rewrite this content and keep HTML tags

While spending on prescription drugs accounts for a relatively small share of overall Medicaid spending, Medicaid drug spending has grown in recent years. As a result, both states and the federal government continue to prioritize the management of rising prescription drug costs. There have been several recent Trump administration prescription drug initiatives, including negotiating “most-favored-nation” (MFN) drug pricing deals. These MFN agreements are based on the premise that the U.S. shouldn’t pay higher prices for prescription drugs than other comparable nations. The deals include agreements by drug manufacturers to provide MFN pricing in Medicaid and other commitments in return for a 3-year reprieve from tariffs, though the specific details of these agreements remain confidential. Though prices vary across countries, studies have shown that drug prices in the U.S. are about three times higher than in other countries.

To make MFN drug prices available to state Medicaid programs, the Centers for Medicare & Medicaid Services (CMS) developed the GENEROUS (GENErating cost Reductions fOr U.S. Medicaid) Model, a drug payment model through which CMS will negotiate supplemental drug rebates based on prices paid in other countries. Given significantly lower drug prices internationally, this approach could result in substantial Medicaid savings, with a recently released White House report estimating that a voluntary MFN framework in Medicaid would save $64.3 billion over a 10-year period. While initial savings would be large and diminish over time – in part due to the fact that prices in other countries might increase as a result – savings would average $6.43 billion a year, or approximately 14% of annual Medicaid prescription drug spending.

However, it is unclear what assumptions were made to develop the administration’s estimates, and there remain several uncertain factors that make it difficult to assess the overall impact the new model will have on Medicaid drug costs. This issue brief provides background on the GENEROUS model, examines the factors that will contribute to the model’s overall impact on Medicaid drug costs, and illustrates how savings will depend on model details that are confidential or uncertain at this time. Key takeaways include:

- The impact of the GENEROUS model on Medicaid prescription drug spending remains unclear due to several uncertain factors related to drug pricing and model participation.

- Existing Medicaid rebates already reduce overall Medicaid prescription drug spending substantially, likely limiting the impact of the GENEROUS model’s MFN supplemental rebate approach.

- GENEROUS model savings will depend on which manufacturers and states participate as well as what drugs are included in the model due to variation in drug rebates (and net prices) as well as spending and utilization trends.

What Is the GENEROUS Model?

The CMS Innovation Center launched the GENEROUS model in January 2026 with the goal of lowering Medicaid drug spending by offering prices based on what other countries pay. The model is voluntary for manufacturers, though it is expected that the seventeen pharmaceutical companies (e.g. Pfizer, AstraZeneca, etc.) that have signed MFN agreements will participate. Manufacturers now have until June 11, 2026 to apply to participate in the GENEROUS model (the deadline has been extended twice from March 31, 2026 to April 30, 2026 and again to June 11, 2026). The model is also voluntary for states, with states having until July 31, 2026 to submit their application and until August 31, 2026 to execute a state participation agreement with CMS. States may be able to join the model after August 31, 2026 at CMS discretion. The model will run for five years through 2030, though manufacturers and states may voluntarily terminate their participation and key terms between CMS and manufacturers may be renegotiated.

Through the GENEROUS model, CMS will negotiate supplemental drug rebates based on prices paid in other countries (or the “MFN price”). For model drugs (single source or innovator multiple source drugs, also known as brand drugs), CMS will calculate the MFN price based on international pricing data provided by manufacturers across eight other countries (the United Kingdom, France, Germany, Italy, Canada, Japan, Denmark, and Switzerland). The MFN price is the second lowest reported net price after any rebates or discounts and is adjusted by gross domestic product per capita using a purchasing power parity method. CMS will then calculate the supplemental rebate for each model drug that results in a Medicaid net price equivalent to the MFN price (more specifics on the MFN price and Medicaid guaranteed net unit price calculations are available in both the state request for applications (RFA) and the manufacturer RFA). States can select which model drugs they’d like to receive MFN pricing for and must enter into new supplemental rebate agreements (SRAs) that reflect the model’s key terms (states cannot receive additional supplemental rebates outside of the model for drugs they have opted into).

