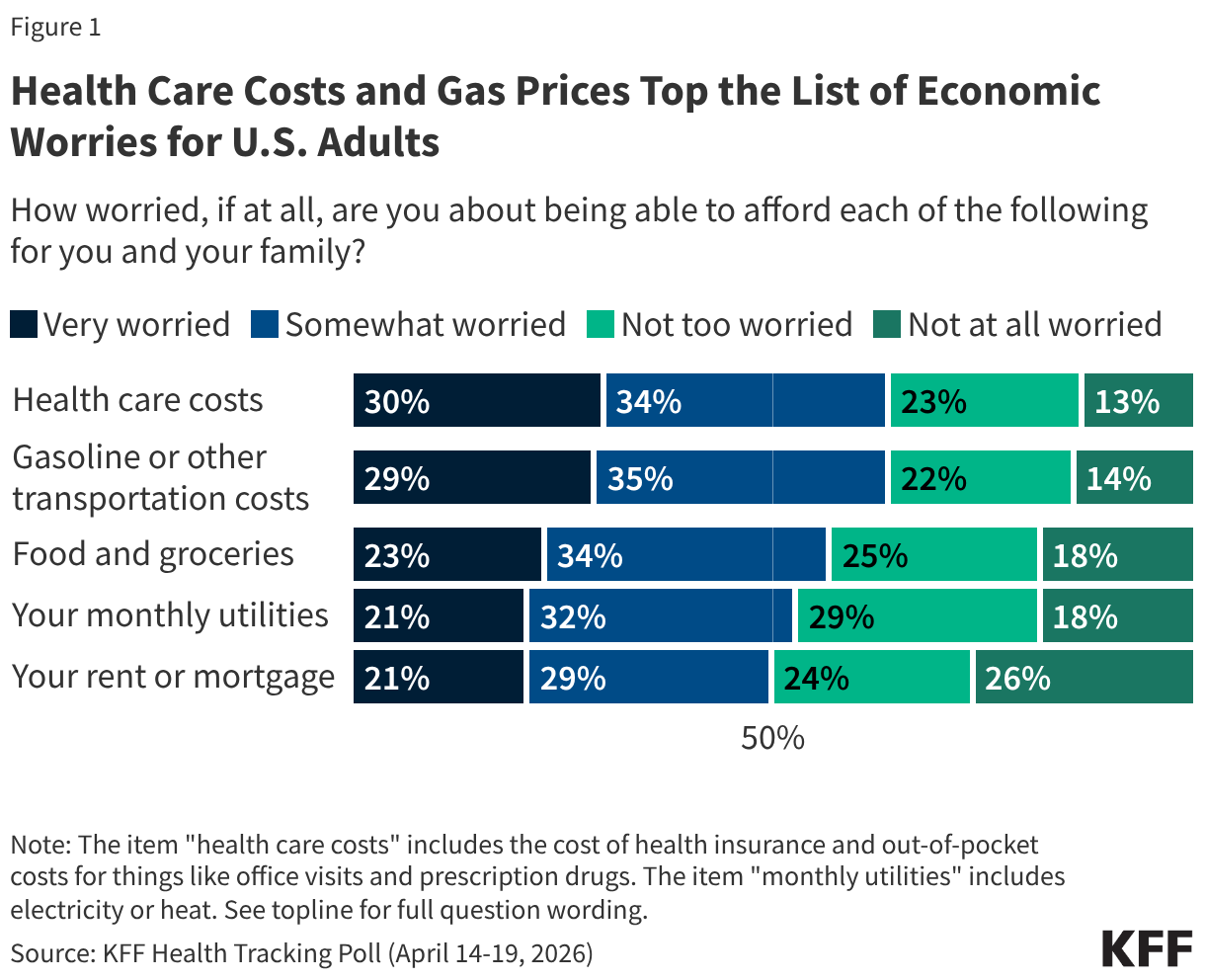

- Health costs continue to top the public’s list of affordability worries, even as concerns about gas prices have risen in recent weeks. Nearly two-thirds (64%) of adults are worried about being able to afford health care costs, on par with the share who now worry about gas and transportation costs (64%) and outranking other economic concerns. In January 2026, prior to the start of the U.S. conflict with Iran, gasoline and transportation costs ranked at the bottom of household financial worries. Now, gas prices share the top spot with health care costs as the biggest financial worry adults face for themselves and their families.

