rewrite this content and keep HTML tags

A Closer Look at North Carolina’s Implementation of the 2025 Reconciliation Law Medicaid Provisions and Other Changes Amid Medicaid Budget Shortfalls

rewrite this content and keep HTML tags

On April 30, 2026, North Carolina Governor Josh Stein signed legislation that includes Medicaid policy changes and closes an estimated $319 million shortfall in funding for the state’s Medicaid program for FY 2026. Many of the legislation’s Medicaid policy changes are related to implementation of the 2025 federal reconciliation law. The 2025 reconciliation law requires states to condition Medicaid eligibility for adults in the Affordable Care Act (ACA) Medicaid expansion group and enrollees in partial expansion waiver programs (Georgia and Wisconsin) on meeting work requirements starting January 1, 2027. The 2025 reconciliation law also limits states’ ability to raise the state share of Medicaid spending through provider taxes, restricts state-directed payments (SDPs) to hospitals, nursing facilities, and other providers, and increases barriers to enrolling in and renewing Medicaid coverage. As states are preparing to implement the reconciliation law provisions, many states are facing more tenuous budget situations with slowing revenue growth and broader reductions in federal funding.

This policy watch examines the current budget context in North Carolina, the state’s recently passed legislation, the state’s Medicaid Advisory Committee (MAC) meetings, and data from KFF’s Medicaid work requirements tracker to provide initial insight into how North Carolina is preparing to implement certain Medicaid provisions of the 2025 reconciliation law and how other policy changes may affect coverage and access to care. While some of the issues North Carolina is facing are unique to that state, others are likely to be faced by other states as they implement federal changes to Medicaid in the midst of other fiscal challenges.

What is the budgetary context as North Carolina prepares to implement the 2025 reconciliation law’s provisions?

North Carolina is facing a more tenuous fiscal climate like in other states, and state legislators have not yet enacted a comprehensive state budget for the FY 2025-27 biennium. In the past year, revenue volatility and rising costs have led to slowing state revenue growth following a period of record-breaking revenue and expenditure growth for states after the initial pandemic-induced economic downturn. In North Carolina, scheduled tax cuts have been projected to drive declines in state revenue, and debates over whether to proceed with the cuts have contributed to a budget stalemate in the legislature.

In August 2025, Governor Stein signed a stopgap funding bill that appropriated $600 million from the state general fund for Medicaid, but it left a $319 million shortfall for FY 2026 in funding for the cost of services for non-expansion (traditional) enrollees. The shortfall and budget stalemate led to rate cuts and the elimination of GLP-1 coverage, both of which were eventually restored. The Medicaid agency ceased “Healthy Opportunities Pilots” program services in FY 2026 due to a lack of appropriations. The pilots covered certain non-medical services that target social needs, including housing, nutrition, transportation, and interpersonal relationship supports to specific and limited enrollees, and evaluations of the “Healthy Opportunity Pilots” 1115 waiver showed lower costs over time and largely positive outcomes. The Medicaid agency also implemented changes to reduce administrative expenses, including reducing temporary staff and contractors, ending certain contracts, pausing quality improvement projects, and scaling back compliance and quality oversight activities. The legislation signed in April 2026 appropriated $319 million to close the shortfall for FY 2026 and made changes aimed at addressing financing pressures associated with new federal limits on provider taxes, which the state uses to help finance its Medicaid expansion and hospital state directed payment program (which increases payment rates for hospitals).

What are some of the Medicaid policy changes included in North Carolina’s recent legislation?

Eligibility and Cost Sharing

North Carolina’s new legislation includes more restrictive standards for how the state will implement work requirements than is required in current law. At a minimum, the 2025 reconciliation law requires states to look back one month immediately preceding the application month and one month between renewal periods to confirm compliance with the requirements. North Carolina’s legislation requires the state to confirm compliance for the three months preceding the application month. At renewal, the state must confirm compliance for at least three of the six months since the last determination of eligibility. The North Carolina legislation also prohibits the acceptance of self-attestation as the only evidence in verification of eligibility requirements (unless required by federal law or regulation, or pursuant to a court order). States await guidance from CMS as to whether self-attestation of medical frailty, parent/caretaker status, or other exemptions or work status can be accepted, but most states report plans to accept self-attestation if allowed.

The legislation increases the frequency of data checks to identify changes in circumstances for Medicaid enrollees from quarterly to monthly. The state will review information on earned and unearned income, employment status and changes in employment, residency status, enrollment status for other public assistance programs administered by the state and outside of the state, financial resources, incarceration status, and lottery and gambling winnings. States are required to follow up on reported changes that potentially affect eligibility and give individuals an opportunity to respond before taking adverse action. In North Carolina, when data indicates an individual is no longer eligible, enrollees only have 10 days in advance of case closure to submit documentation verifying ongoing eligibility. Increasing the frequency of periodic data checks with insufficient response times can lead to procedural disenrollments and exacerbate churn.

The Medicaid agency will be required to set Medicaid copayments at the highest allowable amounts for both traditional Medicaid enrollees and ACA expansion enrollees. Current federal rules limit cost sharing in Medicaid because of enrollees’ low income and limited ability to pay out of pocket costs. The maximum allowable cost sharing varies by type of service and enrollee income. North Carolina has set current cost sharing amounts, regardless of enrollee income, at $4 per service. Starting July 1, 2027, the legislation requires the Medicaid agency to increase current cost sharing amounts for services where the maximum allowable amount is more than $4 and to increase cost sharing for ACA expansion adults with income 100-138% FPL to up to 10% of the cost of the service, except for prescription drugs and non-emergency use of the emergency department. Beginning in October 2028, when states are required to implement mandatory cost sharing of up to $35 per service for ACA expansion adults with income between 100%-138% FPL, the state will be required to set cost sharing amounts at $35 per service, except for prescription drugs, for all non-exempt services for this group.

The legislative text implementing the changes to Medicaid eligibility for certain lawfully residing immigrants effectively ends the state’s long-standing optional Medicaid coverage for lawfully residing children and pregnant immigrants without a five-year waiting period. The law limits Medicaid coverage for immigrants to coverage that is required under federal law. However, North Carolina is one of 40 states that have taken up the option to extend Medicaid and/or CHIP coverage to children and/or pregnant adults who are lawfully residing and waive the five-year wait for these groups. The 2025 reconciliation law imposed additional eligibility restrictions for many lawfully present immigrants but allows states to maintain the option to cover lawfully residing children and pregnant adults. By limiting coverage for immigrants to only what is required by federal law, the state law effectively ends this optional coverage as of October 1, 2026. In a recent Medicaid Advisory Committee (MAC) meeting, the Medicaid agency indicated it was working with the legislature to make “corrections” and restore coverage for these populations.

The legislation requires the Medicaid agency to report certain Medicaid applicants and enrollees for whom it cannot verify citizenship or “satisfactory” immigration status to the Department of Homeland Security. These include applicants and enrollees who, after a reasonable opportunity period, have not verified satisfactory immigration status or whose final verification indicates that they do not have a satisfactory immigration status and are not lawfully present. This group would include those found ineligible based on immigration status and individuals receiving Emergency Medicaid services (where Medicaid pays hospitals for emergency care provided to ineligible immigrants who would otherwise be eligible for Medicaid based on their income).

Medicaid Financing

The legislation increases intergovernmental transfers (IGTs) from public hospitals, reducing reliance on the state’s hospital taxes for financing the nonfederal share of Medicaid spending. The 2025 reconciliation law imposes significant new restrictions on states’ ability to generate Medicaid provider tax revenue, including prohibiting all states from establishing new provider taxes or from increasing existing taxes, as well as reducing existing provider taxes for states that have adopted the ACA Medicaid expansion. North Carolina uses provider taxes to help finance the nonfederal share of Medicaid spending. State law requires the nonfederal share for the expansion program to be fully funded by certain non-general fund sources, including hospital taxes and hospital IGTs, and requires the end of expansion coverage if those sources cannot fully fund the nonfederal share. The state estimates $14.3 million in one-time administrative costs for the current state fiscal year and $44.4 million in recurring annual administrative costs (including both state and county expenditures) for the expansion program to implement work requirements and six-month eligibility redeterminations that existing financing mechanisms did not account for. The increased public hospital IGTs aim to offset the financing of some of the existing costs under the state’s hospital tax, as well as to help finance the new administrative costs.

