rewrite this content and keep HTML tags Hospital Expenses per Adjusted Inpatient Day

Source link

Hospital Expenses per Adjusted Inpatient Day

President Trump Proposes Codifying MFN Drug Pricing Deals But Key Details Are Missing

rewrite this content and keep HTML tags

In his new “Great Healthcare Plan,” President Trump has proposed to “codify” the administration’s most-favored-nation (MFN) drug pricing deals that have been agreed to by drug companies in recent months. These MFN agreements are based on the premise that the U.S. shouldn’t pay higher prices for prescription drugs than the prices paid in other comparable nations, an idea that President Trump promoted in his first term through various proposals that were ultimately not implemented.

In this second term, the Trump administration has conducted dealmaking behind the scenes to negotiate most favored nation pricing agreements with individual drug companies, bypassing more traditional regulatory or legislative approaches to secure these deals. The manufacturers have agreed to make certain products available to state Medicaid programs at most favored nation pricing, to introduce new medications at most favored nation pricing in the U.S., and to sell certain products directly to U.S. consumers at discounted prices. The manufacturers are also committing to increase their investment in U.S. manufacturing and in return they’ll receive a 3-year reprieve from tariffs that would otherwise be imposed.

In general, the details of these agreements remain confidential, which means that very little is known publicly about what exactly has been agreed to. Although price discounts for specific drugs were highlighted at various White House events, the full scope of these deals – including which drugs are subject to these agreements, what specific pricing has been agreed to, and how MFN prices are determined – is largely unknown.

As a result, it’s difficult to understand what it would mean to “codify” these deals. It’s also not clear what the mechanism would be for extending these deals to all Americans. While codifying most-favored-nation drug pricing could be helpful for bringing more transparency to these arrangements and guaranteeing that drug companies will deliver on what they’ve promised, policymakers would need substantially more information to turn these backroom voluntary deals into law.

Higher Premium Payments or Higher Deductibles: The Tradeoffs ACA Enrollees Face

rewrite this content and keep HTML tags

Some Affordable Care Act (ACA) Marketplace enrollees are choosing between plans that charge higher premium payments and plans with higher deductibles. Many enrollees are considering these tradeoffs following the expiration of the ACA’s enhanced premium tax credits at the end of 2025, according to a new Health System Tracker analysis.

While switching from a silver plan to a bronze plan could lower premium payments, the loss of cost-sharing reductions for deductibles and copays and the higher cost-sharing associated with a bronze plan may leave these enrollees worse off financially, depending on how much care they need.

The full analysis and other data on health costs are available on the Peterson-KFF Health System Tracker, an online information hub dedicated to monitoring and assessing the performance of the U.S. health system.

How Unaffordable is Health Care?

rewrite this content and keep HTML tags

In his latest JAMA Forum column, KFF’s Larry Levitt explores how unaffordable health care is in the U.S. in the context of the debate over extending enhanced Affordable Care Act premium tax credits and an upcoming election where affordability will likely be front and center.

Trump Has No Health Plan, He Has the Art of the Health Care Deal

rewrite this content and keep HTML tags

President Trump is often derided for not having a health reform plan, or even his “concepts of a plan” he’s talked about, or more narrowly, a plan to replace the ACA and its enhanced tax credits currently under debate. It’s true he has none of these. But he does have a distinctive game plan of sorts that’s unlike anything we’ve seen before: a series of one-off deals with the health care industry. Most rely on presidential jawboning and voluntary action by industry groups. Some have the threat of regulatory action to go along with hard-edged presidential persuasion. They have the character more of real estate deals than “plans.” Or they’re more similar to Trump’s approach to some of what he calls his foreign policy “deals” (like the current attempt at a peace deal in Ukraine). Or his tariff deals that come and go. To use a word commonly associated with Trump, it’s health policy by transaction.

The plans are far from comprehensive health reform plans addressing coverage and costs and they don’t change the long-term profit incentives of the health care companies that participate in the deals. They in no way offset the huge cuts in Medicaid and the ACA made on his watch. Still, they signify action to voters on issues they care about, can capture news cycles, and even do some good, like lowering some drug prices, at least temporarily. The benefits of some of the deals are exaggerated as Trump is wont to do. A big question about them is whether they have staying power.

There have been three major deals so far, and Trump has started to talk up a fourth deal that, at first blush, sounds bigger than all the others combined.

Trump’s first big set of deals was with the drug companies. It began with deals with three, then eventually nine, drug companies to lower prices on drugs provided to Medicaid beneficiaries, characterized as part of a voluntary “most favored nation” (MFN) policy aligning prices with those paid by other wealthy nations, in return for reported tariff relief. (Whether these deals actually lower costs for Medicaid programs below the rebates they currently get is not my focus here.) Trump also made deals with Eli Lilly and Novo Nordisk to cut GLP-1 prices voluntarily for some patients and to sell the drugs to others on TrumpRx. The Center for Medicare and Medicaid Innovation is to test out models for MFN targets, and regulations have now been promulgated to codify the MFN policy, potentially giving it staying power, at least for some drug prices. For a discussion, see our Wonk Shop.

The administration also announced a voluntary effort with big health insurance companies to speed up and simplify prior authorization review, including promised reforms to cut back on what is reviewed and how often. The effort is expected to kick in this year, though follow through by the companies is TBD and merits scrutiny. The public is beyond frustrated with prior authorization review, as are physicians, but only 20% of the public was aware of the announcement when it was made in June, and few had much faith that it would produce results. Somewhat incongruously, at the same time as they were cutting back on prior authorization review, the administration also announced a demonstration project to introduce targeted prior authorization review to traditional Medicare for the first time, focusing on procedures it sees as prone to fraud and abuse.

Another Trump voluntary initiative led by CMS is a partnership with more than 60 providers, payers and software companies to improve electronic patient information sharing and give consumers better digital tools to use to navigate the health system and public programs. The partnership would require that some companies commit to inter-operability but generally presents participating companies with more new opportunities to make money than sacrifices.

And just before the holidays, in what would be by far the most ambitious deal yet, the president turned to what sounded like a fourth deal in the works, talking the health insurance industry into lowering their premiums.

Trump’s characterization of what might happen was grandiose:

“We should have a meeting, and we should talk to them because I would say that maybe with one talk, they would be willing to cut their prices by 50, 60, or 70%. They’ve made a fortune.”

Trump’s rhetoric is often exaggerated, and it’s possible he was mixing up profits and prices in his remarks or even that this deal will not materialize. Still, he said what he said, and cuts of that magnitude are fanciful. However inflated the premiums charged by health insurance companies may be, they do reflect the underlying costs of hospitals, outpatient care, drugs and the entire health system, and cannot simply be cut in half.