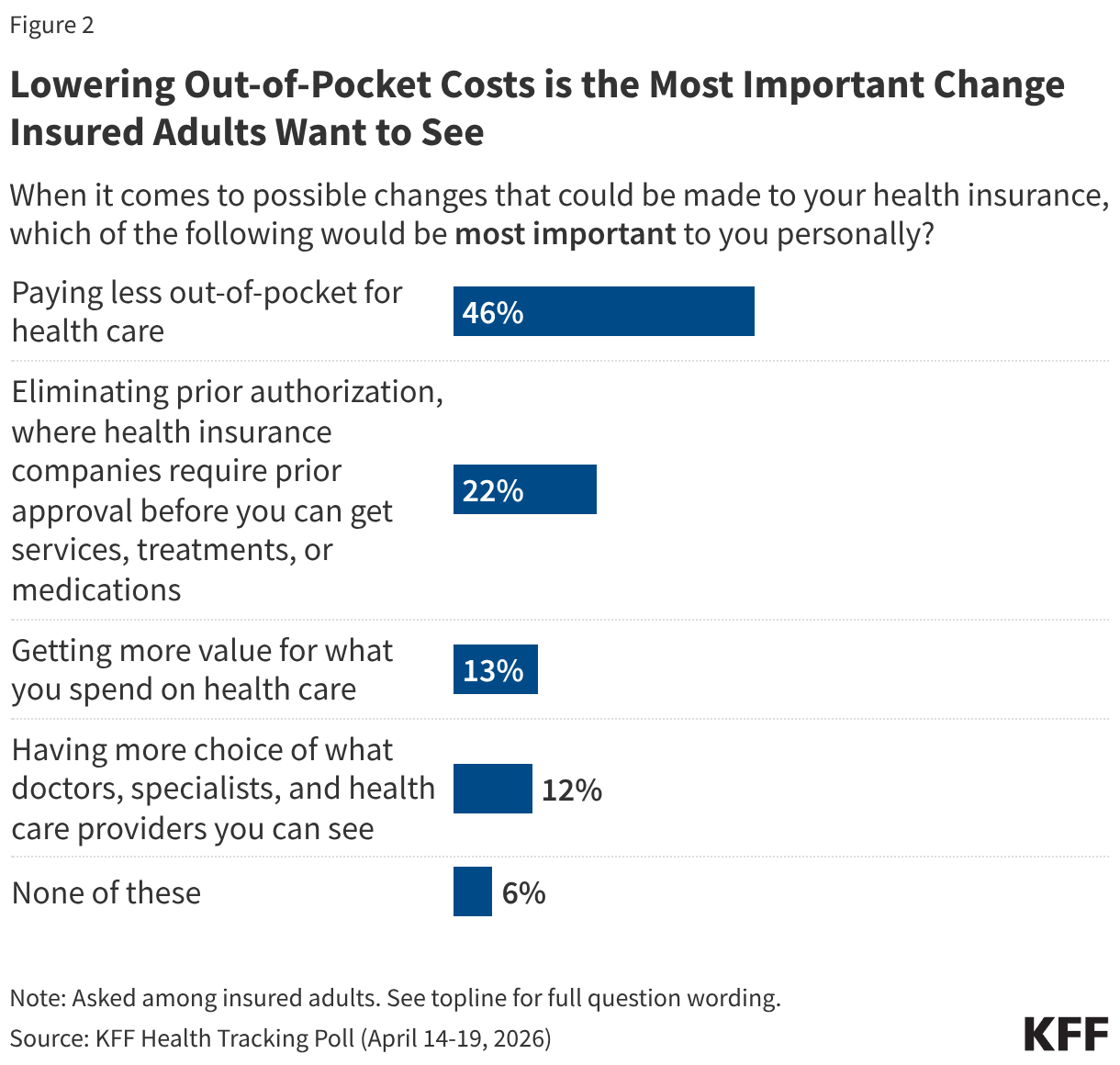

- Lowering out-of-pocket costs ranks as the most important change insured adults say they would like to see from their health insurance. When given a list of possible changes that could be made to their health insurance, half (46%) of insured adults choose lowering their out-of-pocket costs as most important, more than twice the share who cite eliminating prior authorization (22%). Fewer say other possible changes such as getting more value for what they spend (13%) and having more choice in providers (12%) would be most important to them.