CMS and participating manufacturers will also negotiate uniform coverage criteria, which includes utilization controls such as prior authorization or step therapy. These terms will be based on existing criteria states have negotiated, and states will have to adopt the uniform criteria to access the supplemental rebate for a given drug. States currently negotiate their own SRAs with manufacturers and use an array of payment strategies and utilization controls to manage prescription drug expenditures. States often use placement on a preferred drug list (PDL) and prior authorization as leverage to negotiate supplemental rebates with manufacturers, though the specific strategies vary by state. The negotiation of standardized coverage criteria could help reduce the administrative burden for states and manufacturers of negotiating individual SRAs tied to specific clinical criteria. However, the negotiated criteria may be more broad or more restrictive than the criteria states have already developed, which could have implications for state participation and model savings.

CMS will also conduct GENEROUS model monitoring and evaluation. The law requires Innovation Center models to either maintain or reduce program expenditures, and the model will test whether the MFN supplemental rebate approach can reduce Medicaid drug costs. To the extent negotiated clinical criteria broadens, the model may also increase enrollee access. Throughout the model, CMS will track data and assess the impact of the model on health care spending and access to care as well as audit the manufacturer reported international drug pricing data. GENEROUS works within the existing Medicaid Drug Rebate Program (MDRP) framework and builds on other CMS supplemental rebate models including the Cell and Gene Therapy Access Model and the BALANCE model. Notably, while these models aim to address high drug costs for the Medicaid program, they do not affect out-of-pocket costs for Medicaid enrollees, which are limited to nominal amounts under federal law.

What Are the Potential Impacts on Medicaid Prescription Drug Spending?