The would-be insurance company initiative is illustrative of the “make a deal” approach: jawbone, negotiate in some fashion, make a deal, keep it simple and understandable to voters, and announce it with fanfare and usually lots of exaggeration, with no broader plan and without addressing the underlying causes of the problem. Still, any concessions made by the insurance industry would be a political win for Trump, garner news coverage, and at least appear to address voter concerns about affordability in a tangible way. It could also be argued that Trump’s deals, however limited and exaggerated they may be, are disruptive in a positive way. Trump’s drug deals, for example, have helped move the drug industry from politically untouchable to fair game. Similarly, his policies towards Russia and Europe are reprehensible to many but have resulted in Europe coming together and increasing defense spending in response.

There’s an infamous example of a voluntary effort to restrain costs in health care under threat of government action that taught us a lot. It happened in the late 1970s and was called the Voluntary Effort. The shorthand was the “VE.”

President Jimmy Carter and then Health, Welfare, and Education Secretary Joesph Califano put together what was probably the most aggressive cost containment plan ever in health care, featuring a cap on hospital revenue growth. (Bill Clinton had an aggressive one as well, proposing to cap increases in insurance premiums). Carter’s plan failed partly when the industry, led by virtually every major industry group, promised a voluntary effort to restrain hospital expenditure growth by 2 percentage points below 1977 rates. Growth rates were so high then (partly due to high inflation) that the target rates for 1978 and 1979 were 13.6% and 11.6%, respectively, which is hard to fathom now as we complain mightily about much smaller increases. As I captured in our Sad History of Health Care Cost Containment As Told in One Chart article years ago, a Health Affairs article I wrote with Larry Levitt, the impact of the VE was short lived, but Carter’s cost plan died in Congress in 1979, partly due to the VE.

Trump’s VEs are a little different. They are not industry efforts to ward off government action so much as deals initiated by President Trump to achieve short term gains (arguably in some cases) and create at least the appearance of progress on the issue of the day—affordability—and of action on “health reform.”

In the larger picture, by no accounting can the benefits of these one-off deals offset the combined impact on the public of the nearly trillion dollars in Medicaid cuts that will kick in over the next 10 years and the premium spikes that will hit Marketplace enrollees if the enhanced tax credits are not extended, as now seems inevitable. I doubt President Trump connects these dots. His approach isn’t about a policy direction he’s pursuing, or a health reform plan, or a bigger picture—it’s a series of deals. There are likely more to come.

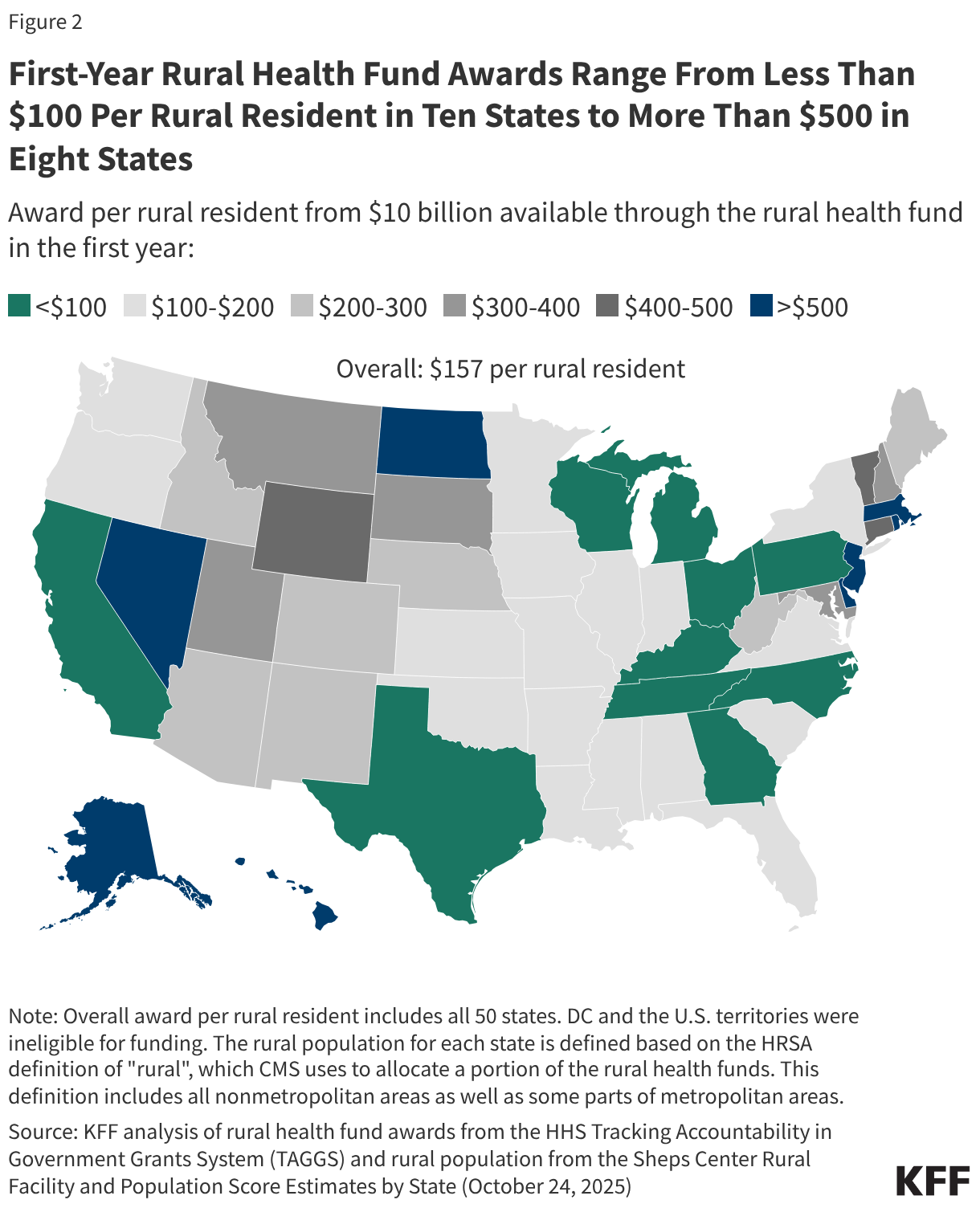

First-Year Rural Health Fund Awards Range From Less Than $100 Per Rural Resident in Ten States to More Than $500 in Eight

rewrite this content and keep HTML tags

On December 29, 2025, the Centers for Medicare & Medicaid Services (CMS) announced first-year state awards from the $50 billion Rural Health Transformation Program (the “rural health fund”), which is being administered by a new Office of Rural Health Transformation. The rural health fund was created as part of the July 2025 budget reconciliation law, sometimes called the One Big Beautiful Bill, to help offset the impact on rural areas of the law—which includes an estimated $911 billion in federal Medicaid spending reductions over ten years, including an estimated $137 billion in rural areas. All 50 states applied for the rural health fund, and each state received an award. CMS will distribute $10 billion each year from fiscal years 2026 through 2030, beginning this year.