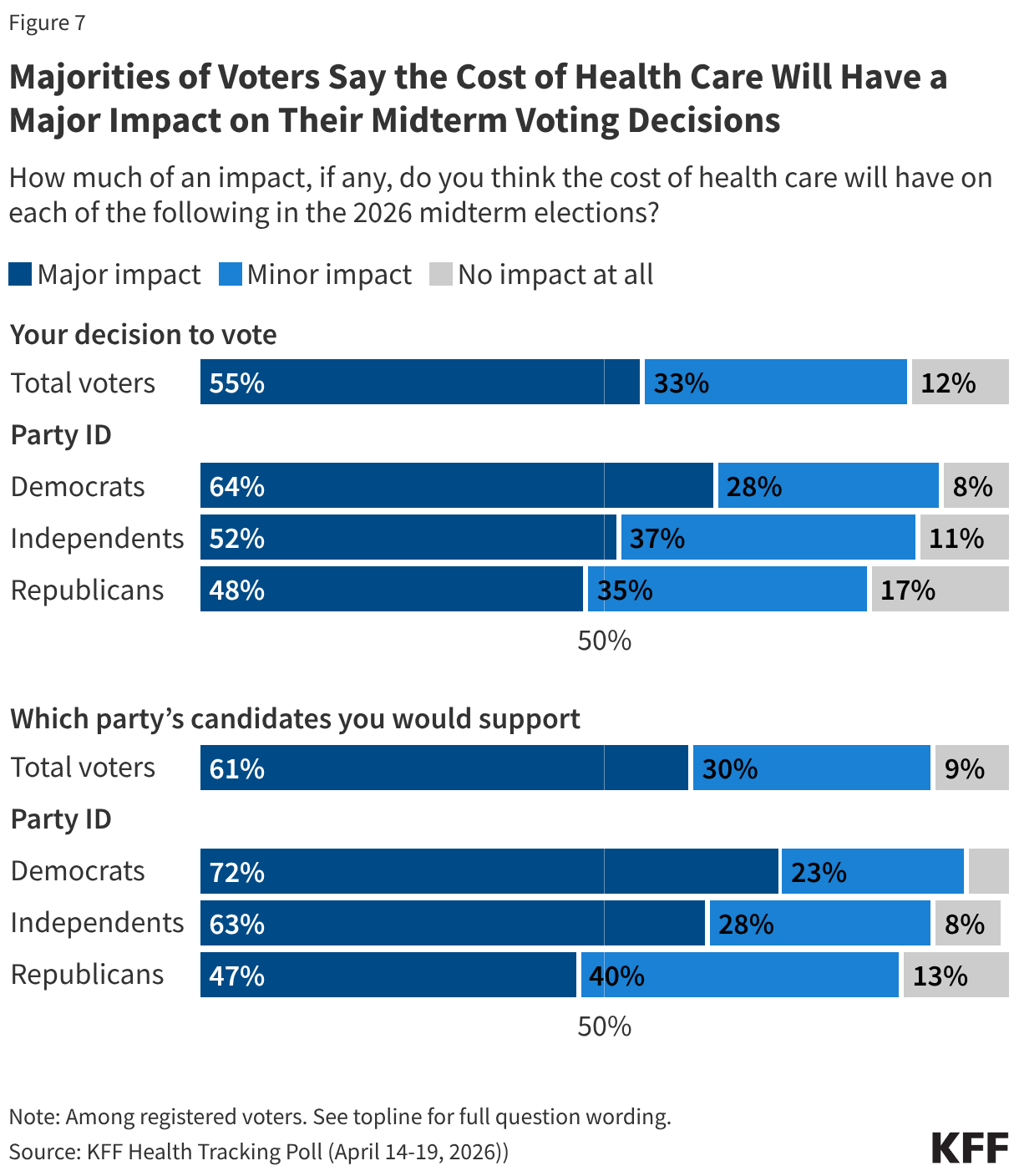

- Health costs also loom large in the upcoming midterm elections. About nine in ten voters say the issue will influence their decision to vote and who to vote for in the 2026 midterm elections, with majorities saying it will have a “major impact” on both areas (55% and 61%). While majorities of voters across partisans say health care costs will impact their vote in November, the issue is more salient among Democratic and independent voters. About seven in ten Democratic voters (72%) and nearly two-thirds of independent voters (63%) say health care costs will impact which party’s candidate they would support in the election, compared to about half of Republican voters (47%) who say the same.