By increasing reliance on IGTs as a financing source, the state may aim to retain higher hospital SDPs under new federal provider tax limits, but new federal requirements for state directed payments are expected to require further changes. North Carolina’s Healthcare Access and Stabilization Program (HASP), a hospital SDP program launched alongside Medicaid expansion in 2023, is also financed through hospital taxes and IGTs. An earlier state report indicated the new federal provider tax limits would eliminate all or most of HASP SDPs. The state has been using HASP payments to incentivize hospitals to relieve medical debt, and as of October 2025, more than $6.5 billion in debt had been relieved for more than 2.5 million North Carolinians under the initiative.

There is significant uncertainty about how federal regulations and state legislation may affect the state’s plan for financing the nonfederal share of Medicaid spending, including for the Medicaid expansion and HASP. New proposed rules on state directed payments and forthcoming provider taxes may affect the state’s financing plans. The state’s legislation created a “trigger” to end the new funding should HASP payments fall below certain thresholds or a change in federal law or regulation result in at least a 20% decrease to IGTs.

Health insurers are exiting the Marketplace again. Should consumers be worried?

rewrite this content and keep HTML tags

At least five health insurers have announced plans to leave the ACA Marketplace after 2026, affecting more than 600,000 enrollees across multiple states. The exits are raising new questions about the stability of the individual market and whether additional insurers could follow.

Although insurer participation in the ACA Marketplace has fluctuated for years, the latest withdrawals come at a time of growing uncertainty driven by higher premiums, declining enrollment, and federal rule changes that could further reshape the market in 2027.

Which carriers have announced they’re leaving the Marketplace?

So far, at least five insurers have announced that they will no longer offer Marketplace plans after the end of 2026. They include:

- Cigna, which offers Marketplace plans in Arizona, Colorado, Florida, Georgia, Illinois, Indiana, Mississippi, North Carolina, Tennessee, Texas, and Virginia. Across those 11 states, Cigna currently covers about 369,000 Marketplace enrollees. Cigna will not offer Marketplace coverage in any state in 2027.

- Baylor Scott & White Health Plan, which covers about 100,000 Marketplace enrollees in Texas.

- CareSource will no longer offer Marketplace coverage in Indiana, where it currently insures about 60,000 people. CareSource offers Marketplace plans in nine states in 2026, and it’s unclear whether any other states where CareSource offers plans will be affected.

- PacificSource will no longer offer Marketplace coverage in Idaho, Montana, or Oregon, where a combined 60,000 people have PacificSource Marketplace plans.

- Providence Health Plan will no longer offer Marketplace plans in Oregon. At the end of 2025, there were nearly 36,000 Oregon Marketplace enrollees with Providence plans.

Across those five carriers, more than 600,000 people will need to select new Marketplace plans for 2027.

Could additional insurer exits still be ahead? Possibly. But it’s still early in the 2027 rate filing season, and the full picture of Marketplace participation may not become clear until much closer to open enrollment, since some insurers have historically waited until the fall to announce Marketplace exits.

Will any carriers exit the market before the end of 2026?

Historically, most Marketplace insurer exits have occurred at the end of the calendar year. Mid-year shutdowns have been rare, with notable exceptions including some ACA CO-OP failures in the early years of the exchanges and the collapse of Friday Health Plans in 2023.

Thus far, all of the Marketplace exits announced this year are scheduled for the end of 2026, so they do not affect anyone’s 2026 coverage. Enrollees can keep their current plan through the end of the year as long as they continue to pay their monthly premiums.

Learn more: What should consumers do if their insurer is leaving the Marketplace?

Why are carriers pulling out of the Marketplace?

Industry groups and insurers have described the current environment as a “perfect storm” for the individual market.

Several major changes are contributing to that uncertainty, including:

All of these factors are causing enrollment declines and a less healthy risk pool in the individual market.

Declining Marketplace enrollment drives carrier decisions

Marketplace enrollment declined in 2026, after five years of steady growth – and according to a Wakely analysis, effectuated enrollment is projected to be 17% to 26% lower in 2026 than it was in 2025.

Although we don’t yet have official nationwide 2026 effectuated enrollment data from Centers for Medicare & Medicaid Services (CMS), NOTUS (News of the United States) has obtained internal CMS documents and reported that 21% of HealthCare.gov enrollees were disenrolled in the early months of 2026 for failure to pay premiums. Across state-run Marketplaces, the drop-off was much smaller, at about 8%, due in part to the supplemental subsidies offered by some state-run Marketplaces.

But nationwide, about 17% of the people who selected a plan during the open enrollment period for 2026 (or whose coverage was automatically renewed) have already lost their coverage for failure to pay premiums.

And some state-run Marketplaces are showing significant declines in effectuated enrollment in early 2026. For example, Georgia’s effectuated Marketplace enrollment dropped from nearly 1.5 million in early 2025 to 950,000 by April 2026. In Washington state (which does offer state-funded subsidies), effectuated enrollment as of February 2026 was down more than 15% from where it had been a year earlier.

Overall, CMS projects that average effectuated Marketplace enrollment will be about 18.9 million people in 2026, although it could potentially drop to as low as 16.5 million. In comparison, average effectuated Marketplace enrollment was 22.3 million people in 2025.

A major reason for the enrollment decline is the expiration of enhanced federal subsidies at the end of 2025. Many Marketplace consumers saw premiums rise sharply when those subsidy enhancements expired. Even though millions of people switched to plans with higher out-of-pocket costs or dropped their coverage altogether, average net premiums in the Marketplace still rose by 58% in 2026.

That sharp increase in net premiums is the primary reason so many people failed to pay their premiums in the early part of 2026. That matters because healthier consumers are generally more likely to drop coverage when premiums increase, while people with ongoing medical needs are more likely to keep their insurance.

As healthier people leave the market, insurers are left covering a smaller but less healthy risk pool. That increases average medical costs per enrollee and puts upward pressure on premiums.

The Trump administration’s rule changes for 2027 could intensify those pressures even further. Federal regulators have projected that the new rules could lead to as many as 2 million additional people leaving the Marketplace.

CMS has also acknowledged that healthier enrollees may be more likely to lose or discontinue coverage under the new rules, potentially contributing to additional premium increases (although CMS notes that these premium increases may be offset by more eligibility verification for special enrollment periods and lower exchange user fees).

Marketplace participation is ultimately a business decision

For insurers, participation in the Marketplace is fundamentally a financial calculation.

Insurers continuously evaluate whether Marketplace coverage is profitable and whether the market appears stable enough to justify continued participation. When enrollment declines, risk pools worsen, and policy uncertainty increases, some insurers decide the business risk is no longer worthwhile.

There can also be state-specific policy factors involved. New Mexico, for example, requires Medicaid managed care insurers to also offer statewide Marketplace coverage. But in most states, Marketplace participation decisions are largely driven by insurers’ assessment of profitability and overall market stability.

Current withdrawals reflect a familiar cycle

Insurer participation in the Marketplaces has been cyclical over time, generally increasing when the individual market was healthier and larger, and decreasing when it was sicker and smaller. We can see a clear illustration of this when we look at how Aetna’s Marketplace participation has shifted in response to changing market conditions.

At the end of 2016, Aetna exited the Marketplace in 11 of the 15 states where it offered coverage. The company then fully exited the ACA exchanges after 2017.

But Aetna later returned to the Marketplace in 2022 and expanded into additional states in 2023. However, the company once again fully exited the Marketplace after 2025.

That pattern mirrors broader Marketplace trends over the past decade.

Insurer participation declined significantly in 2017 and 2018 amid repeated congressional repeal efforts and policy uncertainty surrounding the ACA.