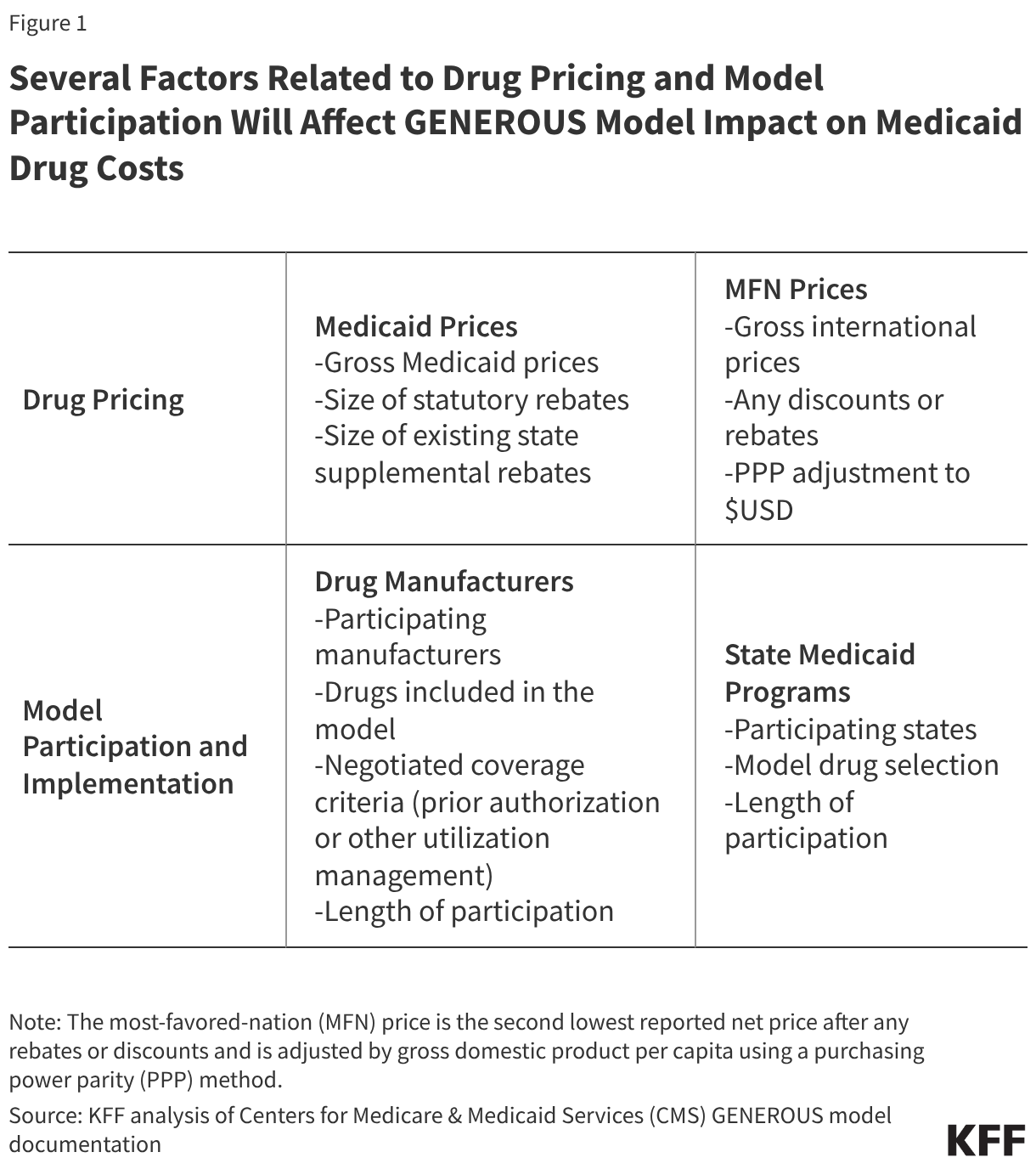

The impact of the GENEROUS model on Medicaid prescription drug spending remains unclear due to several uncertain factors related to drug pricing and model participation. Several factors will affect model cost savings (Figure 1), many of which are confidential or not yet available, including:

- While data on gross drug prices is available, data on the size of rebates for specific drugs is proprietary in both Medicaid and internationally, making it difficult to compare net Medicaid prices to net international prices.

- At this time, it also remains uncertain which manufacturers and states will participate in the model and how long participation will last.

- Further, while model documentation makes it clear that states may select model drugs, it remains uncertain whether all drugs in a participating manufacturer’s portfolio will be subject to the model. The RFAs note that “model drugs are limited to all the single source drugs or innovator multiple source drugs of a participating manufacturer”, indicating manufacturers must include all of their covered outpatient drugs. However, the RFAs also report that the listed terms may differ from the final terms, and a CMS presentation to states noted “manufacturers will opt into the model for certain branded Medicaid covered outpatient drugs”, leaving it uncertain whether all of a manufacturer’s drugs will be subject to MFN pricing or if exemptions will be available. Recent letters from the Senate Finance Committee sent to drug manufacturers push for more model details, including which drugs will be included in the model.

- Lastly, details on the uniform coverage criteria for model drugs have not been released, making it difficult to assess the impact the terms may have on drug spending or access.

