rewrite this content and keep HTML tags

Workers contribute to health insurance in two ways. First, through a premium contribution, which is typically deducted from an employee’s paycheck. Then, secondly, through cost-sharing such as copays, coinsurance, and/or deductibles, which are paid when the employee utilizes services covered by their plan. While all workers enrolled in the plan must pay their premium (or have it paid by the employer), overall cost sharing is higher for workers who use more services.

Workers with health coverage in 2024, on average, were responsible for 16% of the premium for single coverage and 25% of the premium for family coverage. In dollar terms, the average annual contribution for covered workers was $1,368 for single coverage and $6,296 for family coverage.

Over time, the average premium contribution for covered workers has increased. For example, over the last 10 years, the single coverage average contribution has increased 27% and the family coverage average contribution increased 31%. At the same time, the share of the premium paid by workers has remained relatively consistent. In 2024, covered workers contributed, on average, 16% of the premium for single coverage and 25% of the premium for family coverage, which was similar to these averages a decade ago. This is because as premiums have increased over time, both employers and employees have faced similar increases on average.

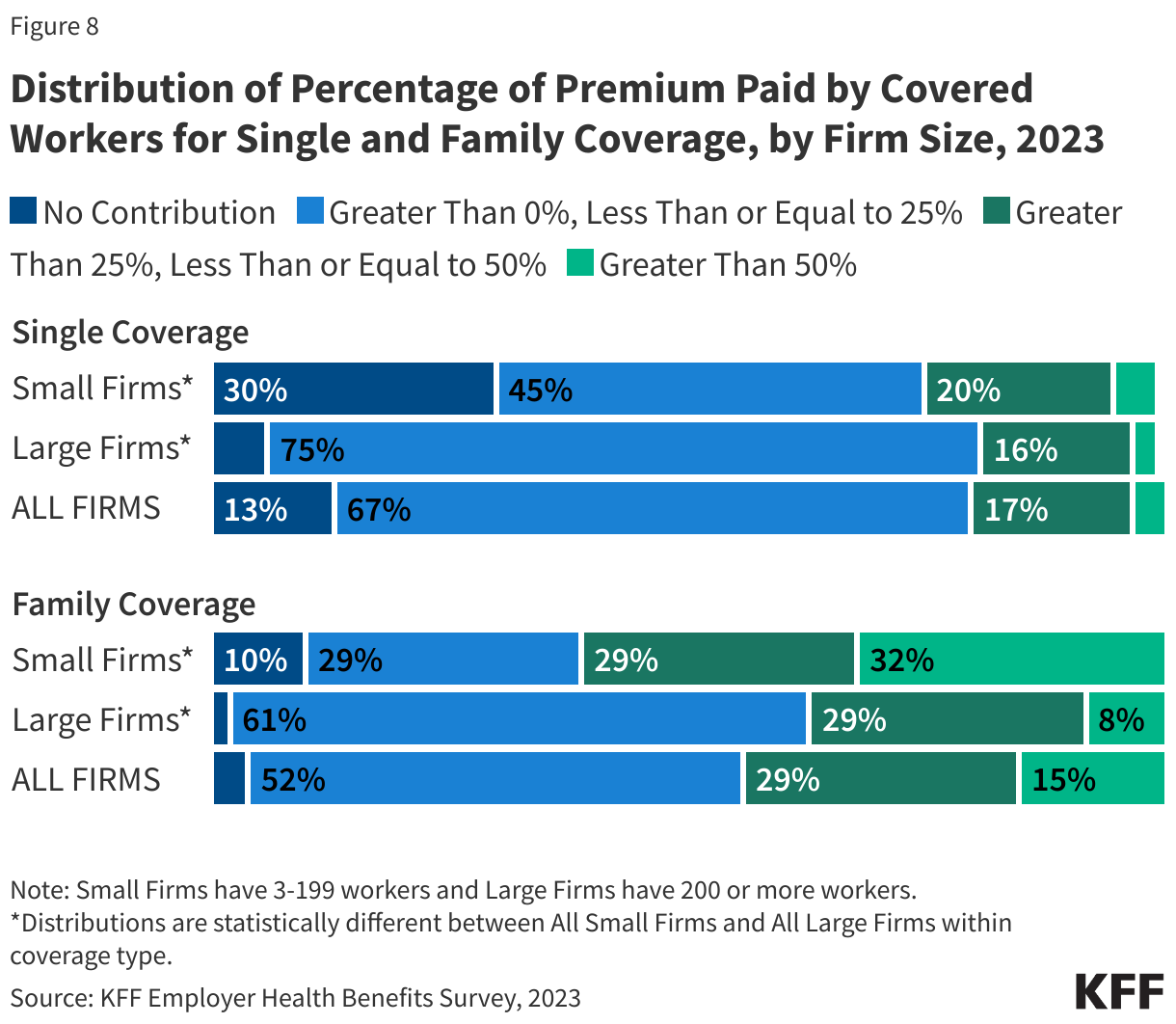