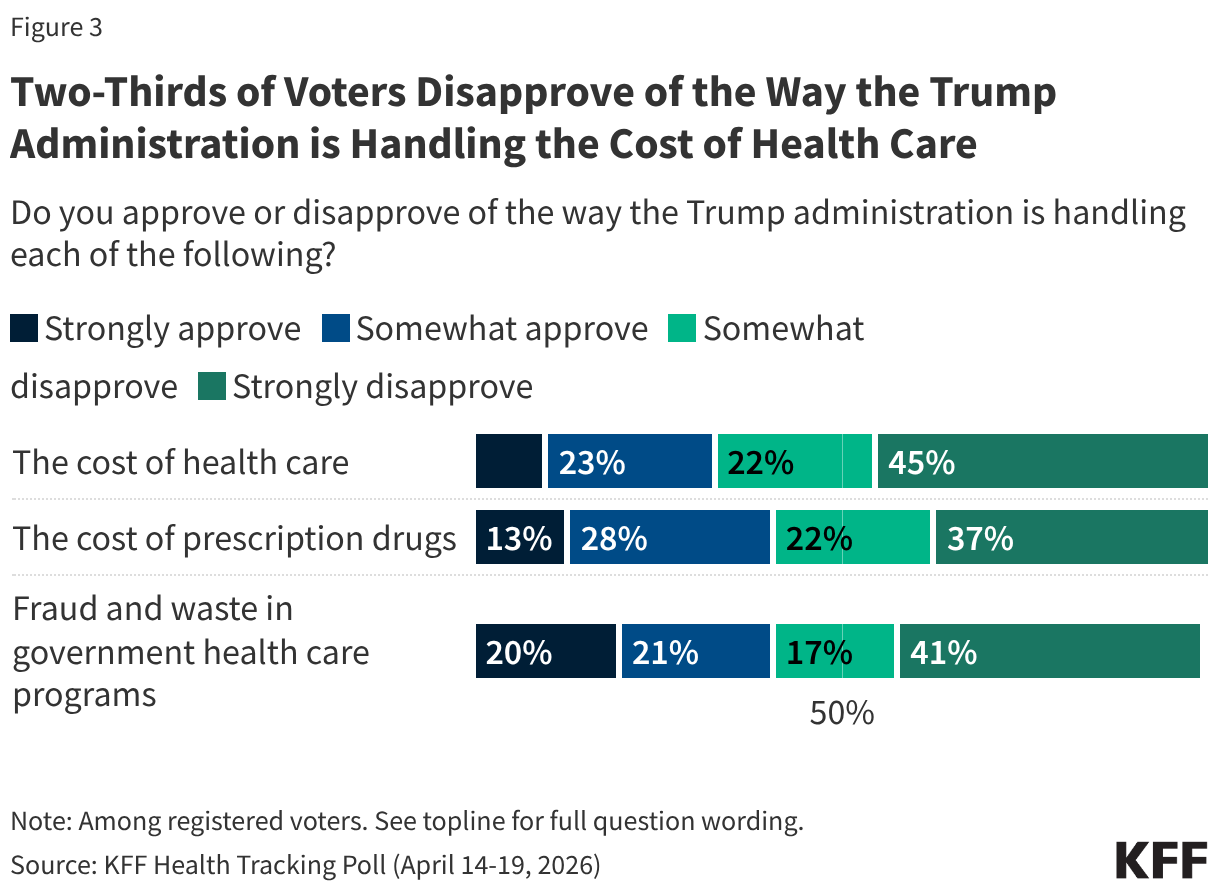

- While both political parties have made recent announcements about their own plans to bring down health costs, the latest polling shows the Democrats currently have the edge among voters. Voters give the Trump administration low approval ratings on its handling of the cost of health care and are more likely to trust the Democratic Party (37%) over the Republican Party (26%) on addressing this issue. Fewer than half of voters approve of the administration’s handling of cost of health care (33%) and the cost of prescription drugs (41%).

- The Republican Party holds an advantage on addressing fraud and waste in government health care programs, which has been a key messaging strategy during the second Trump administration. One-third of voters say they trust Republicans on this issue compared to a quarter who say they trust Democrats. Notably, on most issues asked about, sizable shares of voters say they trust neither party.

Health Care Costs Are a Top Concern for the Public and Voters

Health care costs remain a primary economic concern for the public and voters’ top health concern heading into the 2026 midterm elections. The latest KFF Health Tracking Poll finds health care costs remain at the top of the list of what the public worries about being able to afford for themselves and their family, now tied with gasoline and transportation costs amid rising fuel prices. Nearly two-thirds of the public (64%) say they are at least somewhat worried about affording health care costs including the cost of health insurance and out-of-pocket costs such as for office visits and prescription drugs. This includes three in ten adults overall (30%) and voters (30%) who say they are “very worried” about paying for health care. A similar share of adults is “very worried” about affording gas and transportation costs (29%), up from about one in six (17%) in January. This comes as the national average for gasoline has risen to over $4 per gallon, up roughly 38% since the conflict with Iran began. About one in five adults say they are “very worried” about affording food and groceries (23%), rent or mortgage (21%) or monthly utilities (21%).

Even among adults with health insurance coverage, lowering health care costs is a top concern. When asked about possible changes that could be made to their health insurance, about half of insured adults say “paying less out-of-pocket for health care” (46%) is most important, more than twice the share who choose “eliminating prior authorization” (22%), an area that previous KFF polls have identified as the most significant pain point for health care consumers aside from costs. Fewer insured adults say getting more value out of their care (13%) or having more choice of which health care providers they can see (12%) are the most important changes they’d like to see.