State awards for 2026, the first of five years, average $200 million, ranging from $147 million in New Jersey to $281 million in Texas (Figure 1). Differences in total awards across states in the first year (and most likely in future years) are modest relative to large differences in rural populations and rural health needs more generally. For example, Texas has about thirty times as many rural residents as New Jersey (4.3 million versus about 140,000) but is only receiving about twice as much funding in the first year ($281 million versus $147 million). Differences in total awards across states are relatively modest primarily because half of the rural health fund (50%) is being distributed equally across approved states, regardless of need, as required by law. Because all states have been approved for funding, each is slated to receive $100 million from this half of the fund in 2026 and in each year from 2027 through 2030.

Texas, Alaska and California are receiving the largest total awards in the first year. While Texas and California have the largest and fourth-largest rural populations in the country, respectively, Alaska has the fifth smallest rural population. Alaska likely received a relatively large award at least in part because a portion of the fund was distributed to the five largest states based on land area. New Jersey, Connecticut, and Rhode Island are receiving the smallest awards in the first year. These are all states with relatively small rural populations.

Figure 1

First-year awards per rural resident vary widely across states, ranging from less than $100 in ten states to more than $500 in eight states according to KFF analysis (see Figure 2). State awards are partially, but not closely, tied to rural population, meaning that first-year awards per rural resident are generally relatively small among states with the largest rural populations. For example, Texas has the largest rural population in the country—and the largest total award in the first year—but will receive the smallest payment per rural resident ($66 in 2026). In contrast, states like Rhode Island, New Jersey, and Alaska, with far fewer rural residents, will receive substantially higher amounts per rural resident ($6,305, $1,069, and $990 respectively, with Rhode Island being an extreme outlier). Only a quarter of the $50 billion fund is being distributed exclusively based on measures of state need, with just 5% of the fund that is based on rural population. Other measures of need, according to CMS, include the number of rural facilities, land area, the share of hospitals receiving Medicaid disproportionate share hospital (DSH) payments, and other factors.

While lawmakers created the fund in part to help offset the impact on rural hospitals of cuts under the reconciliation law, CMS has made clear that funding is intended to benefit rural communities more broadly by transforming health care systems. Examples of state initiatives based on the subset of state applications available to the public and abstracts posted on CMS’s website include initiatives related to Make America Healthy Again (MAHA) (such as improving access to healthy foods and preventing and managing chronic conditions), expanding telehealth services and remote patient monitoring, rural workforce development programs, and supporting regional collaboration among providers.

CMS stipulates that payments to hospitals and others for patient care cannot exceed 15% of total funds, though providers could benefit in other ways, such as through investments in existing buildings and infrastructure (restricted to 20% of total funds). It is unclear how much of the money will benefit rural hospitals either directly or indirectly and the extent to which this will offset hospitals’ losses under the reconciliation bill. Moreover, it is not yet clear how much information will be available to the public to track the flow of dollars from states to rural providers and other entities and to evaluate the effectiveness of state initiatives.

This work was supported in part by Arnold Ventures. KFF maintains full editorial control over all of its policy analysis, polling, and journalism activities.

What to Know About Pharmacy Benefit Managers (PBMs) and Federal Efforts at Regulation

and Federal Efforts at Regulation")

rewrite this content and keep HTML tags

The price of prescription drugs in the U.S. continues to be a concerning issue to the public, with KFF polling consistently showing the public supports various approaches to lowering prescription drug costs. Efforts to rein in drug costs have long been a priority for both federal and state policymakers. The Trump administration has recently taken steps to address drug costs through Executive Orders and multiple pricing agreements to bring ‘Most Favored Nation’ pricing to consumers in the U.S., though the impact and savings from these efforts are not yet known. The Biden administration enacted the Inflation Reduction Act of 2022, which authorized the federal government to negotiate lower drug prices with manufacturers for some drugs covered by Medicare, among other provisions, resulting in an estimated reduction in the federal deficit of $237 billion over 10 years for the drug pricing provisions alone.