Participation later rebounded during the Biden administration, when enhanced subsidies and other policy changes (including a low-income special enrollment period, fixing the “family glitch,” and Marketplace access for DACA recipients) made Marketplace coverage more affordable and accessible, resulting in far more people with Marketplace coverage.

But the number of insurers participating in the Marketplace declined again for 2026, after several of the Biden-era changes were eliminated. This was the first overall decline in insurer participation since 2018.

Still, today’s Marketplace participation levels remain significantly stronger than they were during the market instability of 2017 and 2018.

In 2018, more than a quarter of Marketplace enrollees only had access to plans from a single insurer. By contrast, despite the recent decline in participation, only 1% of HealthCare.gov enrollees in 2026 had access to just one insurer’s plans.

What should consumers expect next?

Additional Marketplace exits remain possible over the coming months, as insurers finalize 2027 rates participation decisions.

But while the current insurer withdrawals and declining Marketplace enrollment are significant, the individual market has proven to be resilient. It has gone through cycles of expansion, contraction, policy changes, and insurer repositioning over the past decade.

The coming months will provide a clearer picture of whether 2027 represents another temporary contraction – or the beginning of a more significant shift in the Marketplace landscape.

Key Facts About Health Care Affordability for People With Medicare

rewrite this content and keep HTML tags

This brief draws on data from various sources. Data on income and savings of Medicare beneficiaries, including the share of beneficiaries who relied on Social Security for at 75% or 90% or more of their total per capita income and the number of Medicare beneficiaries who spent more than 10% of their annual per capita income on Part B premiums, are drawn from the Urban Institute’s Dynamic Simulation of Income Model (DYNASIM4). See Methods of KFF, “Income and Assets of Medicare Beneficiaries in 2024” (August 2025) for more details.

Data on out-of-pocket health care spending are from the Centers for Medicare & Medicaid Services (CMS) Medicare Current Beneficiary Survey, 2023 Cost Supplement File (the most recent year of data available). For the analysis on average out-of-pocket spending as a share of average per capita Social Security income, see the methods of KFF, “Health Costs Consume a Large Portion of Income for Millions of People with Medicare” (August 2025) for more details.

The 2024 Consumer Expenditure Survey (CE) by the Bureau of Labor Statistics is used to assess the financial burden of health care spending among households where all members are covered by Medicare (referred to as Medicare households) compared to households where no members are covered by Medicare (referred to as non-Medicare households). The CE is a survey of households (“consumer units”), excluding people residing in institutions such as long-term care facilities. The estimates presented in this analysis are averages for demographic groups of consumer units, not per capita estimates, and thus are not comparable to estimates based on other surveys that report per capita estimates, such as out-of-pocket health care spending reported in the Medicare Current Beneficiary Survey.

Estimates of Medigap premiums are based on KFF analysis of Medicare Supplement Market Data from Mark Farrah Associates Health Coverage Portal TM, 2023. See methods of KFF, “Key Facts About Medigap Enrollment and Premiums for Medicare Beneficiaries” (October 2024) for more details.

Data on annual Medicare premiums, deductibles, and other cost sharing over time are based on KFF analysis of the 2025 Annual Report of the Boards of Trustees of the Federal Hospital Insurance and Federal Supplementary Medical Insurance Trust Funds.

Understanding Medicaid Cost Sharing and Policy Changes from the 2025 Reconciliation Law

rewrite this content and keep HTML tags

Current rules permit, but do not require, states to impose cost sharing on certain populations, within limits designed to protect Medicaid enrollees who have low incomes from high out-of-pocket costs. States have flexibility to impose cost sharing on certain populations. Cost-sharing is generally limited to nominal amounts but may be higher for those with incomes above 100% FPL. Certain populations and services are exempt from cost sharing requirements (Table 1). Total out-of-pocket costs for premiums and cost sharing for all individuals in a Medicaid household are capped at 5% of monthly or quarterly household income. States are required to establish a process for tracking incurred cost sharing that does not rely on enrollee documentation and stops cost sharing once a family meets the cap. States must allow providers to reduce or waive cost sharing for enrollees on a case-by-case basis. A state may allow providers to deny services to enrollees for nonpayment of cost sharing, if the enrollees have a household income above 100% FPL and are not a part of a population exempt from cost sharing except for certain services.

While cost sharing is generally limited to nominal amounts, states can charge higher cost sharing to individuals with income above 100% FPL. The nominal cost sharing amounts for individuals with income up to 100% FPL are specified in regulation and are set at $4 for most outpatient services and preferred drugs, $8 for non-preferred drugs and non-emergency use of the emergency department (ED), and $75 per inpatient stay. These maximum allowable amounts are increased annually by the percentage increase in the medical care component of the Consumer Price Index. For services other than prescription drugs and non-emergency ED use, cost sharing cannot exceed 10% of the cost of the service for individuals in families with incomes from 101-150% FPL and cannot exceed 20% of the cost of the service for individuals in families with incomes above 150% FPL.

States have additional flexibility for imposing cost sharing on non-preferred drugs and non-emergency ED (emergency department) use, including imposing cost sharing for populations otherwise exempt from cost sharing. For prescription drugs, states may impose different cost sharing amounts for preferred and non-preferred drugs and may impose nominal cost sharing for non-preferred drugs on populations otherwise exempt from cost sharing. Preferred drug cost sharing must be applied to non-preferred drugs if the prescribing doctor determines that the preferred drug would not be as effective or would have adverse effects for the individual.

For non-emergency ED use, states may require cost sharing if enrollees are screened by a medical professional to confirm that the care is non-emergency. Enrollees must be notified about the cost sharing charges and provided with the name and location of an available and accessible alternative non-emergency services provider. States may impose cost sharing for non-emergency ED use for individuals otherwise exempt from cost sharing but must limit cost sharing to the maximum amount allowed for individuals with income below 150% FPL. For individuals with income above 150%, there is not a maximum cost sharing amount states may impose. (See Table 1 for full cost sharing rules on prescription drugs and non-emergency ED use.)

Under current rules, states may not charge premiums for Medicaid enrollees with incomes less than 150% FPL. States may charge certain pregnant individuals with premiums of up to 10% of the amount by which their income exceeds 150% FPL. States may also obtain waivers to impose premiums in Medicaid that federal rules do not otherwise allow.

What We Know So Far About 2026 ACA Marketplace Enrollment, Premiums, and Deductibles

rewrite this content and keep HTML tags

The enhanced premium tax credits established by the American Rescue Plan in 2021 and extended through 2025 by the Inflation Reduction Act significantly expanded Affordable Care Act (ACA) Marketplace affordability, driving enrollment to record highs. When those enhancements expired at the end of 2025, premium payments rose sharply for many enrollees, particularly those with incomes above 400% FPL who had been newly eligible for subsidies under the enhanced credits.

This analysis draws on data from the Centers for Medicare & Medicaid Services (CMS) and state-based Marketplace (SBM) Open Enrollment reports, as well as KFF survey data and individual market enrollment estimates from Wakely Consulting Group, to examine early indicators of how the expiration of enhanced premium tax credits has affected effectuated enrollment levels (i.e., enrollment among people who have paid their premiums), plan selections, and out-of-pocket costs in 2026.