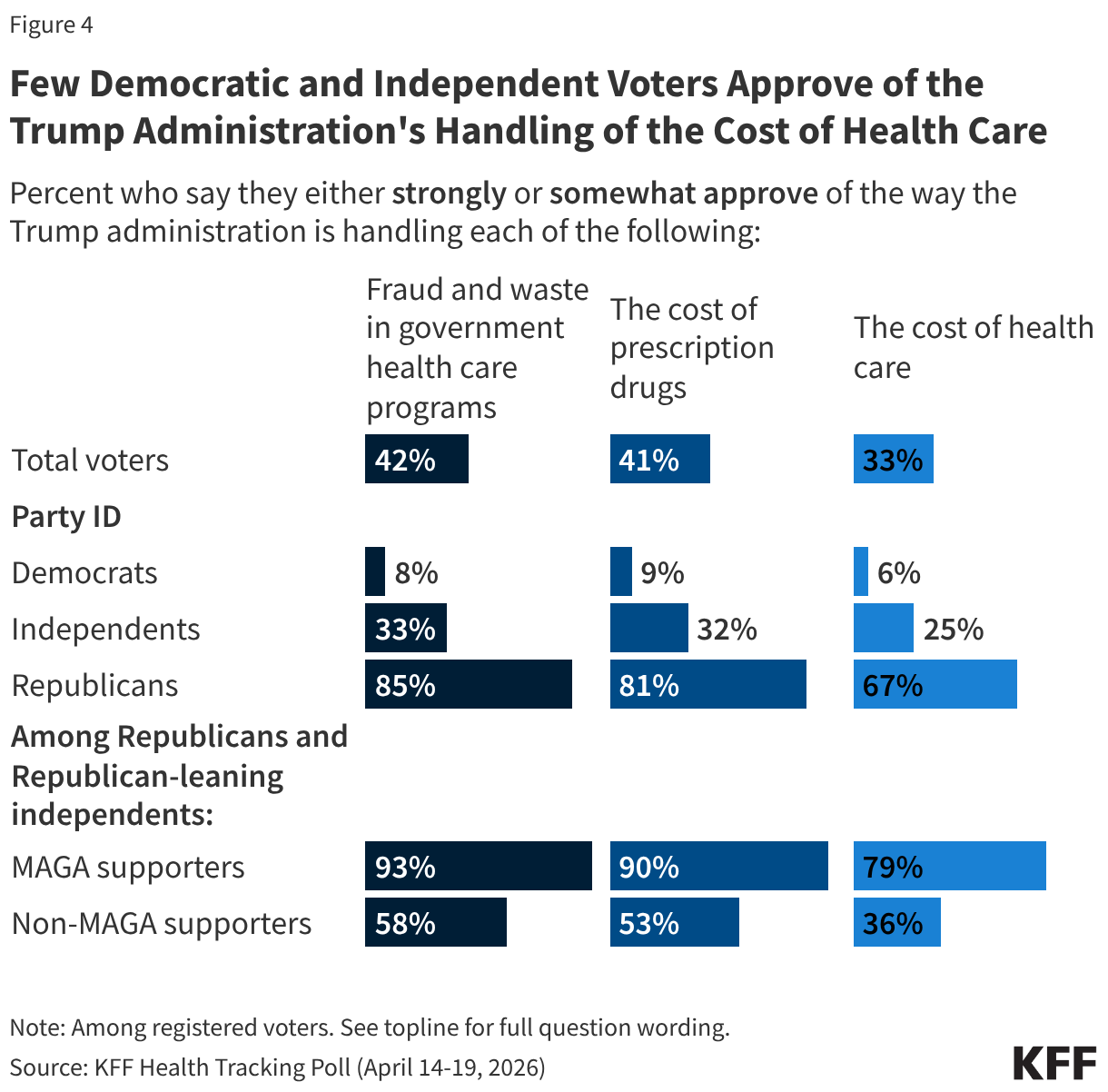

Voters’ Approval of the Trump Administration and Party Preference on Health Care Issues

With about six months to go before the midterm elections, most voters disapprove of how the Trump administration is handling issues related to health care costs. One-third of voters (33%) approve of the administration’s handling of the cost of health care while two-thirds (67%) say they disapprove – including 45% who say they “strongly disapprove.” Several months after the unveiling of TrumpRx, about four in ten voters (41%) approve of the administration’s handling of prescription drug costs. Following a recent announcement by the Trump administration of increased efforts to crack down on health care fraud, about four in ten voters (42%) say they approve of the way the administration is handling fraud and waste in government health programs, while a majority (58%) say they disapprove.