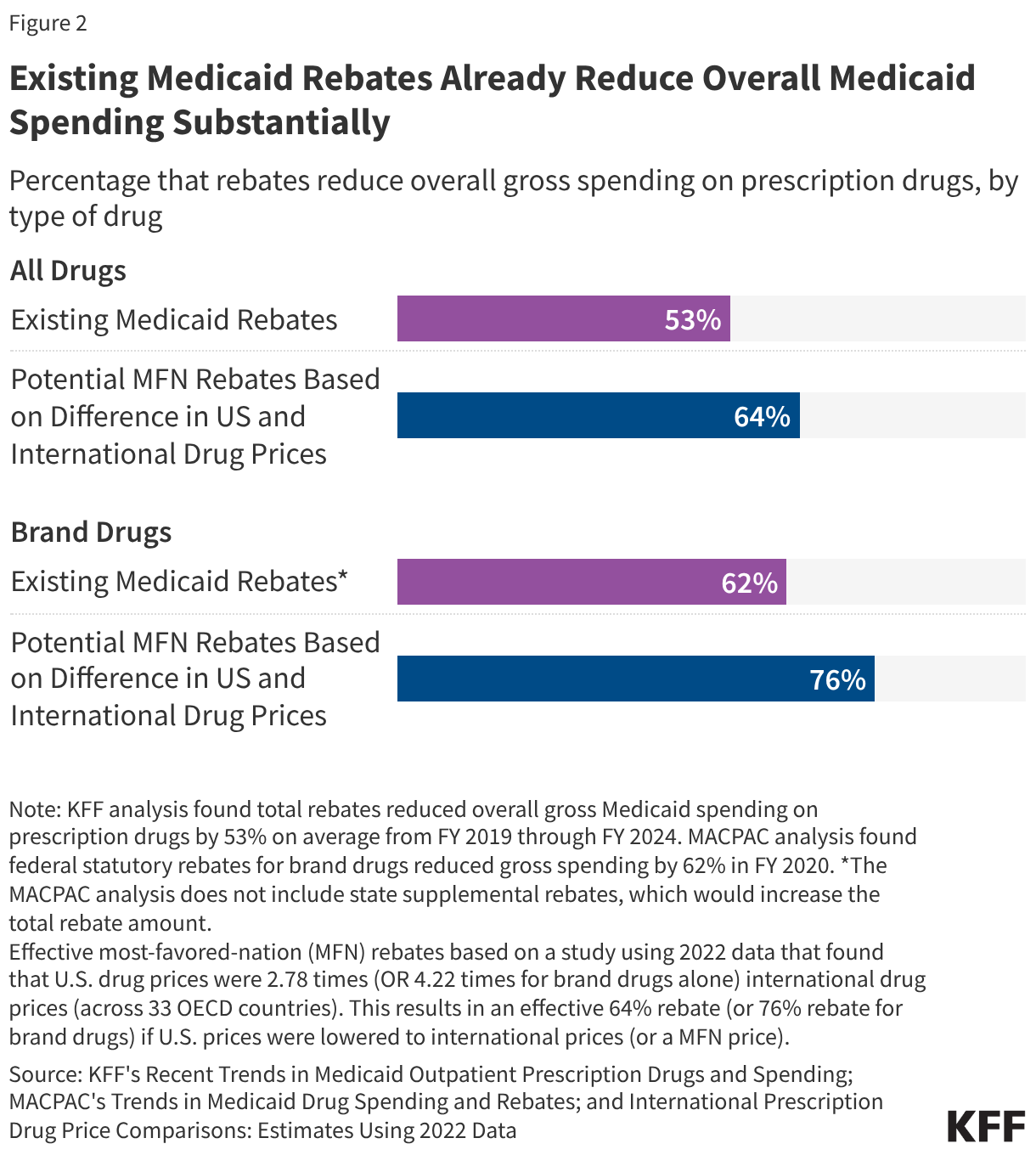

Existing Medicaid rebates already reduce overall Medicaid drug spending substantially, likely limiting the impact of the GENEROUS model’s MFN supplemental rebate approach. Medicaid programs already pay lower prices, net of rebates, than other payers due to the MDRP, which requires manufacturers to rebate a portion of drug payments to states. Medicaid rebates overall reduced gross Medicaid spending on prescription drugs by 53% on average from FY 2019 to FY 2024 (Figure 2). Rebates for brand drugs are typically even higher, with a Medicaid and CHIP Payment and Access Commission (MACPAC) analysis of FY 2020 data finding a 62% rebate overall for brand drugs.

At the same time, a recent study showed that U.S. drug prices overall were 2.78 times international drug prices (across 33 OECD countries); this differential is similar to those found in other research. Assuming U.S. drug prices are 2.78 times more than international prices, this would mean international prices are about one-third (36%) of U.S. drug prices. Based on this calculation, an MFN approach that reduced prices to international levels would provide a 64% rebate off existing U.S drug prices (Figure 2). The same study found U.S. brand drug prices were 4.22 times international drug prices, which is effectively a 76% rebate. While this is an illustrative example based on non-Medicaid specific drug prices in aggregate, it indicates that an MFN approach could provide substantial discounts given the large difference between drug prices in the U.S. and abroad. However, Medicaid already receives sizeable rebates, signaling there may be limits to this approach when applied to the Medicaid program.