There remains a lot of variation in how much workers are required to contribute to their health plan across firms, particularly within firm size. In 2024, 37% of covered workers at small firms were enrolled in a plan where the employer paid the entire premium for single coverage. This was only the case for 5% of covered workers at large firms. However, 26% of covered workers at small firms were in a plan where they must contribute more than half of the premium for family coverage, compared to 6% of covered workers at large firms. The family average contribution rate for covered workers in firms with fewer than 200 employees was 33%, which is higher than the average contribution rate of 23% for covered workers in larger firms. Small firms often approach the cost of health insurance differently than large firms, sometimes making the same employer contribution regardless of whether the employee enrolls any dependents. Similarly, some large employers encourage spouses and dependents to enroll in other plans, if they have access, through spousal surcharges.

In addition to any required premium contributions, most covered workers must pay a share of the cost of the medical services they use. The most common forms of cost-sharing are deductibles (an amount that must be paid before most services are covered by the plan), copayments (fixed dollar amounts), and coinsurance (a percentage of the charge for services). Some plans combine cost sharing forms, such as requiring coinsurance for a service up to a maximum amount or requiring either coinsurance or a copayment for a service, whichever is higher. The type and level of cost sharing may vary with the kind of plan in which the worker is enrolled. Cost sharing may also vary by the type of service, with separate classifications for office visits, hospitalizations, and prescription drugs. Plans often structure their cost sharing to encourage enrollees to reflect on their use, reducing overall utilization.