Unsurprisingly, voters are split along partisan lines with the Trump administration receiving high approval ratings from Republicans overall, and most Democrats disapproving of the administration. Among independent voters, about a third say they approve of the Trump administration’s handling of fraud and waste in government health programs (33%) and its handling of the cost of prescription drugs (32%). Fewer independents (25%) say they approve of the administration’s handling of the cost of health care.

Notably, while two-thirds of Republican voters approve of the administration’s handling of health care costs (67%), there is some nuance within the Republican coalition. Among the two-thirds of Republicans and Republican-leaning voters who identify as MAGA supporters, about eight in ten (79%) approve of the administration’s handling of health care costs. However, Republican voters who do not support the MAGA movement are less approving of the administration with just over one-third (36%) of non-MAGA Republicans approving of the administration’s actions on health costs while 64% disapprove. Additionally, non-MAGA Republicans and Republican-leaning independents are much less likely than their MAGA counterparts to say they approve of the Trump administration’s handling of the cost of prescription drugs (53% vs. 90%) and their handling of fraud and waste in government health programs (58% vs. 93%).

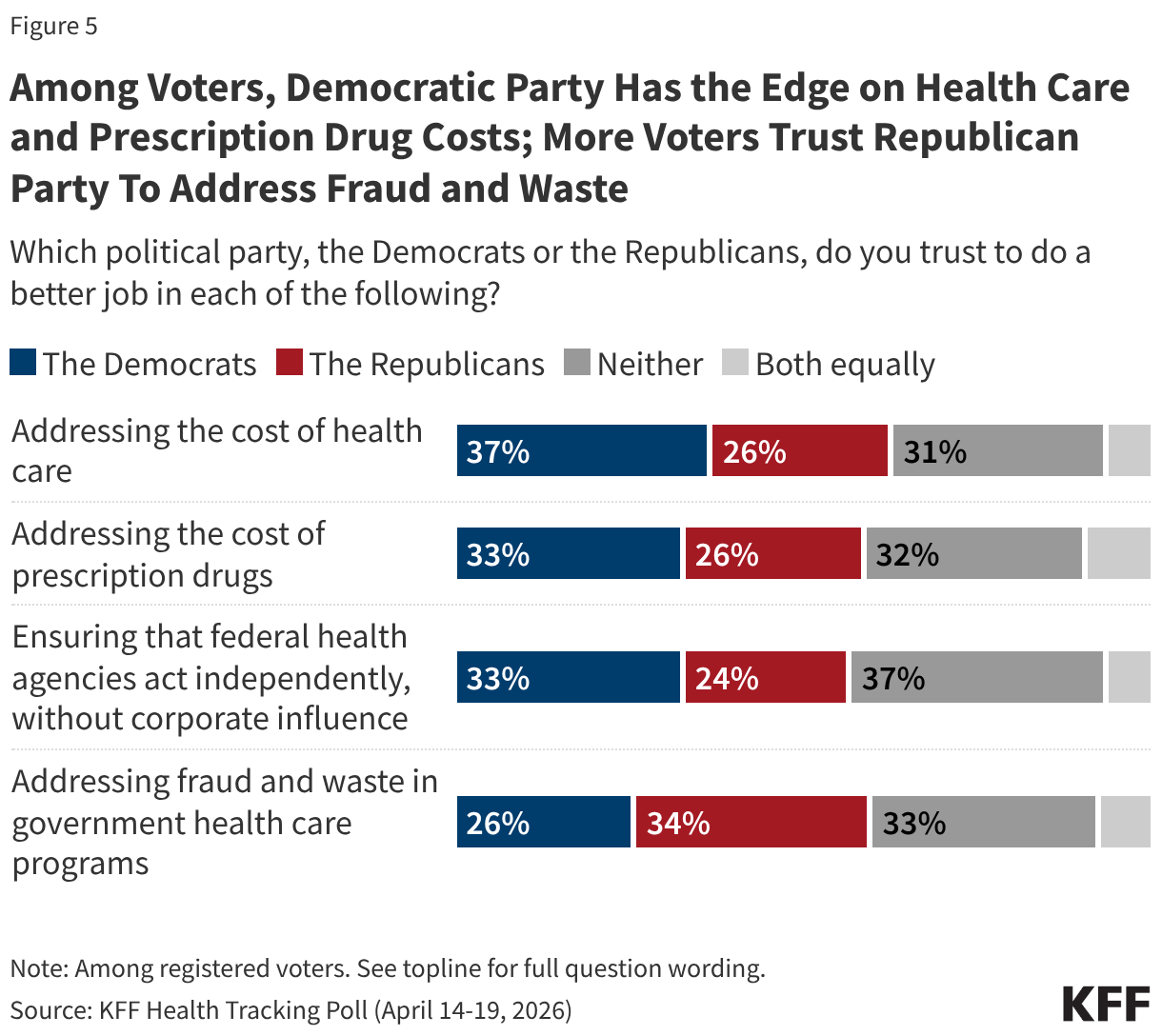

As voters evaluate congressional candidates ahead of the midterm elections, the Democratic Party has an edge over the Republican Party when it comes to addressing the cost of health care, while the Republican Party has the edge on addressing fraud and waste in government health care programs. Democrats have a double-digit advantage over Republicans when it comes to who voters trust to address the cost of health care (37% vs. 26%) and continue to hold a narrow edge among voters when it comes to addressing the cost of prescription drugs (33% vs. 26%).

Voters are more likely to trust the Republican Party (34%) than the Democratic Party (26%) when it comes to addressing fraud and waste in government health care programs, an area the Trump administration has focused heavily on recently. About one-third (33%) say they trust neither party to handle this issue.

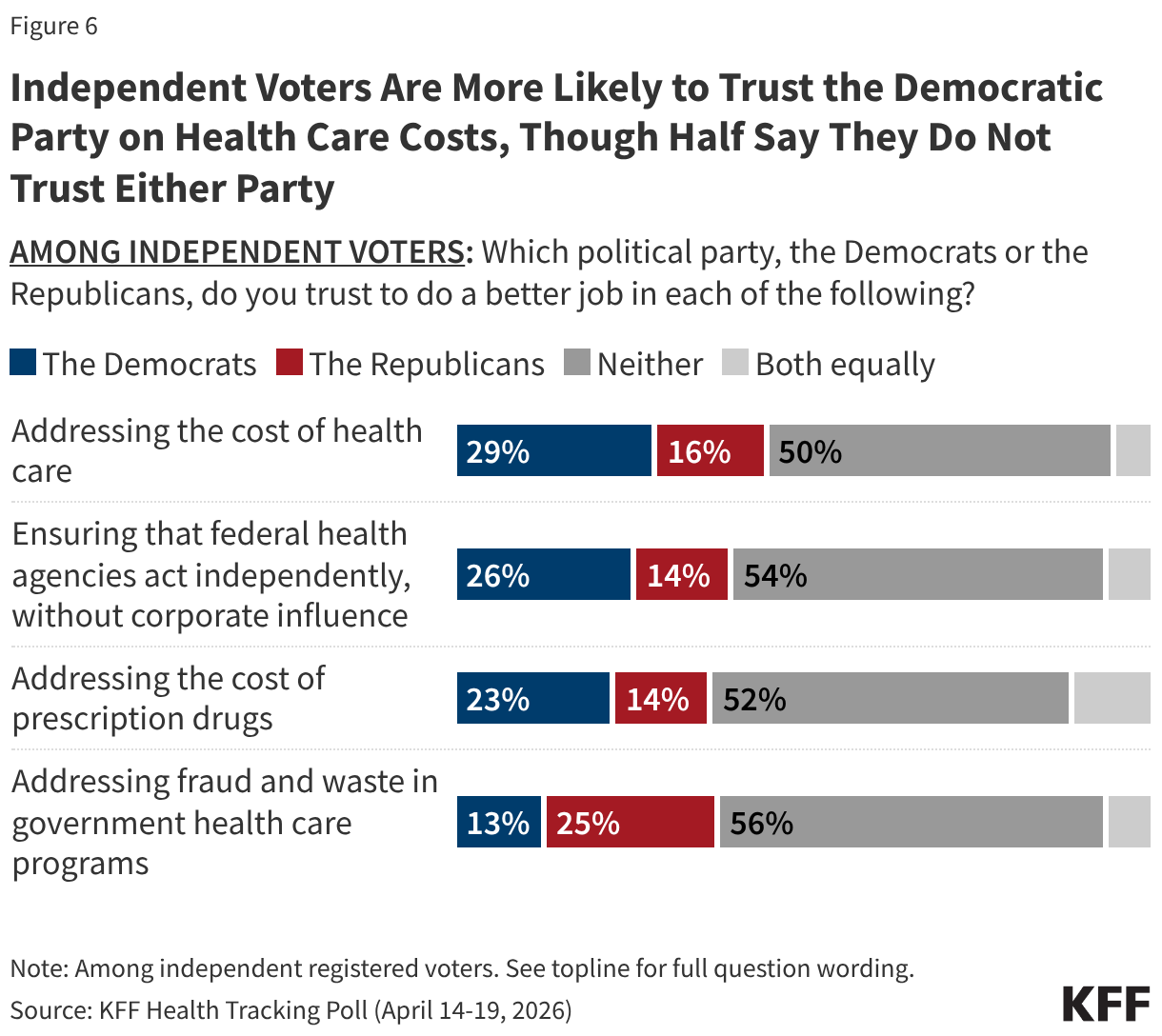

Among independent voters, the Democratic Party has a double-digit advantage over the Republican Party when it comes to addressing the cost of health care (29% vs. 16%), while the Republican Party holds the advantage when it comes to addressing fraud and waste in government health care programs (25% vs. 13%). Yet notably, at least half of independent voters say they trust neither party to address each of these issues.