Key Findings

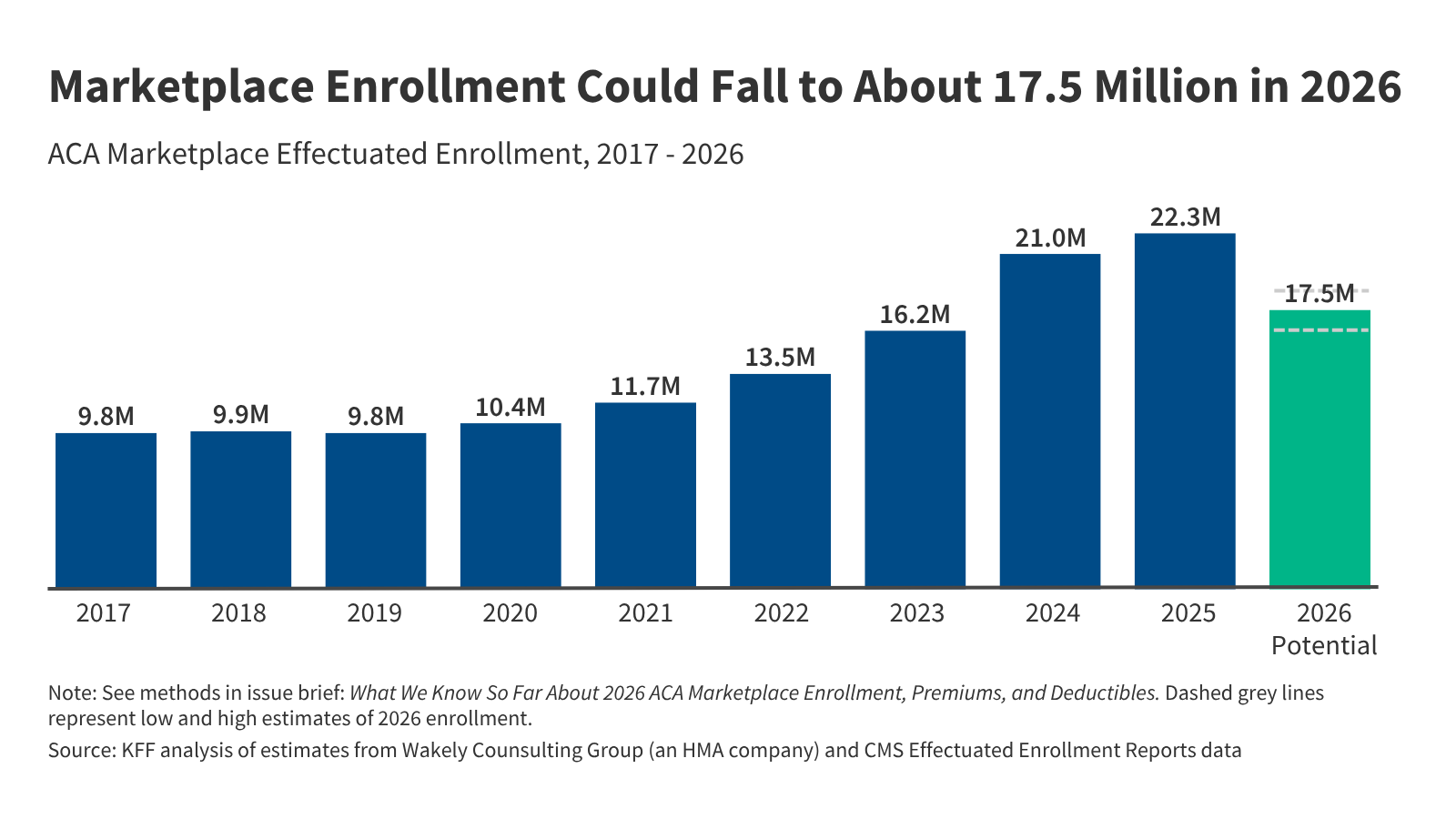

- Based on reports to date of sign-ups and premium payments, average monthly effectuated ACA Marketplace enrollment could fall to about 17.5 million people in 2026 and could be as low as 16.5 million people, down from 22.3 million people in 2025.

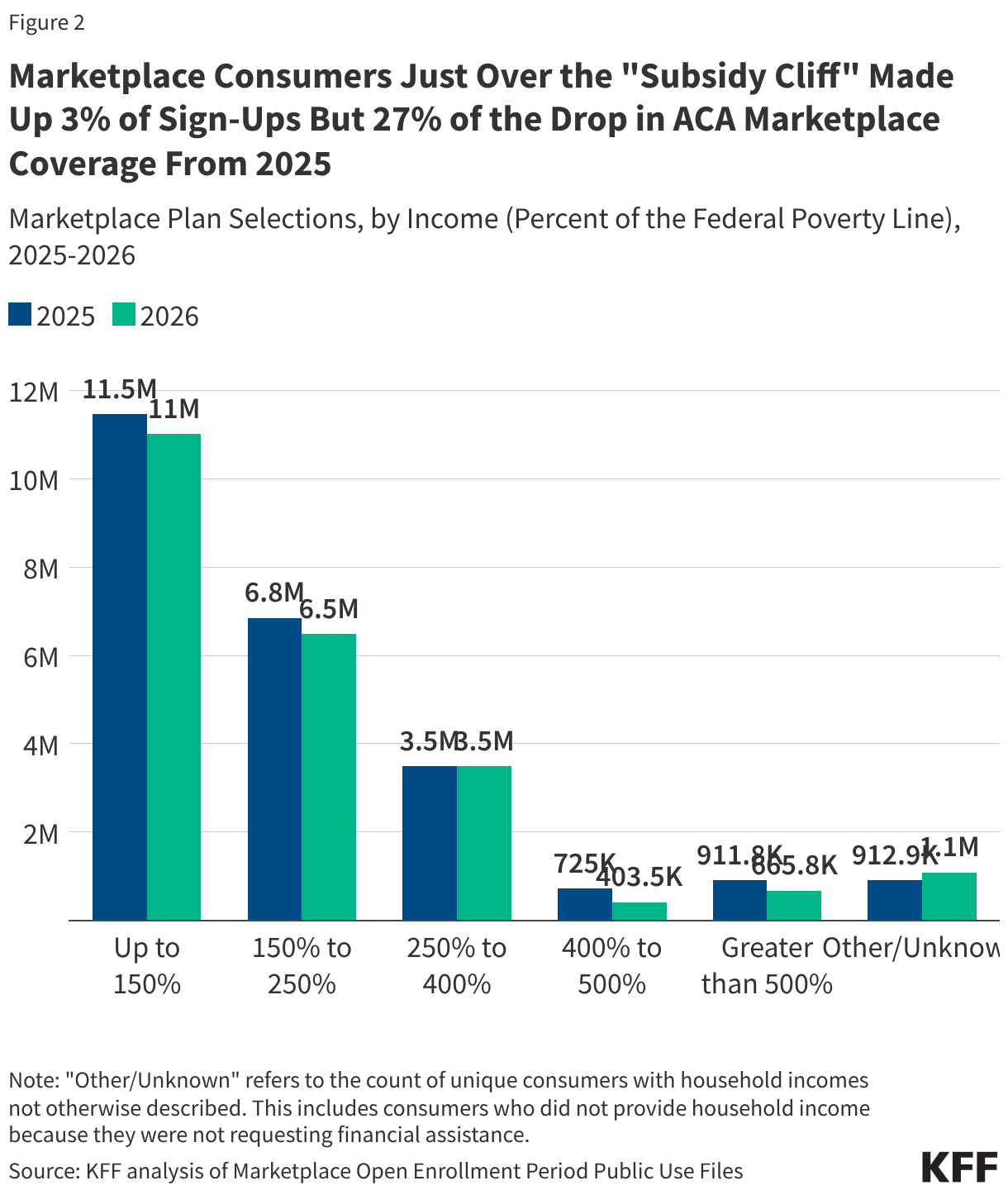

- A disproportionately large share of the drop in sign-ups (27%) is among people with incomes just above the “subsidy cliff” (between 400%-500% FPL), despite this group making up just 3% of plan selections in 2025.

- Premium payments from enrollees increased by an average of 58% from $113 to $178 per month. This is lower than the 114% increase KFF projected if everyone had stayed in the same plan because many people bought down to higher-deductible plans and because those just past the subsidy cliff with the steepest increases dropped ACA coverage at higher rates. Additionally, the 114% increase was among people receiving a tax credit whereas the 58% increase is among all consumers, including the most number who did not receive a tax credit in 2025.