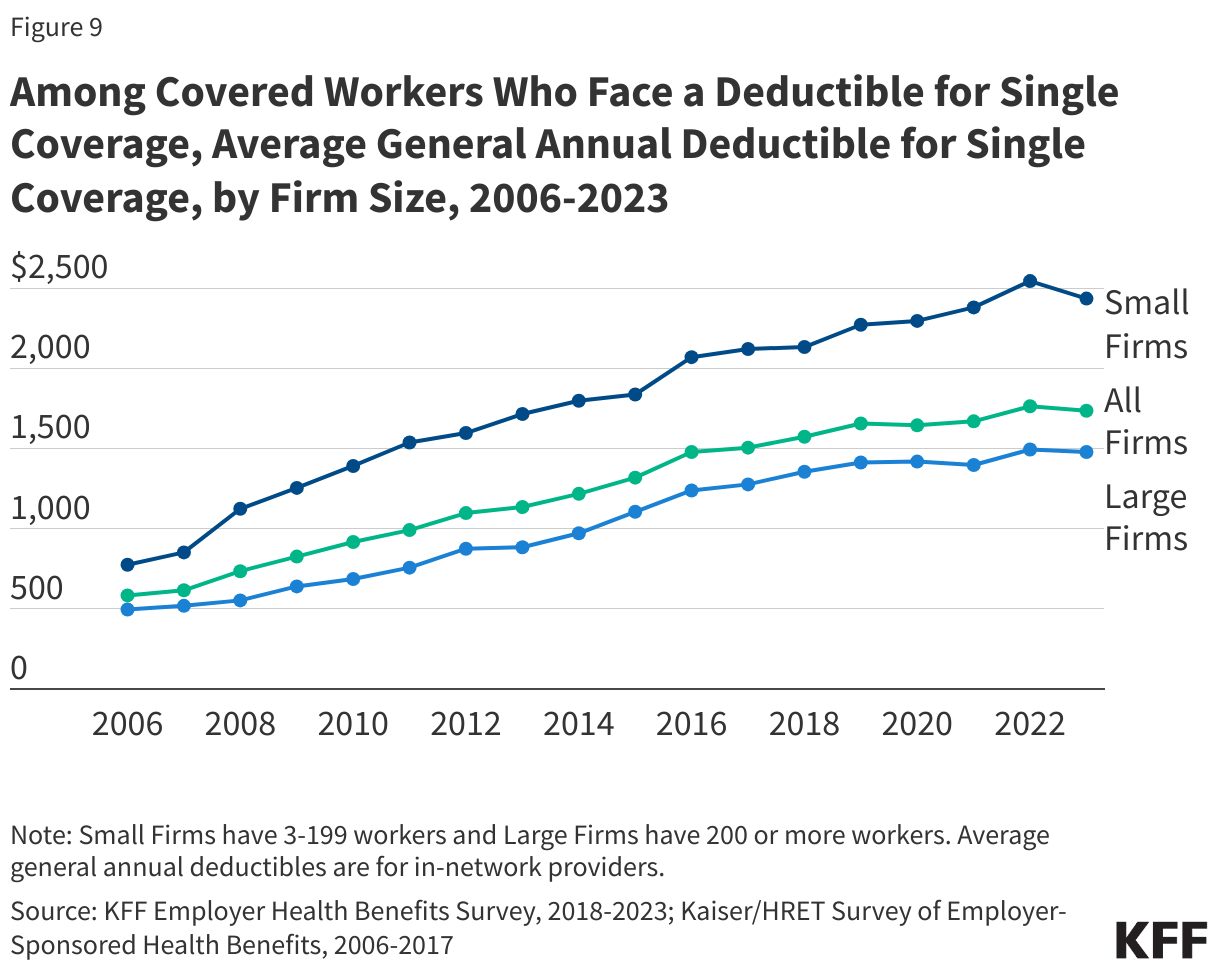

In recent years, general annual deductibles have grown in prominence in plan design. In 2024, 87% percent of covered workers were enrolled in a health plan that required an enrollee meet a deductible before the plan covered most services. The average deductible amount as of 2024 for workers with single coverage and a general annual deductible was $1,787. On average, covered workers at smaller firms face higher deductibles than those at large firms ($2,434 vs. $1,478). Generally, a substantial share of workers faced relatively high deductibles. Fifty percent of workers at small firms and 26% of workers at large firms had a general annual deductible of $2,000 or more. Over the last five years, the percentage of covered workers with a general annual deductible of $2,000 or more for single coverage has grown from 28% to 32%.