In addition to ranking as a top economic concern for the public, majorities of voters say health care costs will have a “major impact” on their decision to vote (55%) and which party’s candidate they would support (61%) in the upcoming midterms. The issue of health costs is more salient for Democratic voters compared to Republicans. More than six in ten Democratic voters say the cost of health care will have a major impact on their decision to vote (64%) and which party’s candidate they support (72%). About half of Republican voters say the issue of health costs will majorly impact whether they vote (48%) and what candidate they will support (47%). About half of independent voters say the cost of health care will majorly impact their decision to vote (52%) and six in ten say this issue will majorly impact the party’s candidate they support (63%).

Poll: The Cost of Health Care Remains at the Top of the Public’s List of Economic Concerns, Even as Concerns About Gas Prices Climb

rewrite this content and keep HTML tags

Health care costs continue to top the public’s list of economic anxieties, even as fuel prices and economic uncertainty rose following the start of the Iran war, a new KFF Health Tracking poll finds. Nearly two-thirds (64%) of U.S. adults are worried about being able to afford health care costs, including three in ten who say they are “very worried.” The same share (64%) are worried about gasoline or other transportation costs, up from about half (52%) in January.

Underscoring these concerns, nearly half of insured adults (46%) say that lowering out-of-pocket costs is their most-wanted change to their health insurance. Additionally, majorities of voters say health care costs will have a “major impact” on their decision to vote (55%) and which party’s candidate they support (61%).

While the poll finds that voters trust Democrats more than Republicans to address both health care costs (37% vs. 26%) and prescription drug costs (33% vs. 26%), voters are more likely to trust Republicans on the issue of fraud and waste in government health care programs (34% vs. 26%)—an issue on which the Trump administration has been particularly engaged.

CMS Extends Medicare’s Short-Term Bridge Program for GLP-1 Obesity Drug Coverage

rewrite this content and keep HTML tags

The Centers for Medicare & Medicaid Services (CMS) has announced that its temporary program to cover GLP-1 drugs for obesity in Medicare, called the BALANCE model, will not launch as scheduled on January 1, 2027. Instead, CMS is extending the duration of a separate short-term program, called the Medicare GLP-1 Bridge, which was originally scheduled to run from July-December 2026 but will now run through the end of 2027. Under the Bridge program, eligible beneficiaries can get Medicare coverage of GLP-1s for obesity for a $50 copay.

Extending the short-term GLP-1 Bridge program is good news for eligible Medicare beneficiaries because it provides the certainty of obesity drug coverage at a $50 copay for a longer duration, but federal spending will also rise by some unknown amount since CMS hasn’t disclosed the projected cost. The cost to Medicare of covering obesity drugs under Part D has been estimated at between $25 billion and $35 billion over 10 years, which could have been a driving factor in the reluctance or unwillingness of major Part D plan sponsors to participate in the BALANCE model as it was originally designed.

While CMS sought robust participation of Part D plan sponsors in the BALANCE model, which was voluntary for plans, interest appears to have fallen short of the targeted level. Although GLP-1 drug manufacturers agreed to a $245 net price, a substantial discount off prevailing list prices, savings to plans from a lower price may have been insufficient to offset higher costs associated with an uptake in GLP-1 use for obesity treatment. Plans would also have been at some financial risk if their actual costs for covering GLP-1s were higher than they expected. Higher costs for Part D plans under the BALANCE model would have translated to higher federal spending and increased Part D premiums for enrollees, always a tough sell but especially so when the cost of health care, including prescription drugs, ranks as a top concern for many Americans.

Implementation of the BALANCE model in Medicare faces an uncertain future. CMS could opt to revise the financial incentives to make participation more appealing to Part D plan sponsors, such as by negotiating an even lower net price with manufacturers or taking other steps to shift financial risk associated with GLP-1 coverage away from plans. While CMS’s approach to Medicare obesity drug coverage after the short-term Bridge program ends is unknown, a financially sustainable solution for how to cover GLP-1 drugs for obesity remains elusive.