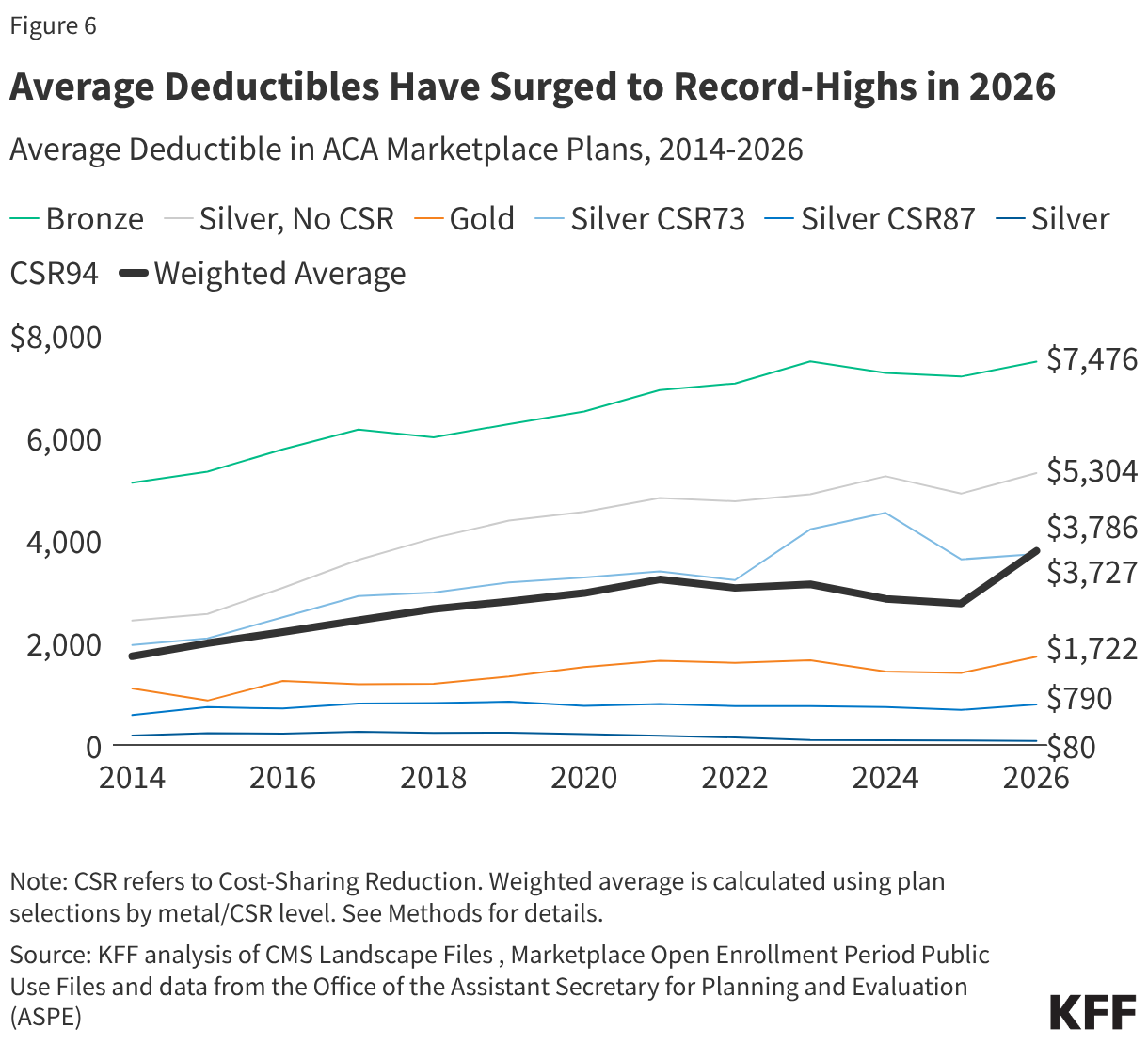

- Average ACA Marketplace deductibles increased by 37% (or $1,027 per person) to a record high of $3,786 in 2026. This is the steepest increase in deductibles ever seen in this market and largely reflects the shift from silver plans with reduced deductibles for lower-income enrollees to bronze plans with very high deductibles.

How Many People Are Leaving the ACA Marketplace?

Plan sign-ups fell by over a million to 23.1 million people during the 2026 Open Enrollment Period, the sharpest single-year drop since the ACA Marketplaces launched. However, Open Enrollment plan selection data alone do not capture the full scope of coverage loss — they measure how many people chose a plan or were automatically renewed, not how many ultimately paid their premiums for their coverage. Effectuated enrollment (the number of people who pay premiums and maintain effective coverage) is expected to fall even further than previous years as 2026 unfolds and many enrollees are unable to afford higher premium payments without enhanced tax credits, signaling significant mid-year attrition on top of already declining sign-ups.

According to an analysis of proprietary data on January premium payments by Wakely Consulting Group, approximately 86% of January 2026 enrollees in the individual market (of which over 90% was through ACA Marketplaces in 2025) paid their first month’s premium, with considerable variation across states. State-based exchanges, many of which have their own premium subsidy programs and more robust outreach efforts, tended to retain higher shares of enrollees than federally-facilitated exchanges.

Accounting for unpaid premiums, mid-year attrition, and other factors, Wakely estimates that average effectuated enrollment in the individual market could decline by between 17% and 26% in 2026 compared to the number of people who had effectuated coverage in 2025.

If applied to the ACA Marketplaces (which represent the vast majority of the individual insurance market in 2025), Wakely’s estimated enrollment decline could translate to an average of about 17.5 million enrollees over the course of 2025, which would represent a potential drop of 4.8 million people from the Marketplaces relative to 2025. To arrive at this estimate, the midpoint value of the range Wakely projects for individual market enrollment to decline by (21.5%) was applied to the average effectuated enrollment in the ACA Marketplace for the first 7 months of 2025. The low and high ends of the grey region in Figure 1 represent estimated effectuated enrollment if the endpoints of the range estimate (17% and 26%, respectively) were applied, ranging from a drop of 3.8 to 5.8 million.

Several other sources of information also point to a sharp decline in ACA effectuated enrollment associated with the expiration of enhanced premium tax credits. A decline of effectuated enrollment to 17.5 million aligns closely with the Congressional Budget Office’s previous projection of a roughly 25% ACA Marketplace contraction in enrollment following the expiration of the enhanced premium tax credits. CBO had projected average monthly ACA Marketplace enrollment of 16.9 million for 2026. Federal data reported on by NOTUS indicated a similarly steep increase in cancellations and terminations due to nonpayment, with about 19 million enrollees in the weeks following Open Enrollment.

Moreover, a KFF survey fielded in late February and early March of 2026 showed that 9% of 2025 Marketplace enrollees had become uninsured, 4% of returning ACA Marketplace enrollees had not yet paid their first month’s premiums, and that one in six (17%) returning enrollees were not confident they could afford their premiums for the entire year.

Recently published data from California, the nation’s largest state-based Marketplace, indicate that the cancellation rate among consumers who renewed coverage increased roughly six percentage points from 2025 such that nearly one in five renewing consumers actively terminated their plans before the end of March or had their coverage cancelled due to nonpayment.

Some states, like Maryland, expect that in the coming months, high premium payments will prompt even more people to either actively cancel their plans or be terminated due to nonpayment of premiums. These cancellations, whether active or passive, will drive a gap between the number of plan sign-ups and effectuated coverage.

Who Dropped ACA Marketplace Coverage?

While there is no publicly available effectuated enrollment data broken out by income, the plan selection data indicate that a large share of the drop in ACA Marketplace coverage is among consumers above 400% of the federal poverty level (FPL), where eligibility for premium tax credits ends (“subsidy cliff”). Under the enhanced premium subsidies, people with incomes above 400% of the poverty level had their premium payments for a benchmark silver plan capped at 8.5% of income. People with incomes above 400% up to 500% FPL, who represented just 3% of 2025 sign-ups, accounted for 27% of the drop in sign-ups from 2025 to 2026. Plan sign-ups for this group fell by 44% (over 321,000 people). Those with incomes above 500% FPL accounted for an additional 21% of the difference.

Overall, consumers with incomes known to be above the subsidy cliff made up just 7% of 2025 enrollment but nearly half (48%) of the decline in plan selections from 2025 to 2026. (There are about 1 million consumers for whom household income is unknown, so the actual share of consumers who are above the subsidy cliff may be higher.)