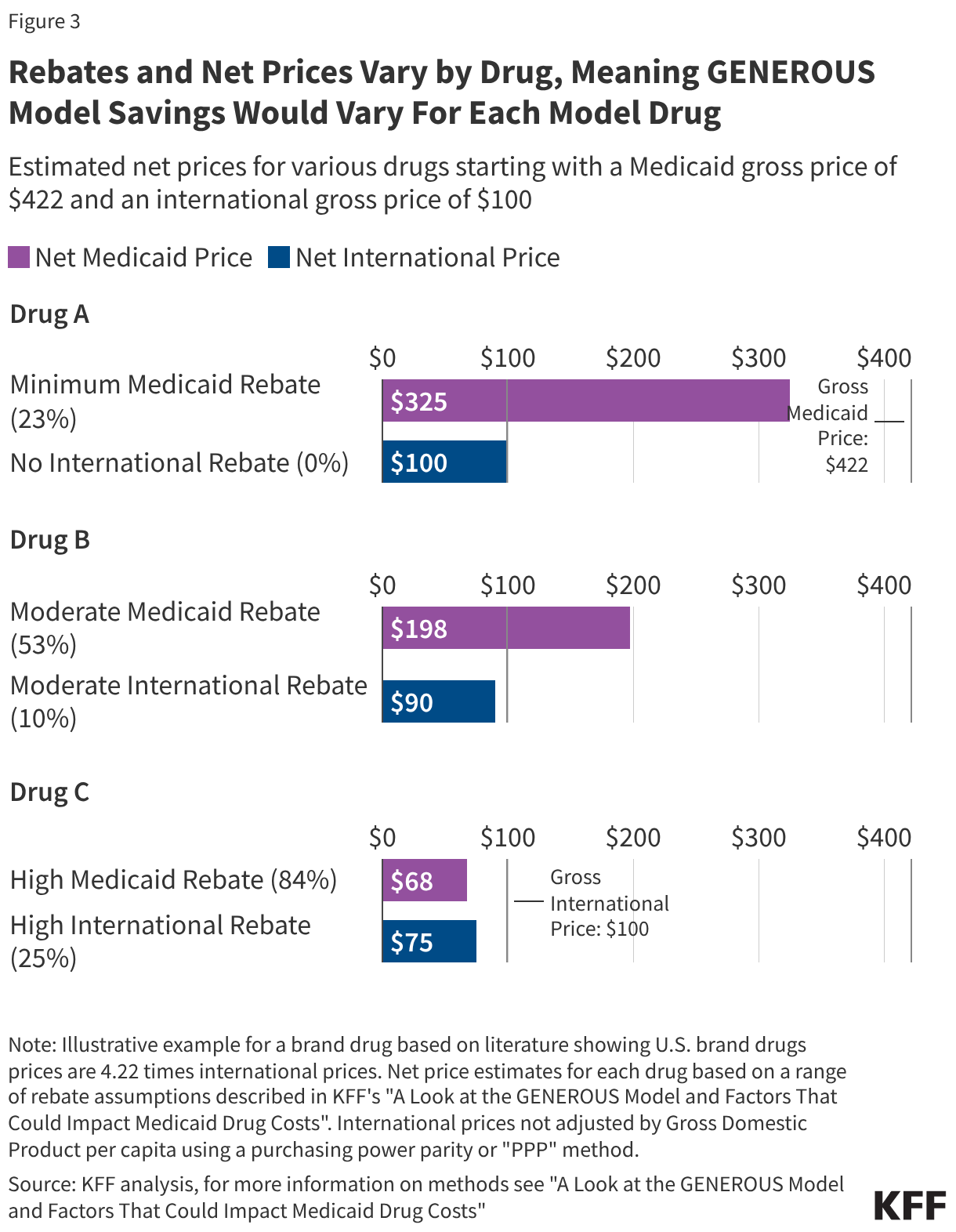

However, rebates and net prices vary substantially by drug, meaning GENEROUS model savings will vary for each model drug (Figure 3). While data on the total rebate for a specific drug is confidential, rebates vary substantially by drug. The minimum federal statutory rebate for a brand drug is 23.1%, but FY 2020 data shows statutory rebates for brand drugs subject to Medicaid’s best price provision and inflationary rebate component are generally much higher, reaching 77% overall. Further, as of January 1, 2024, there is no longer a cap on the total rebate amount if a drug’s price increases quickly over time, meaning overall rebates may now be even higher. In addition to these federal statutory rebates, states have been increasingly negotiating supplemental rebates with manufacturers, with supplemental rebates across states reducing gross Medicaid spending by 7% in FY 2024 (resulting in a higher total rebate estimate of 84% if added to the 77% in statutory rebates for some brand drugs). International countries in the model may also negotiate rebates or discounts. Available studies indicate rebates vary by type of drug and country, ranging anywhere from 0% of gross spending in Japan to about 25% or more in several model countries including Canada, Germany, France, Switzerland.