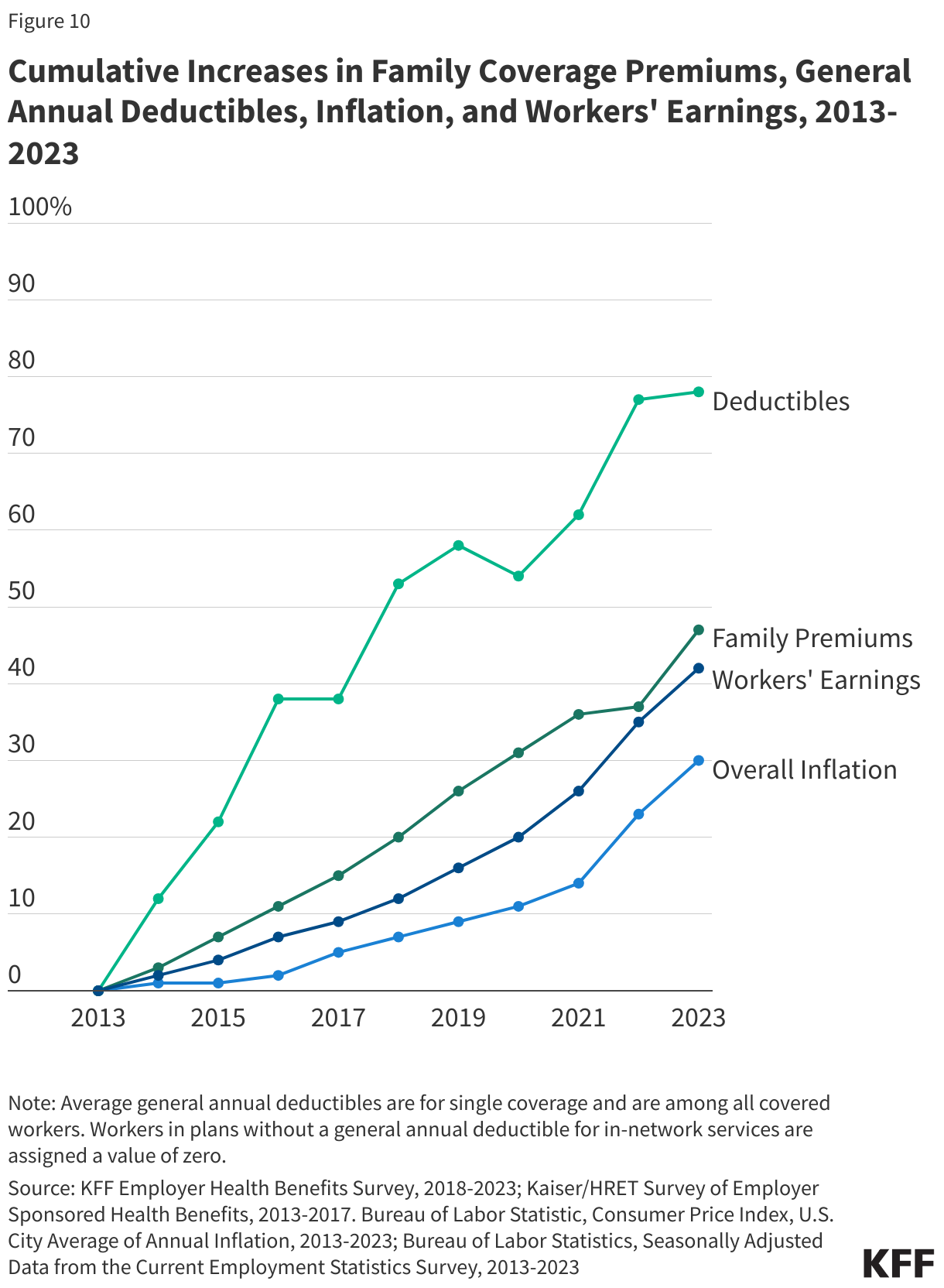

While average deductibles have not grown over the last few years, the growth over the last ten years outpaces the increases in premiums, wages and inflation. The rise in deductible costs has focused attention on consumerism in health care. Some believe that increasing deductibles will place a greater incentive on enrollees to shop for services, therefore reducing total plan spending. Alternatively, deductibles are less common in Health Maintenance Organization (HMO) plans, which use forms of gatekeeping to dissuade utilization. The growth of deductibles has had important consequences for the financial protection that health insurance provides. A multitude of plans require deductibles well in excess of the financial assets of many of their enrollees. As opposed to coinsurances and copays that accumulate throughout the year, deductible spending may require enrollees to finance relatively high expenses all at once.