Lower-income consumers, who continue to receive financial assistance but still saw increases in their premium payments with the expiration of the enhanced tax credits, dropped ACA Marketplace coverage at lower rates. Still, they account for a large share of the decline in sign-ups. Sign-ups for those with incomes below 150% FPL — the largest income group in the Marketplace — fell by roughly 441,000 people (a 4% drop from 2025), accounting for 37% of the decline. Those with incomes greater than 150% and up to 250% FPL accounted for 30% of the drop in ACA Marketplace coverage. Plan selections among consumers with incomes above 250% up to 400% FPL was roughly flat, as losses among the 250 to 300% FPL group were largely offset by gains among the 300 to 400% FPL group.

Declines in plan sign-ups for young adults ages 18 to 34 account for more of the decrease in ACA Marketplace plan selections than any other age group. This is in line with expectations detailed in insurer rate filings from last year, which reported that the expiration of the enhanced premium tax credits would cause younger adults, who are typically healthier, to leave the Marketplace. Sign-ups in this age group declined by 542,000, or 8%, from 6.7 million people in 2025 to 6.2 million people in 2026, comprising 46% of the total decline in ACA Marketplace sign-ups.

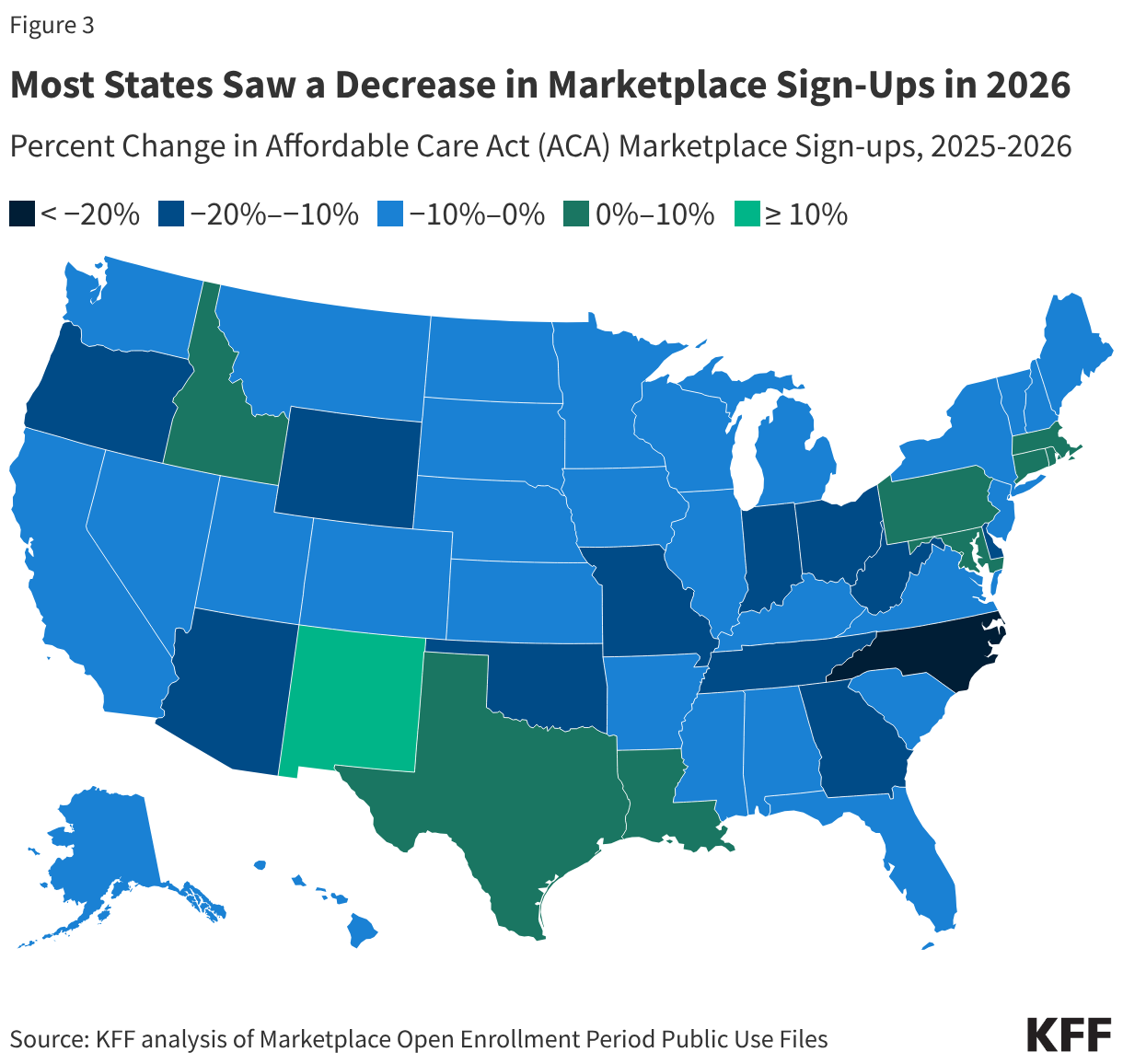

Marketplace plan selections declined in 41 states in 2026. In percentage terms, plan selections fell the most in North Carolina (22%), Ohio (20%), West Virginia (17%) and Indiana, Delaware, and Arizona (all 16%).

A smaller number of states saw stable or modestly increasing sign-ups, in some cases reflecting state-specific policy decisions that helped offset the loss of enhanced federal premium tax credits. Notably, New Mexico experienced an 18% increase in plan selections, likely due in part to the state’s supplemental financial assistance program, which temporarily backfills the entirety of the lost federal premium assistance.

Increases in Premium Payments

In 2026, the average monthly premium payment among consumers net of tax credits (including those who did not receive premium tax credits) rose 58% from $113 to $178 in 2025. With the expiration of enhanced premiums tax credits, KFF previously estimated that premium payments would increase by 114% on average for subsidized ACA Marketplace enrollees to keep their same plan in 2026. However, as discussed more below, many Marketplace enrollees bought down to bronze plans (with lower premiums and higher deductibles). Additionally, people with the steepest increases in premiums — those who lost eligibility for tax credits entirely — appear to have left the market at a disproportionately high rate.

At the same time, the share of people receiving premium tax credits fell from 92% in 2025 to 87% in 2026, the first decline in subsidy uptake since 2020. This is due, in part, to the loss of financial assistance eligibility for people making greater than 400% of poverty and the relatively large exodus from the market among people with incomes over this amount, who would have faced some of the largest premium increases if they had remained in the market.