To illustrate, this analysis examines three example drugs (Drugs A-C), all with a gross Medicaid price of $422 compared with $100 internationally (based on the above study) but with different sized rebates (Figure 3). Some drugs, typically newer drugs with few (or no) competitors in their therapeutic class, may have smaller rebates and large gaps between the net Medicaid and net international price (like Drug A). For example, Biktarvy, the first single tablet combination HIV treatment with the ingredient bictegravir, was FDA approved in 2018 and had an estimated Medicaid rebate of 24% in 2019. It can be difficult for states to secure supplemental rebate agreements for these types of drugs, meaning their inclusion in the model would likely result in savings for states but at a cost to manufacturers.

However, there are also drugs, typically those with more competitors or that have been on the market longer, for which states are already receiving sizeable Medicaid rebates (like Drug B or C). For example, Eliquis, an anticoagulant (or blood thinner), was FDA approved in 2012 and had an estimated Medicaid rebate of 100% in 2019, meaning Medicaid programs are likely paying little to nothing for the drug. In cases where Medicaid rebates are already high, there may not be substantial savings for states through the GENEROUS model, but the impact of the model on manufacturer profits would be mitigated.

Medicaid drug rebates also vary by state, resulting in differing model impacts across states. While federal statutory rebates are required by law and calculated by CMS, the number and magnitude of SRAs vary across states. Medicaid rebates reduced gross Medicaid spending on prescription drugs by 53% on average nationally from FY 2019 to FY 2024, though the percentage varies across states. MACPAC data from FY 2024 shows that drug rebates (including both statutory and state supplemental rebates) reduced gross Medicaid spending on drugs by less than 40% in four states (Kentucky, Oregon, South Dakota, and Virginia) to over 90% in another four states (Delaware, Mississippi, Nevada, and Wyoming). This variation likely reflects differences in the amount and types of drugs paid for as well as differences in SRAs across states. States will likely complete their own internal analyses to assess model impact, including comparing their existing supplemental rebate agreements to what is available under the model and analyzing the impacts of standardized criteria before entering into new model SRAs.