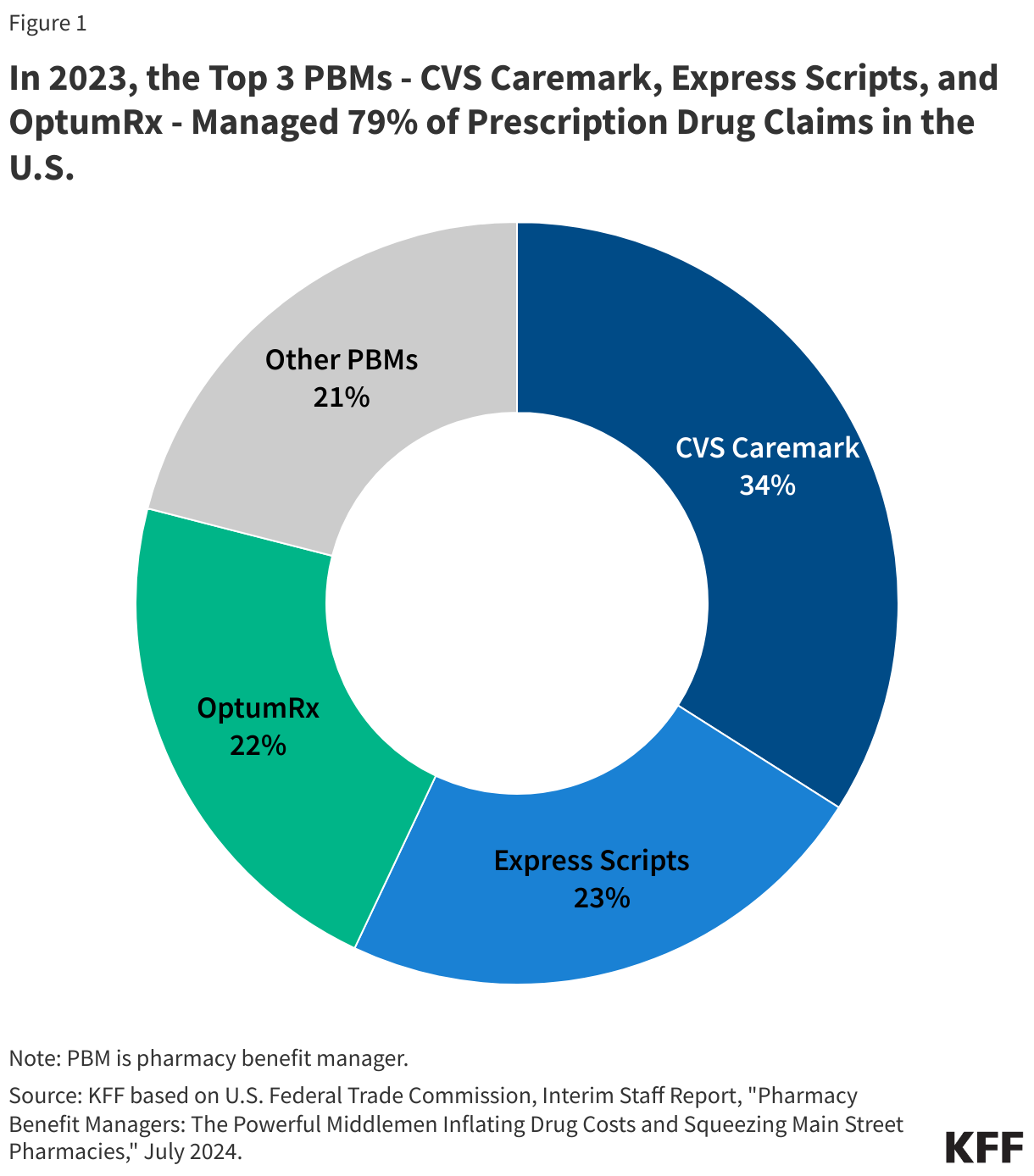

One player in the system of pharmaceutical pricing in the U.S. that has come under increasing scrutiny in recent years is the pharmacy benefit manager, or PBM. These so-called ‘middlemen’ are used by health insurance companies to manage their pharmacy benefits. PBMs have been the focus of attention from policymakers for several reasons, including their business practices, market consolidation, and lack of transparency, all of which factor into concerns that PBMs themselves have played a role in increasing drug prices, even as they work to manage pharmacy benefits and costs for insurers.

In an April 2025 Executive Order, the Trump administration directed the Assistant to the President for Domestic Policy to reevaluate the role of ‘middlemen’ to “promote a more competitive, efficient, transparent, and resilient pharmaceutical value chain”. In the current session of Congress, legislation addressing various concerns related to PBMs and their business practices has been introduced and voted on but not enacted, including provisions in recent House GOP legislation responding to the expiration of the enhanced ACA premium subsidies, which passed the House in December 2025, and in budget reconciliation legislation passed by the House but not the Senate in May 2025. This brief provides an overview of the role of PBMs in managing pharmacy benefits, discusses recent federal legislation focusing on several elements of PBM business practices, and explains the potential federal budgetary impact of this legislation, which would have a relatively modest impact on the federal deficit, based on available CBO estimates. (This brief focuses on actions at the federal level and does not address state legislative efforts related to PBMs, which have occurred in all 50 states.)

The Role of PBMs

Pharmacy benefit managers (PBMs) act as intermediaries between drug manufacturers and insurance companies that offer drug benefits to employer health plans, Medicare Part D prescription drug plans, state Medicaid programs, and other payers. In this role, PBMs serve several functions: negotiating rebates and price discounts with drug manufacturers, processing and adjudicating claims, reimbursing pharmacies for drugs dispensed to patients, structuring pharmacy networks, and designing drug benefit offerings, which includes developing formularies (lists of covered drugs), determining utilization management rules, and establishing cost-sharing requirements.

Although there are many PBMs, a few companies dominate the overall U.S. market. According to the Federal Trade Commission (FTC), the top 3 PBMs – OptumRx (owned by UnitedHealth Group), Express Scripts (owned by Cigna), and CVS Caremark (owned by CVS Health, which also owns Aetna) – manage 79% of prescription drug claims on behalf of 270 million people in 2023 (Figure 1).

Certain PBM Business Practices Have Given Rise to Concerns About Their Impact on Drug Prices

Sources of revenue: PBMs generate revenue in different ways. PBMs are typically paid fees for the functions they serve managing pharmacy benefits. PBMs also negotiate rebates with drug manufacturers in exchange for preferred placement of rebated drugs on a health insurance plan formulary, and they may retain a portion of the drug rebates they negotiate, though this may be more common in the commercial employer market than in the Medicare Part D market. Many state Medicaid programs and Medicaid managed care plans also contract with PBMs to manage or administer pharmacy benefits, including negotiating supplemental prescription drug rebates with manufacturers.

Rebates can help lower the cost of drug benefits for health insurers, which enables them to offer lower premiums in turn and may translate to lower out-of-pocket costs for patients at the point of sale. In order for PBMs to maximize rebate revenue, however, they may favor higher-priced drugs with higher rebates over lower-priced drugs with low or no rebates in their negotiations with drug companies. This may have an inflationary effect on drug pricing by manufacturers, increase costs for payers across the system, and raise out-of-pocket costs for patients who pay based on the list price – a particular concern for those without insurance but also for those with high-deductible insurance plans or when cost sharing is calculated as a percentage of the drug’s price, such as for Part B drugs under Medicare.

Because of these impacts, some have suggested that rebates negotiated between PBMs and drug manufacturers should be passed along in full to individuals at the point of sale and make discounts available upfront at the pharmacy counter. This arrangement would produce savings for individuals who take drugs with high rebates, since they would face lower out-of-pocket costs on their medications when they fill their prescriptions. However, if rebates are no longer being used to reduce a plan’s overall drug benefit costs, point-of-sale drug discounts could result in higher premiums for all plan enrollees.

Spread pricing: Another potential source of revenue for PBMs comes from the contracting practice of spread pricing, which is when a PBM pays a lower rate for a drug to the dispensing pharmacy than the amount the PBM charges an insurer for that drug and retains the difference or “spread” as profit. The practice of spread pricing can result in higher costs for insurers, while lower reimbursement levels put financial pressure on pharmacies.

PBMs have come under bipartisan scrutiny in recent years for spread pricing arrangements in Medicaid managed care that have increased Medicaid costs for states and the federal government. As a result, a number of states have prohibited spread pricing or adopted other reforms to increase transparency and improve oversight. Concerns about Medicaid spread pricing also led the Centers for Medicare & Medicaid Services (CMS) to issue an informational bulletin in May 2019 about how managed care plans should report spread pricing, which may have reduced the practice.

Consolidation: Consolidation in the PBM market has enabled a few PBMs to gain significant market power. As mentioned above, three PBMs manage nearly 80% of all prescription claims in the U.S. Moreover, the top three PBMs are vertically integrated with major health insurers: OptumRx is owned by UnitedHealth, Express Scripts is owned by Cigna, and CVS Caremark is owned by CVS Health, which also owns Aetna. Each of these PBMs also own mail order pharmacies and specialty pharmacies.

The FTC and members of Congress on both sides of the aisle have raised concerns that this level of market concentration and vertical integration enables PBMs to steer consumers to their preferred pharmacies, mark up the cost of drugs dispensed at their affiliated pharmacies, reimburse PBM-affiliated pharmacies at a higher rate than unaffiliated pharmacies for certain drugs, and apply pressure over certain contractual terms, all of which may disadvantage unaffiliated and independent pharmacies, contributing to pharmacy closures.

Transparency: Financial contracts between PBMs and drug manufacturers, including drug pricing information and the rebate arrangements that PBMs negotiate with drug manufacturers, are generally not made public. This means that plan sponsors often do not have insight into how much PBMs are actually paying for drugs on their formularies, and PBMs often consider this information to be proprietary. In the pharmaceutical supply chain as whole, many players operating in this market do not have information about prices, which can make informed decision-making difficult and imperfect.