Increase in Deductibles

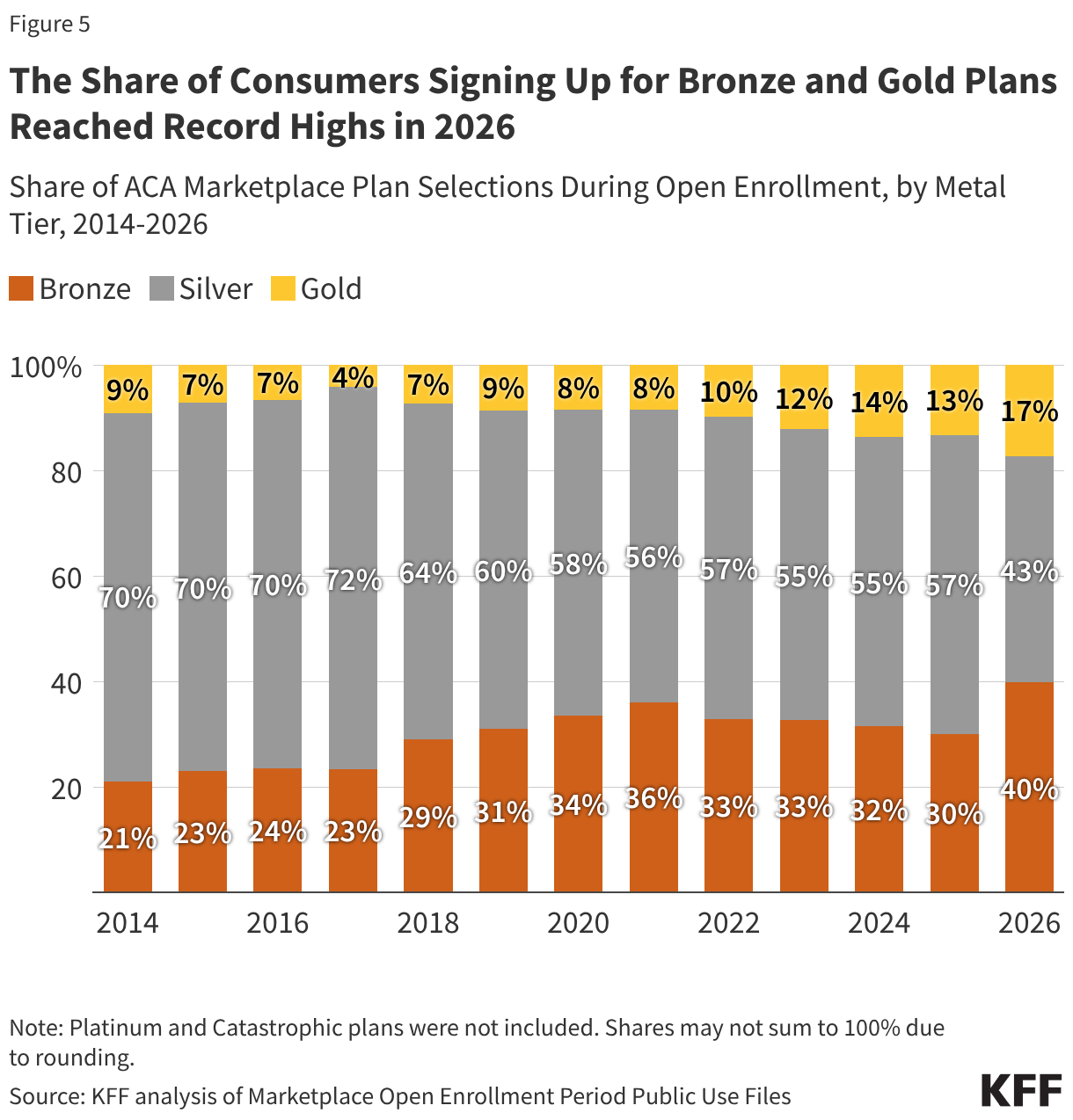

To offset these increases in premium payments with the expiration of enhanced premium tax credits, a number of consumers switched to bronze plans, which have lower premiums but higher deductibles. The share of people selecting bronze plans increased from 30% (7.3 million people) in 2025 to 40% (9.2 million people) in 2026, while the share selecting gold plans rose from 13% (3.2 million people) to 17% (4.0 million people). Meanwhile, the share of ACA marketplace consumers selecting a silver plan fell from 57% (13.7 million people) to 43% (9.8 million people), marking a record low and the first time fewer than half of ACA consumers have selected a silver plan.

With more people signing up for bronze plans than ever before, average deductibles in the ACA Marketplaces are rising. From 2025 to 2026, the average deductible in the ACA Marketplaces has grown by over a thousand dollars per person, a 37% increase, from $2,759 to $3,786. This marks the steepest increase ever in the average Marketplace deductible since the markets launched in 2014. For context, if the distribution of plan selections across metal levels had stayed the same as in 2025, the average Marketplace deductible would have gone up just 6% (to $2,912).

The lowest income Marketplace enrollees (100-250% FPL) also qualify for cost-sharing reductions (CSRs), which lower their out-of-pocket costs (deductibles, copayments, and coinsurance) when paying for health care services if they enroll in silver plans. These CSR plans are offered on a sliding scale, such that those with lower incomes receive more assistance. The average silver deductible available to a person making up to 150% of poverty is $80, compared to $5,304 for the standard silver plan. Previously, with enhanced premium tax credits, silver plans enrollees in this low-income group could get a silver plan with a $0 monthly premium payment. After the expiration of enhanced tax credits, an enrollee would now pay 4.19% of their income, or about $82 a month for a single person at 150% of poverty to keep that low-deductible silver plan.

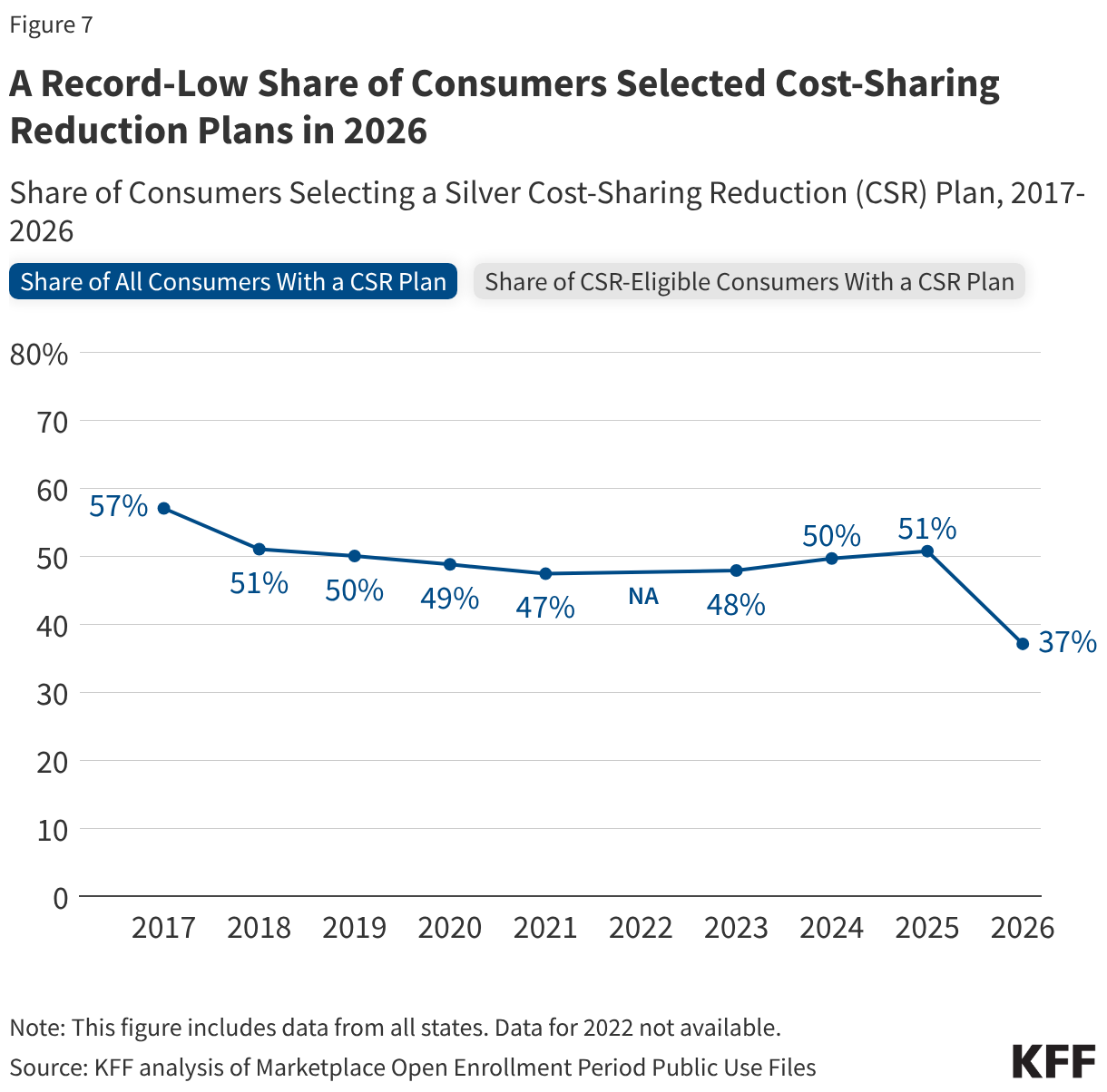

The share of all Marketplace consumers selecting a cost-sharing reduction (CSR) plan fell to its lowest level on record in 2026 (37%). Available data suggests that people are choosing non-CSR plans despite having the income to be eligible for this financial assistance. In 2025, 66% of people in states using the federal platform who were eligible for CSRs signed up for a silver CSR plan. But in 2026, the share of eligible consumers in Healthcare.gov states who selected a CSR plan fell to 45%.