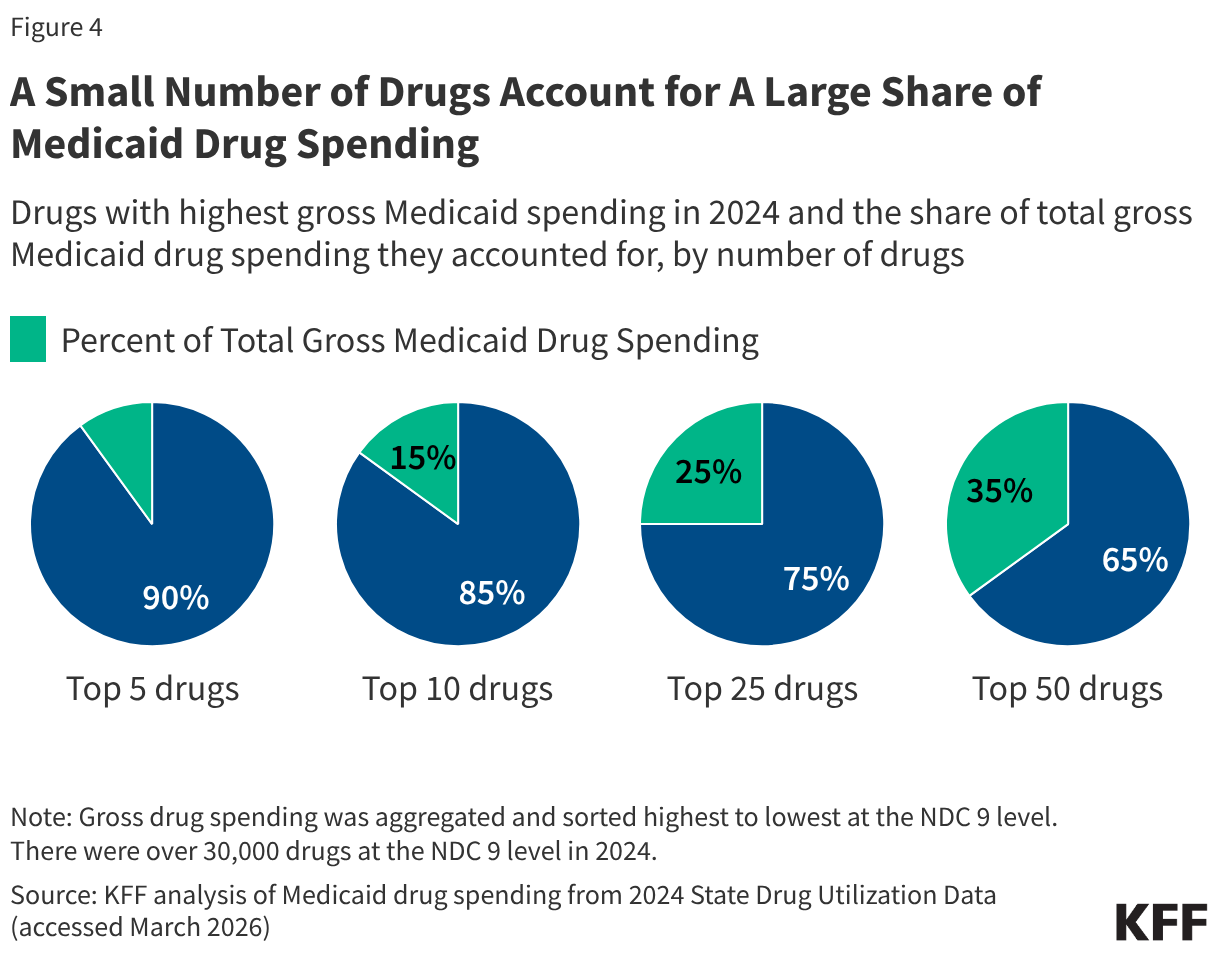

Medicaid drug utilization and spending patterns will also have implications for the Medicaid savings possible under the model. KFF analysis of Medicaid State Drug Utilization Data shows that a relatively small number of drugs account for a large share of Medicaid drug spending (Figure 4). The top five drugs (Biktarvy, Humira, Stelara, Dupixent, and Ozempic) account for 10% of all Medicaid drug spending, and the top 50 drugs account for over one-third of all Medicaid drug spending. Substantial MFN supplemental rebates on the costliest and most utilized drugs for Medicaid programs could result in significant savings (if the drugs are not already subject to sizeable Medicaid rebates), whereas substantial rebates on drugs that are not frequently utilized or only account for a small share of spending would have less of an impact. In addition, the overall number of participating manufacturers and model drugs as well as the number of participating states will affect the magnitude of savings.

Overall, GENEROUS model savings will depend on who participates, both manufacturers and states, and what drugs are included. While these factors remain uncertain at this time, the implications for Medicaid drug costs may become clearer as additional model details become available or if manufacturers respond to recent Senate letters requesting details of the Trump administration’s deals. Looking ahead, substantial state participation will likely indicate the potential for considerable model savings as states may only opt in if they expect the model supplemental rebates to be larger than their current supplemental rebates. States are also currently facing broader state budget pressures and federal Medicaid cuts, which may make some states eager to adopt pharmacy cost containment strategies. Further, manufacturer model participation may increase following the recent announcement of new pharmaceutical tariffs for companies who have not yet entered into MFN deals, though it is not clear what will happen to manufacturer participation when the tariff reprieves end. Once implemented, the GENEROUS model could also have implications for Medicaid prices on drugs from non-participating manufacturers or for the broader drug market, including changes in international prices or manufacturer participation in international markets.