In recent years, federal lawmakers have focused several Congressional hearings on the topic of PBMs, including their role in prescription drug pricing, drug spending growth, and rising out-of-pocket costs for drugs, and have introduced legislation focusing on several elements of PBM business practices. The legislation highlighted below is not an exhaustive list but includes some of the more recent and prominent legislative efforts in the 119th Congress.

In May 2025, the House passed a version of the 2025 federal budget reconciliation law that included several provisions that would have addressed some PBM operations, though the PBM provisions were not included in the final version of the bill that was passed by Congress and signed into law in July 2025 (sometimes referred to as the “One Big Beautiful Bill Act”). The provisions in the May 2025 House-passed budget reconciliation bill include:

- Delinking PBM compensation from drug prices, rebates, and discounts that they negotiate for drug plans under Medicare Part Dand instead basing compensation on a ‘bona fide service fee’, which would be a flat dollar amount.

- Establishing transparency and reporting requirements for PBMs, including data on utilization, pricing, and revenues for formulary covered drugs; PBM-affiliated pharmacies; contracts with drug manufacturers; and other PBM business practices. This provision would require PBMs to provide this data to Part D plan sponsors as well as the HHS Secretary.

- Prohibiting spread pricing in Medicaid and instead basing payments on a ‘pass-through model’ in which payments made by a PBM on behalf of the State Medicaid program to the pharmacy are limited to the drug ingredient cost and a professional dispensing fee. Payments to PBMs and similar entities would be required to reflect the pharmacies’ costs and an administrative fee that is fair market value.

- Ensuring accurate payments to pharmacies under Medicaid: All retail pharmacies and certain non-retail pharmacies would be required to complete the National Average Drug Acquisition Cost (NADAC) survey, if they are selected for participation in the survey. This provision would require survey participation across all retail pharmacies, including larger chain pharmacies who have historically not participated in the survey and who likely obtain their drugs at lower prices, which could lower pharmacy reimbursement for some drugs and result in federal and state savings.

In December 2025, the House passed GOP legislation responding to the expiration of enhanced ACA premium subsidies, the Lower Health Care Premiums for All Americans Act (H.R. 6703), which included a separate PBM provision that would increase oversight of PBMs that provide services to employer group health plans through data transparency and reporting requirements. This provision would require PBMs to report detailed prescription drug utilization and spending data to plans, including gross and net spending, out-of-pocket spending, pharmacy reimbursement, and other details related to the plan’s pharmacy benefit.

Separately, reflecting the bipartisan support for legislation related to PBMs, Representatives Buddy Carter (R) and Vincente Gonzalez (D) introduced the PBM Reform Act of 2025 in the House, while the chairman and ranking member of the Senate Finance Committee, Senators Mike Crapo (R) and Ron Wyden (D), introduced the Pharmacy Benefit Manager (PBM) Price Transparency and Accountability Act in the Senate. These bills are similar but not the same; the PBM Reform Act of 2025 includes the provision that would increase oversight of PBMs that work with employer group health plans (as in the broader House GOP bill), which is not included in the PBM Price Transparency and Accountability Act. A bipartisan group of representatives, including Representatives Jake Auchincloss (D), Diana Harshbarger (R), and James Comer (R) also recently reintroduced the Pharmacists Fight Back Act, which includes two coordinated pieces of legislation that would regulate PBMs in certain federal health benefits programs.

- The PBM Reform Act of 2025 (H.R.4317) includes most of the PBM provisions that were included in a preliminary version of the budget reconciliation bill that passed the House in May 2025 and includes: delinking PBM compensation from the cost of medications for drug plans under Medicare Part D, prohibiting spread pricing in Medicaid, and ensuring accurate payments to pharmacies under Medicaid. In addition, the bill includes provisions to increase oversight of PBMs that work with employer group health plans and to assure pharmacy access and choice for Medicare beneficiaries, which were not included in the May 2025 House-passed bill.

- The provision to assure pharmacy access for Medicare beneficiaries would reinforce existing regulatory requirements that Part D plan sponsors contract with any willing pharmacy that meets their standard contract terms and conditions and have those conditions be ‘reasonable and relevant.’ These conditions would be defined and enforced according to standards determined by the Secretary of Health and Human Services (HHS).

- The PBM Price Transparency and Accountability Act (S.3345) also includes most of the PBM provisions that were included in the May 2025 House-passed bill and includes: delinking PBM compensation from the cost of medications for drug plans under Medicare Part D, prohibiting spread pricing in Medicaid, and ensuring accurate payments to pharmacies under Medicaid. Additionally, it includes the provision to assure pharmacy access and choice for Medicare beneficiaries, which was not included in the May 2025 House-passed bill.

- The Pharmacists Fight Back Act (H.R. 6609) and (H.R. 6610) would establish certain requirements with regard to PBMs in Medicare and Medicaid and in Federal Employee Health Benefits Plans, respectively. Plan sponsors (or PBMs acting on behalf of those sponsors) would be required to reimburse pharmacies for drugs based on pricing benchmarked to the National Average Drug Acquisition Cost (NADAC) and would be required to share a portion of rebates at the point of sale, with the remainder of the rebates being used to lower plan premiums. The legislation also prohibits PBMs from steering patients to PBM-affiliated pharmacies.

Budgetary Effects of PBM Legislation

In general, cost estimates from the Congressional Budget Office (CBO) have scored PBM provisions with relatively low savings to the federal government. CBO estimated a total federal deficit reduction of $3.2 billion over 10 years (2025-2034) attributable to the PBM provisions incorporated in the May 2025 House-passed budget reconciliation bill (which were not included in the final legislation enacted in July 2025):

- A reduction of $400 million from delinking PBM compensation from the cost of medications for drugs under Part D and establishing PBM transparency and reporting requirements

- A reduction of $261 million from prohibiting spread pricing in Medicaid

- A reduction of $2.5 billion from ensuring accurate payments to pharmacies under Medicaid

The provision to increase oversight of PBMs that work with employer group health plans was scored as part of the Lower Health Care Premiums for All Americans Act (H.R. 6703) that passed the House in December 2025. CBO estimated this provision would reduce the federal deficit by $1.9 billion over 10 years (2026-2035), with $1.8 billion in additional revenues and savings of $22 million. CBO assumes this provision would modestly reduce premiums charged in the group health insurance market, which could increase wages and therefore increase federal revenues.

CBO has not provided cost estimates for the PBM Reform Act of 2025, the PBM Price Transparency and Accountability Act, or the Pharmacists Fight Back Act. The provision to assure pharmacy access and choice for Medicare beneficiaries is not reflected in any of the cost estimates above. It is also possible that the effects of the Medicaid spending reductions in the budget reconciliation law will impact estimates of savings from the Medicaid PBM provisions. The law is expected to result in fewer Medicaid enrollees, which could lower Medicaid drug spending and translate to lower savings from Medicaid PBM provisions.