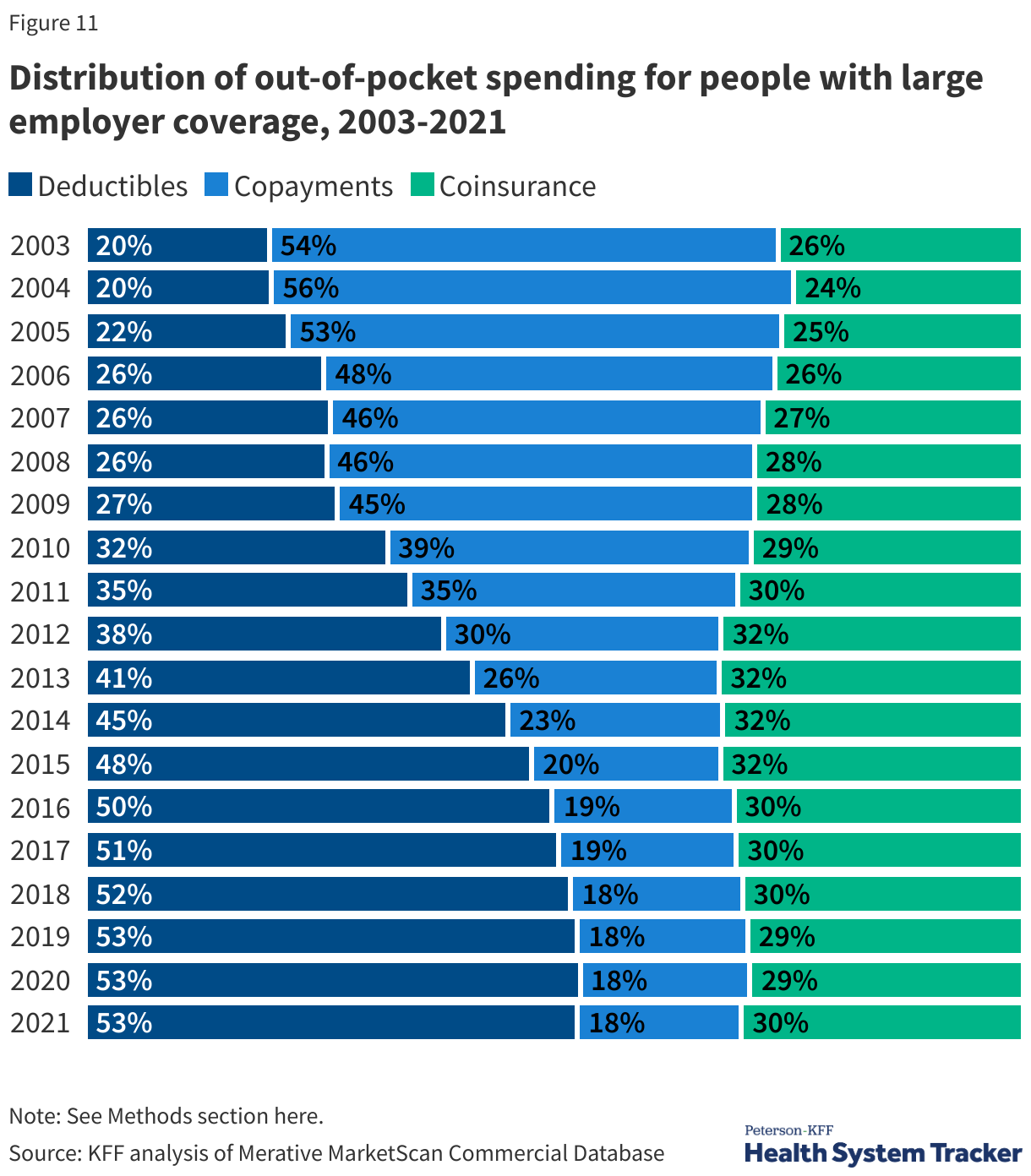

In addition to looking at the average obligations enrollees face under their health plan, we can look at the actual spending incurred by enrollees in large group plans. In 2021, deductibles accounted for more than 58% of an enrollee’s cost-sharing liability, which is significantly greater than 35% of enrollee liability ten years ago.

The amount of cost sharing large group enrollees face varies, particularly around how many health services a person uses. Individuals who have a hospitalization, or a chronic condition which requires ongoing management, often incur higher cost-sharing over the year. For example, large group enrollees faced an average of $779 in cost sharing, but individuals with a diabetes diagnosis (even without complications) incurred costs of $1,585 in 2017.

While some employer health plans have relatively generous benefits, there remains a concern about affordability, particularly for lower-wage workers who do not have the assets to meet the cost-sharing required under their plan, as well as for individuals enrolling in family coverage at smaller firms. Overall, individuals in families with employer coverage spend 2.4% of their income on the worker contribution required to enroll in an employer-sponsored health plan, and another 1.4% of their income on typical out-of-pocket spending on cost-sharing. Individuals covered by employer-sponsored plans in households at or below 199% of the FPL contribute nearly 10% of their income on average towards their premiums and cost-sharing.

A key component of plan design is the out-of-pocket maximum, which caps the amount of money an enrollee spends on in-network covered benefits within a year.

The ACA requires that almost all plans have an out-of-pocket (OOP) maximum below a federally determined limit. In 2024, 14% of covered workers in plans with an OOP maximum had an OOP maximum of less than $2,000 for single coverage, while 24% of these workers had an OOP maximum above $6,000.