A More Complete Picture is Still to Come

All the information available so far on the demographics of people who left the ACA Marketplace and the increase in premium payments and deductibles is based on plan selections, not effectuated enrollment. Even among those who do effectuate coverage, some could lose it during the year if they cannot afford to continue their premium payments. When CMS publishes effectuated enrollment data later this year, it will include only aggregate counts — without the demographic and plan-level breakdowns available in the plan selection files. Additionally, a grace period was available for returning enrollees to have until late March to make their premium payments, and CMS effectuated enrollment data fully reflecting that grace period may not be available for another year. As a result, a complete picture of how the expiration of enhanced premium tax credits reshaped who has coverage and what kind of plan they hold may not be available for some time.

Methods

This analysis used plan selection and effectuated enrollment data from the Centers for Medicare & Medicaid Services (CMS) and state-based Marketplace (SBM) Open Enrollment reports for plan selections (sign-ups). The estimate of the potential loss in ACA effectuated enrollment (Figure 1) references the report “Who Paid, and Who Stayed? Early 2026 Enrollment Trends in the Individual Market” produced by the Wakely Consulting Group. ACA effectuated enrollment values reflect average monthly effectuated enrollment estimates over the full year for 2017-2024 and over the first seven months for 2025. Potential 2026 enrollment was estimated by applying the midpoint of Wakely Consulting Group’s estimates of reduction in individual market enrollment to average 2025 Marketplace effectuated enrollment. Blue dots represent high and low estimates of effectuated enrollment. Wakely’s estimate may understate enrollment decline in the Marketplaces if a higher share of off-Exchange enrollees pay their January premiums.

Changes in sign-ups by income (Figure 2) and state (Figure 3) were extracted from Open Enrollment Public Use Files. The “Other/Unknown” income category refers to the count of unique consumers with household incomes not otherwise described. This includes consumers who did not provide household income because they were not requesting financial assistance. Trends in average premium (net of tax credits) and share of consumers with advanced premium tax credits (APTC) were taken from the CMS Health Insurance Exchanges 2026 Open Enrollment Report. Average premium payment includes those who signed up both with and without APTC. Distribution of metal level (Figure 5), sourced from the Open Enrollment Period Public Use Files and data from the Office of the Assistant Secretary for Planning and Evaluation (ASPE), does not include platinum and catastrophic plans, which each had <1% of plan selections in 2026. Shares may not sum to 100% due to rounding.

Average deductible over time by plan type (Figure 6) trends the individual medical deductible in plans with combined medical and prescription drug deductibles for only plans offered in the federally facilitated Marketplace, with plan design information from the Medical Individual Market file of the QHP Landscape Files. Plans included were not adjusted for states transitioning to state-based exchanges. First, simple averages over distinct plans were calculated within each metal level (or CSR variant) and were not weighted by plan enrollment. A distinct plan was defined by having a unique state, issuer, metal level, and cost-sharing design combination. In 2014 and 2015, a distinct plan took into consideration the plan marketing name. “Expanded bronze” and “bronze” plans were combined; catastrophic and platinum plans were excluded from analysis. Second, the weighted average was calculated using plan selection data at the metal and CSR (or FPL) level from Marketplace Open Enrollment Period Public Use Files and ASPE data. Share of CSR and non-CSR variants among those selecting silver plans for 2017 and earlier were from the 2017 Open Enrollment income distribution among silver plan selections; consumers selecting a silver plan with income ≥100% to ≤150% of FPL , >150% to ≤200% of FPL , and >200% to ≤250% of FPL were assumed to have selected CSR94, CSR87, and CSR73 variants, respectively. All other years, including 2026, used plan selection, metal level, and CSR distributions from that year.

The share of CSR-eligible consumers with a CSR plan (Figure 7) was calculated from Open Enrollment Public Use Files. While the overall share of consumers with a silver CSR plan includes all states, the share of eligible consumers that signed up for a CSR plan pertains to states using the federally facilitated exchange that year, without adjustment for states transitioning to state-based exchanges.

The Average Marketplace Deductible Grew by About $1,000 Per Person in 2026, With More Enrollees Shifting to Higher-Deductible Plans as Enhanced Tax Credits Expired

rewrite this content and keep HTML tags

The average Affordable Care Act (ACA) Marketplace deductible experienced the steepest increase in history—growing by 37% or over $1,000, from $2,759 in 2025 to $3,786 in 2026 as enhanced premium tax credits expired, according to a new KFF analysis.

After the enhanced tax credits ended, many Marketplace shoppers shifted toward lower-premium, higher-deductible plans. Between 2025 and 2026, sign-ups for bronze plans jumped from 30% to 40% of total plan selections—growing from 7.3 million to 9.2 million people.

Meanwhile, sign-ups for silver Marketplace plans, which have higher premiums and lower cost-sharing, hit the lowest levels in the program’s history. Silver plan sign-ups fell from 57% to a record-low 43%, dropping from 13.7 million to 9.8 million people. The share of Marketplace enrollees who signed up for cost-sharing reduction (CSR) silver plans—which reduce out-of-pocket costs for deductibles, copayments, and coinsurance for lower income enrollees—also fell to the lowest level on record: 37%.

While higher deductible plans have lower premiums, they also result in bigger out-of-pocket bills for patients, straining household budgets and leading to potential medical debt and poorer access to care. Most Marketplace enrollees (67%) said they would likely cut spending on basic household needs if their annual health costs increased by $1,000, according to a KFF survey conducted last November, before the enhanced credits expired.

How Much Marketplace Enrollment Could Fall

Marketplace enrollment could ultimately decline by 21.5% or nearly five million people this year, falling from 22.3 million people in 2025 to about 17.5 million in 2026, according to KFF analysis of estimates from Wakely Consulting Group on premium payments as well as federal data.

About 23 million people signed up for Marketplace plans during the 2026 Open Enrollment Period—over a million fewer than in 2025 and the sharpest single-year drop in raw numbers since the ACA Marketplaces launched—and more enrollment declines are likely this year due to higher out-of-pocket premiums with the enhanced tax credits expired.

A significant number of Marketplace enrollees are expected to lose their coverage mid-year because they fail to make premium payments, which have increased by an average of 58% from $113 to $178. Accounting for this drop from unpaid premiums as well as mid-year attrition and other factors, Wakely estimates that average effectuated enrollment in the individual market could decline by 17% to 26% between 2025 and 2026.

Who Dropped Marketplace Coverage and Where

Middle-income individuals represent a disproportionately larger share of those who dropped ACA Marketplace coverage during the 2026 Open Enrollment Period. When the ACA’s enhanced subsidies expired, the “subsidy cliff” reemerged, causing many middle-income people to drop their coverage because they earned too much to qualify for standard subsidies but too little to afford unsubsidized premiums.

People with incomes over this subsidy cliff (400% or more of the federal poverty level, or $62,600 for a single person in 2026) made up just 7% of 2025 Marketplace enrollment but nearly half (48%) of the decline in plan selections from 2025 to 2026.

Most states experienced major drops in ACA sign-ups. Marketplace sign-ups fell in 41 states, with the largest drops seen in North Carolina (22%), Ohio (20%), West Virginia (17%), and Indiana, Delaware, and Arizona (all 16%). Many of these states saw rapid Marketplace enrollment growth under the enhanced subsidies, suggesting that higher out-of-pocket premium contributions following their expiration may have led some Marketplace enrollees to drop their coverage.

State-based exchanges, many of which have their own supplemental premium subsidy programs and more robust outreach efforts, tended to retain higher shares of enrollees than states with federally facilitated exchanges.