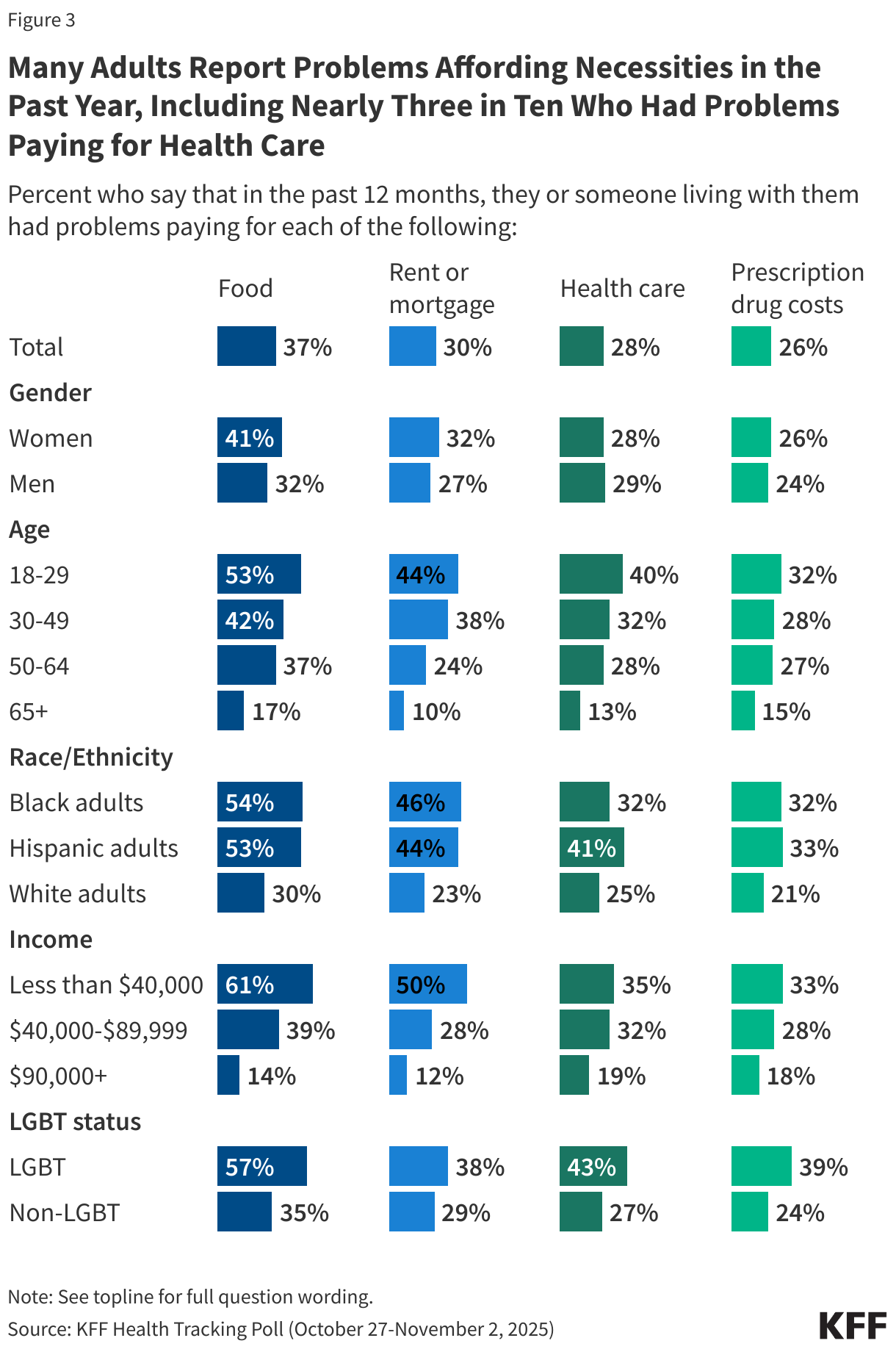

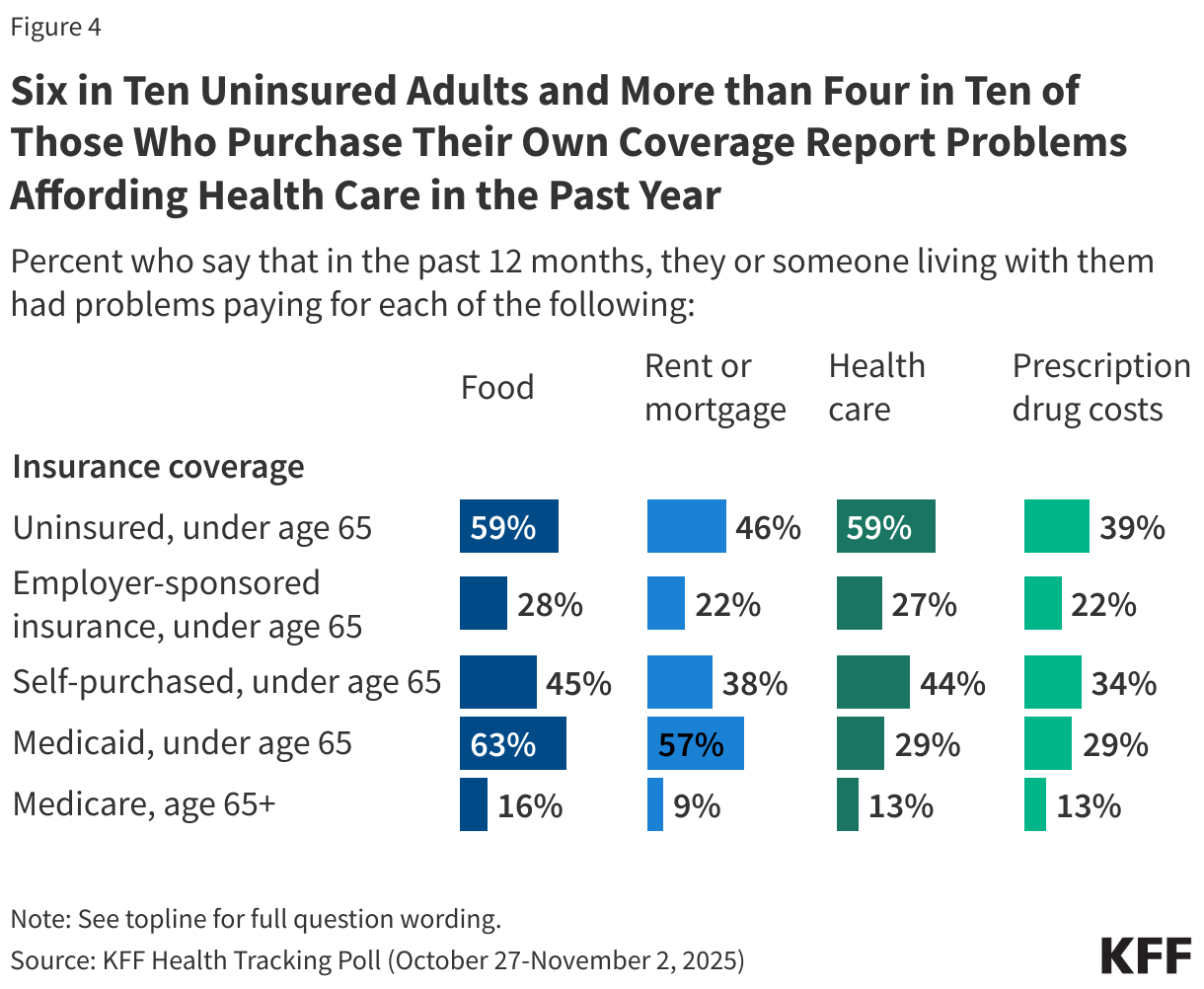

KFF Health Tracking Poll: Health Care Costs in the Current Moment of Economic Anxiety

rewrite this content and keep HTML tags

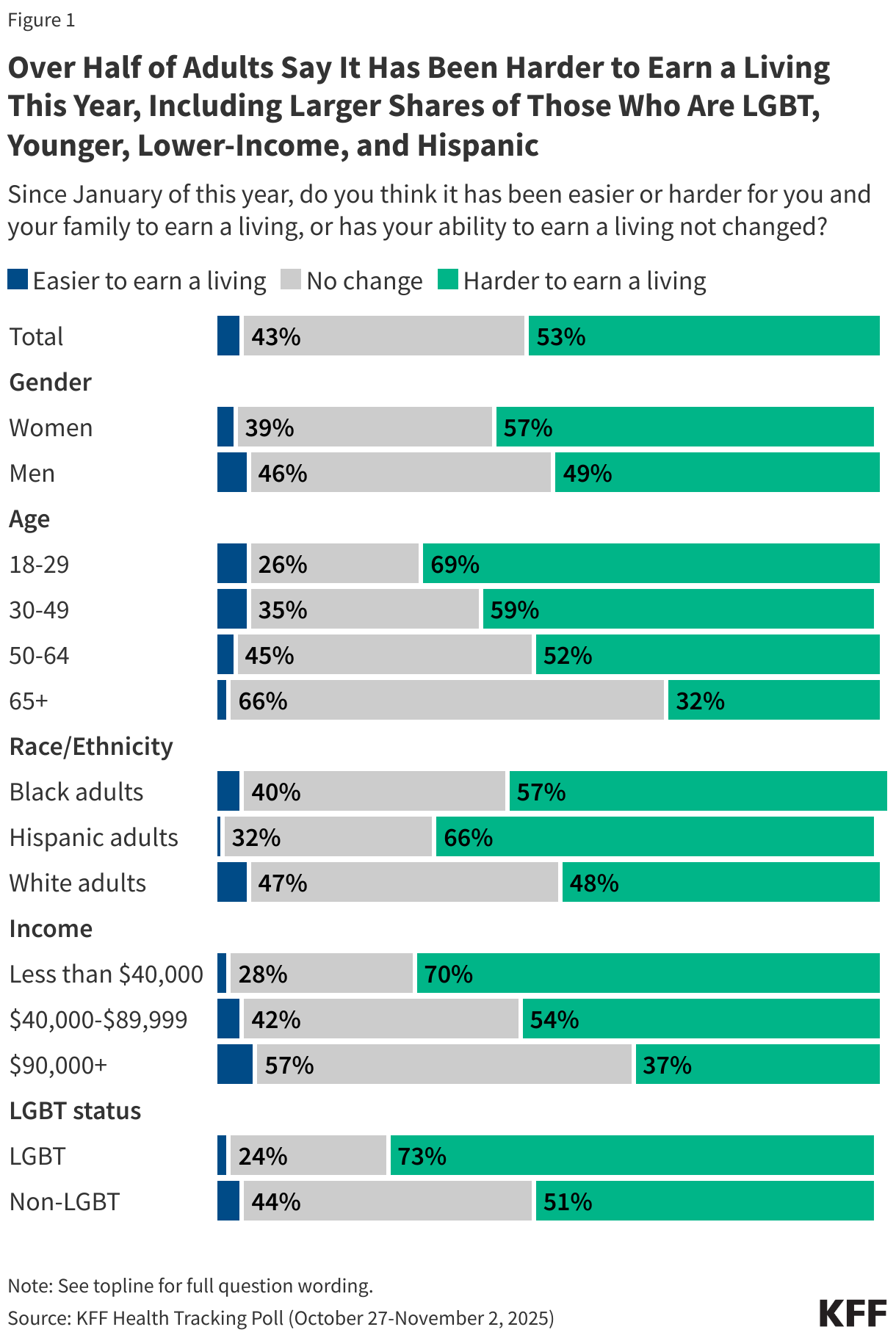

Multiple recent polls have found that economic anxiety in the U.S. is on the rise, and decades of KFF polling show how the rising cost of health care is a key component of people’s economic concerns. New data from the KFF Health Tracking Poll provide additional insights into who is struggling most in the current economy and how the cost of health care factors into those struggles. Overall, it shows that younger adults, LGBT adults, Hispanic adults, and those with more modest incomes are some of the groups most likely to report problems earning a living and affording health care and other necessities. Large shares of those who are uninsured or purchase their own insurance also report challenges earning a living and paying for care. Those with higher incomes are not immune from the problem of health care affordability; about one in five of those with incomes of $90,000 or more say their household had problems affording health care (19%) or prescription drugs (18%) in the past year.

Many adults are struggling to earn a living, particularly those who are LGBT, younger, Hispanic, and living in lower-to-moderate income households. A little over half (53%) of U.S. adults overall say it has been harder for them and their family to earn a living since January, while just 4% say it has been easier and four in ten (43%) say their ability to earn a living hasn’t changed. The share who report difficulty earning a living is higher among certain groups, with nearly three-quarters of LGBT adults (73%), seven in ten of those with household incomes under $40,000 (70%) and those ages 18-29 (69%), and two-thirds of Hispanic adults (66%) saying it has been harder to earn a living this year. Women are also somewhat more likely to report difficulty earning a living compared to men (57% vs. 49%).

Very few across groups say it has been easier for them and their family to earn a living this year, though the share is slightly higher among those with incomes of $90,000 or more (6%) compared to those with incomes under $40,000 (2%).

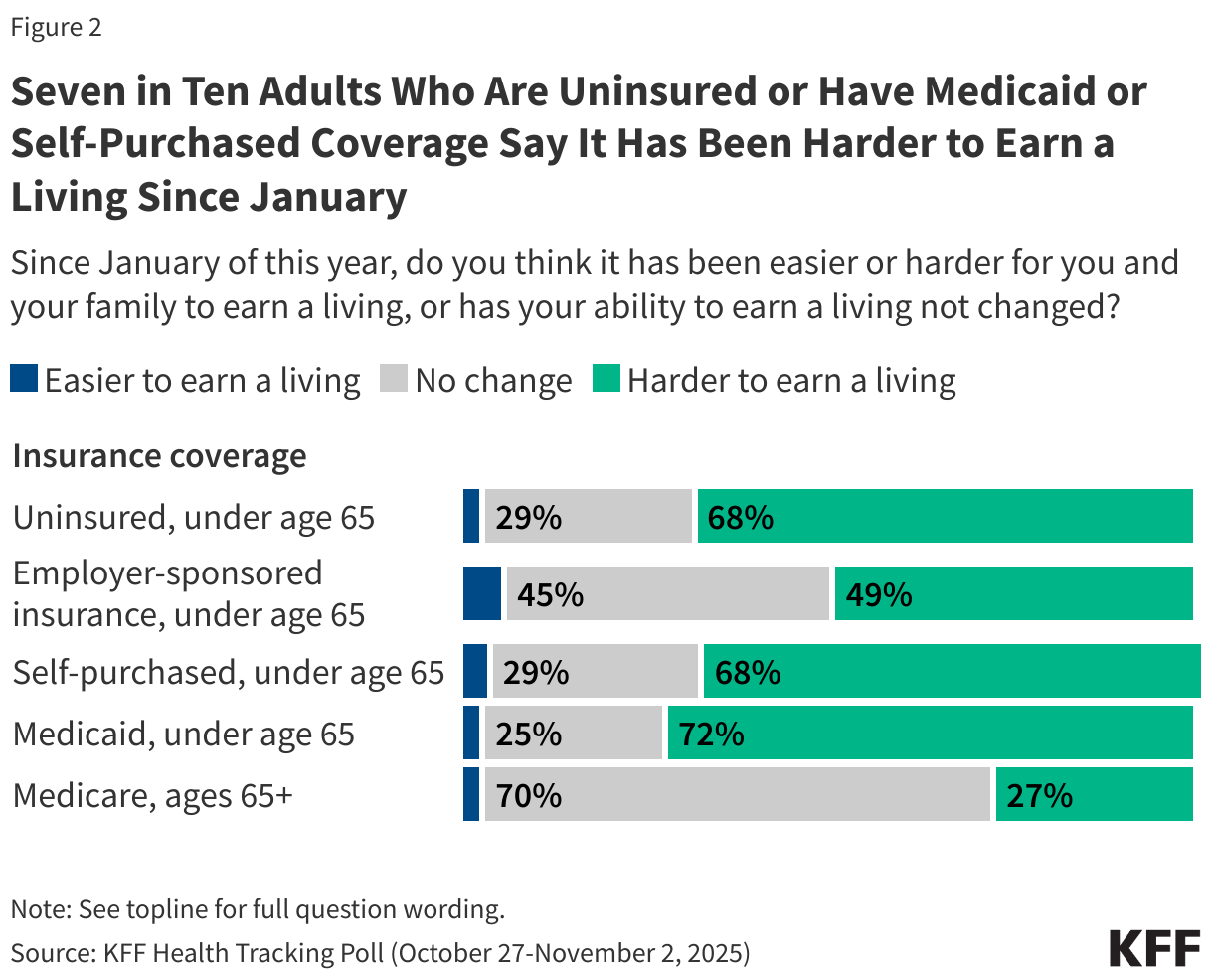

Uninsured adults and those with Medicaid or self-purchased insurance are more likely than those with employer coverage or Medicare to report difficulty earning a living. About seven in ten adults under age 65 who are uninsured (68%) or covered by Medicaid (72%) say it has been harder for them and their families to earn a living since January. The share is similar (68%) among those who purchase their own insurance, many of whom are self-employed or work in small businesses. By comparison, about half (49%) of those covered by an employer and just a quarter (27%) of adults ages 65 and over with Medicare coverage say it has been harder for them and their families to earn a living this year.

The cost of health care and prescription drugs is an important component of the financial struggles facing individuals and families in the current economy. Nearly four in ten adults overall (37%) report that their household had problems paying for food in the past year, while three in ten (30%) said they had problems paying their rent or mortgage. Problems affording health care are also common, with about three in ten (28%) saying they had problems paying for health care, up slightly from 23% in May 2025, and about a quarter (26%) reporting problems affording prescription drugs.

Problems affording each of these necessities are more common among the same groups who are most likely to say it’s been harder for their families to earn a living since January. For example, about six in ten of those in households earning less than $40,000 a year (61%) and at least half of LGBT adults (57%), Black adults (54%), Hispanic adults (53%), and adults under age 30 (53%) say their household had problems paying for food in the past twelve months.

Four in ten LGBT adults (43%), Hispanic adults (41%) and younger adults (40%) report problems paying for health care, higher than their non-LGBT, White, and older counterparts. While problems with health care affordability are somewhat higher among those with lower and moderate incomes, people with higher incomes are not immune. About one in five adults in households earning at least $90,000 a year say they had problems affording health care (19%) or prescription drugs (18%) in the past year.

Six in ten (59%) uninsured adults report problems paying for health care in the past year, as do more than four in ten (44%) of those who purchase their own coverage. Large shares of the uninsured and those who purchase their own coverage also report problems affording food (59% and 45%, respectively), housing (46% and 38%), and prescription drugs (39% and 34%). If Congress does not act before the end of this year to extend the enhanced premium tax credits for individuals who purchase coverage through the ACA Marketplace, those who purchase their own coverage are likely to face increasing financial hardship in the coming year.

Likely reflecting their lower incomes, about six in ten adults ages 18-64 with Medicaid coverage report problems paying for food (63%) and housing (57%) in the past year. Medicaid offers this population some protection from health care expenses, but still about three in ten say they had problems affording health care (29%) or prescription drugs (29%) in the past twelve months.

Recent Trends in Commercial Health Insurance Market Concentration

rewrite this content and keep HTML tags

Commercial health insurance markets remain highly concentrated across coverage types. However, the individual market, which consists mostly of the ACA Marketplaces, has attracted more insurers and witnessed greater insurer competition across a variety of measures since the implementation of the enhanced premium tax credits in 2021, according to a new Healthy System Tracker analysis.

For example, from 2020 to 2023, the average market share of the largest insurer in each state’s individual market declined from 60% to 53%, corresponding with enrollment growth in the ACA Marketplaces driven by the enhanced premium tax credits. By contrast, fully insured employer-sponsored health insurance markets have become less competitive in the past decade. The analysis presents 2013-2023 enrollment and market competition data for fully insured and individual plans both nationally and on a statewide basis.

The full analysis and other data on health costs are available on the Peterson-KFF Health System Tracker, an online information hub dedicated to monitoring and assessing the performance of the U.S. health system.